What if the most effective tool for your 2026 growth isn’t a new marketing campaign, but a strategically structured business overdraft? It is exhausting to manage the constant stress of lumpy cash flow, especially with the July 2026 Payday Super regulations adding fresh pressure to your weekly payroll cycle. We understand that staring at a pile of unpaid invoices while an unexpected equipment repair bill sits on your desk is a situation no business owner enjoys. You deserve to feel in control of your finances rather than being reactive to every hurdle that comes your way.

We agree that the difference between a thriving enterprise and one that is just getting by often comes down to having the right safety valve in place. This article promises to help you master the essentials of business overdrafts so you can manage your working capital with absolute confidence. We will walk you through the mechanics of how these facilities work, provide a ready to go checklist of every document you need for a successful application, and help you decide whether a secured or unsecured option fits your specific needs. By the end, you will have a clear, professional roadmap to ensure your business stays in good hands through 2026 and beyond.

Key Takeaways

- Discover how a business overdraft acts as a cost-effective revolving facility where you only pay interest on the funds you actually use.

- Learn the specific frameworks for deciding when an overdraft is the superior choice over a business credit card or a standard working capital loan.

- Identify the critical “clean conduct” benchmarks and financial documents lenders require to approve your facility in the 2026 lending environment.

- Understand the strategic differences between secured and unsecured structures to protect your assets while maximising your borrowing power.

- Gain inside access to over 30 lenders and proprietary technology to streamline your application and secure the most competitive market rates.

Table of Contents

- Understanding the Business Overdraft: Your 2026 Cash Flow Safety Net

- When to Use an Overdraft vs Other Finance Options

- Secured vs Unsecured Overdrafts: Choosing the Right Structure

- The Ultimate Business Overdraft Application Checklist

- How a Broker Unlocks the Best Overdraft Rates for Your Business

Understanding the Business Overdraft: Your 2026 Cash Flow Safety Net

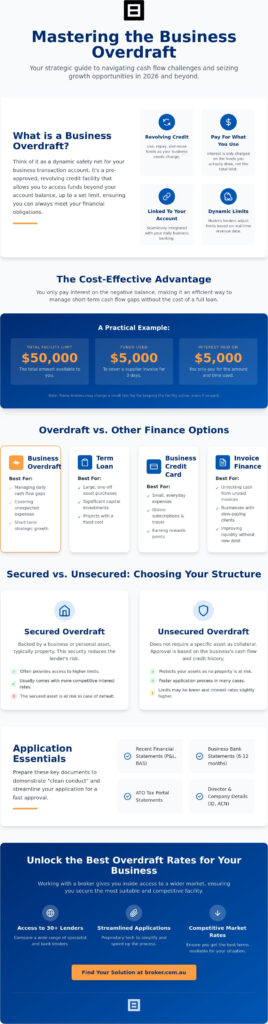

Think of a business overdraft as a dynamic extension of your existing transaction account. It is a revolving credit facility that allows your business to draw more money than is currently available in your balance, up to a pre-approved limit. While you might be familiar with the basic concept of what is an overdraft, the 2026 version of this finance tool is significantly more sophisticated than the rigid products of the past. It serves as a tailored buffer, ensuring you can meet immediate obligations without the stress of a declining balance.

The primary appeal of this facility lies in its flexibility compared to a standard term loan. A term loan provides a lump sum with a fixed repayment schedule, which is excellent for purchasing a specific asset but often too heavy for daily operations. In contrast, an overdraft expands and contracts with your cash flow needs. A major trend we are seeing in 2026 is that Australian lenders are increasingly moving away from static annual reviews. Instead, they now utilize real-time data feeds from cloud accounting software to set and adjust limits. This means your access to capital can grow seamlessly alongside your actual revenue, providing a level of agility that traditional finance simply cannot match.

How the Interest is Calculated

One of the most efficient aspects of a business overdraft is the “pay only for what you use” model. Interest is calculated on the daily overdrawn balance rather than the total facility limit. If you have a $50,000 limit but only use $5,000 for three days to cover a supplier invoice, you only pay interest on that $5,000 for that specific window. This makes it an incredibly cost-effective tool for budget management. However, it’s vital to be aware that some lenders charge “unused limit fees” or line fees. These are small, ongoing charges for the privilege of having the funds ready and waiting. This revolving nature of the debt ensures that as you deposit client payments, your debt reduces instantly, freeing up your limit for the next business cycle.

The Role of the “Safety Valve” in SME Finance

For most Australian SMEs, the facility acts as a strategic safety valve. It bridges the often unpredictable gap between paying your team or suppliers and receiving cleared funds from your own clients. With the 2026 payroll environment becoming more demanding, having this buffer prevents the anxiety of a temporary shortfall. The most successful business owners we work with ensure they have this facility in place long before a cash flow crunch actually hits. Waiting until you are in a desperate position often makes the application process more complex; securing your access to capital during a period of stability ensures you remain in total control when the unexpected occurs.

When to Use an Overdraft vs Other Finance Options

Selecting the right finance tool is a decision that impacts your bottom line as much as your daily stress levels. While many business owners default to the products they already have, a strategic comparison often reveals that a business overdraft provides a unique balance of speed and cost-effectiveness that other facilities lack. It isn’t just about having access to cash; it’s about the cost of that capital and how it integrates with your existing banking workflow. Choosing the wrong product can lead to unnecessary interest costs or, worse, a lack of liquidity when you need it most.

We often see clients use these facilities for two distinct purposes: the “emergency” safety net and “strategic growth”. An emergency use case might involve covering an unexpected tax bill or a sudden equipment failure that threatens to halt production. Strategic growth, however, is where the business overdraft truly shines. It allows you to confidently bid on larger contracts or hire new staff before the revenue from those projects hits your account. If your growth is specifically tied to a high volume of outstanding invoices from slow-paying corporate clients, Invoice Finance might be a more potent competitor, as it unlocks the value of your receivables without adding traditional debt to your balance sheet. For one-off, specific purchases like a bulk stock buy, a Working Capital Finance loan might offer a more structured repayment path.

Overdraft vs Business Credit Card

Business credit cards are handy for earning rewards on minor expenses, but they fall short for significant operational needs. Overdrafts typically offer much higher limits and significantly lower interest rates for facilities exceeding $10,000. Crucially, a credit card is often restricted to merchant transactions or comes with high “cash advance” fees. An overdraft gives you direct access to cash in your account. This allows you to pay staff, rent, or subcontractors through your standard banking portal without incurring penalties. It’s a more professional and flexible way to manage larger lumpy expenses that a card simply cannot handle.

Overdraft vs Line of Credit

Although the terms are sometimes used interchangeably, a Line of Credit is usually a standalone facility, whereas an overdraft is physically linked to your transaction account. A line of credit is often the superior choice for large-scale business restructures or major capital projects where you need a separate pool of funds to draw from. For the day-to-day rhythm of an Australian SME, the integrated nature of an overdraft makes it the more seamless option. If you are unsure which structure suits your 2026 goals, you can discover more about tailored finance solutions through our expert team who can help you choose with confidence.

Secured vs Unsecured Overdrafts: Choosing the Right Structure

Choosing the right structure for your business overdraft is a pivotal moment in your financial planning. It is more than just a box-ticking exercise; it is a strategic decision that balances the cost of your capital against the level of personal risk you are willing to carry. While many traditional banks will push you toward a secured model, the modern Australian lending market in 2026 offers significantly more nuance. Understanding these differences ensures you don’t inadvertently put your personal assets at risk while trying to grow your professional ones.

A secured overdraft is typically backed by tangible assets, such as residential or commercial property. Because the lender has a “safety net” to fall back on, they generally offer lower interest rates and more generous borrowing limits. On the other hand, an unsecured overdraft is supported primarily by your business’s cash flow and trading history. While these usually come with a higher interest rate, they often require a director’s guarantee rather than a mortgage over your home. The choice between them often comes down to how much “equity” you have available and how quickly you need to move.

We must warn you about the hidden risks of cross-collateralisation. This happens when a lender links your business debt to your personal assets, such as your family home, under a single security umbrella. If one part of your financial world faces a hurdle, the lender may have the power to freeze or call in assets across both. It is a trap that many business owners fall into when dealing directly with a single bank. By separating your security, you maintain a layer of protection that is essential for long-term peace of mind.

The Benefits of Going Unsecured

For many agile SMEs, an unsecured business overdraft is the gold standard for flexibility. The most significant advantage is the speed of approval. Because there are no property valuations required, funds can often be accessed in a fraction of the time it takes to process a secured application. This structure ensures you aren’t tying up the family home, keeping your personal and professional lives distinct. Businesses with consistently strong cash flow and at least two years of clean trading history are the ideal candidates. At Broker.com.au, we specialise in finding these flexible options outside the Big Four, giving you access to lenders who value your business’s performance over your property portfolio.

When Security Makes Sense

Security makes sense when your primary goal is to minimise interest costs or secure a much larger facility limit. If you have significant equity in a commercial property or a residential asset, pledging it can unlock the most competitive rates available in the 2026 Australian market. Lenders are currently open to a wider range of assets, including well-located commercial suites and even some high-value industrial equipment. This path is often best for established firms looking for a permanent, high-limit buffer to support long-term operational stability rather than quick, short-term liquidity.

The Ultimate Business Overdraft Application Checklist

Preparing for a business overdraft application doesn’t have to be a source of anxiety. In 2026, lenders have moved toward a more holistic view of your enterprise, focusing on three core pillars: profitability, stability, and character. While your balance sheet tells part of the story, your “account conduct” often carries the most weight. Lenders look for a history of clean transactions, meaning no dishonoured payments or unarranged over-limit events on your existing accounts. Before you begin the process, it’s essential to check both your personal and business credit scores to ensure there are no surprises that could stall your momentum.

We believe that moving from a state of uncertainty to one of streamlined confidence starts with being prepared. When you approach a lender with a complete, professional package, you signal that your business is well managed and in good hands. This proactive approach not only speeds up the decision but often helps in securing more favourable terms. If your credit file has a few marks from the past, don’t panic. Many non-bank lenders in the current market are willing to look at the context of your situation rather than just a single number.

Essential Documentation Checklist

Having your paperwork organised in advance transforms a complex task into a seamless experience. Most Australian lenders will require the following to assess your eligibility for a business overdraft:

- Up-to-date BAS statements: Usually covering the last two to four quarters to verify your recent turnover and GST obligations.

- Bank statements: Six to 12 months of transaction history, though many modern lenders now prefer direct digital bank feeds for faster verification.

- Tax returns: The most recent two years of both personal and business returns to confirm long-term financial stability.

- Proof of identity: Current Australian driver’s licences or passports for all company directors.

- Schedule of debt: A clear list of any existing business loans, equipment finance, or commercial leases you are currently servicing.

Utilising integrated cloud accounting platforms like Xero or MYOB significantly accelerates the 2026 application process by providing lenders with real-time, verified financial data.

Financial Health Indicators

Beyond the paperwork, lenders will run your numbers through specific filters to ensure you can manage the facility comfortably. We recommend reviewing these internal metrics before submitting your request:

- Revenue Growth: Demonstrate consistent or increasing revenue over the last two quarters to show your business is heading in the right direction.

- ATO Obligations: Ensure your GST and Superannuation payments are fully up to date; lenders in 2026 are particularly strict about ATO compliance.

- Debt Service Cover Ratio (DSCR): Verify that your operating cash flow is sufficient to cover all current and proposed debt obligations without strain.

If you aren’t sure how your financials stack up against current lending criteria, you can get started with a preliminary assessment to see where you stand. Our team acts as your expert guide, ensuring your application is positioned for a stress-free approval.

How a Broker Unlocks the Best Overdraft Rates for Your Business

Applying directly to your primary bank for a business overdraft often feels like the easiest path, but it is rarely the most cost-effective. A single bank can only offer you their own suite of products, which may not be the most competitive or flexible option for your specific industry. This is where the “Broker Advantage” becomes your greatest asset. By partnering with us, you gain immediate access to more than 30 different lenders, ranging from traditional institutions to boutique non-bank specialists. We take the stress out of the search by using our proprietary AI technology to scan the market for you. This ensures your application is both quick and accurate, matching you with a facility that aligns perfectly with your 2026 growth targets.

Comparing complex fee structures is where many business owners lose significant time and money. Between establishment fees, monthly line fees, and tiered interest rates, the true cost of a facility is often buried in the fine print. We handle all the heavy lifting, providing you with a clear, side-by-side comparison of your best options. Our role is to act as your expert guide and long-term partner. We don’t just secure your initial funding; we stay by your side to help with future loan restructures as your business evolves and scales. You can move forward with the relief of knowing your finance is being managed by professionals who prioritise your results over mere process.

Beyond the Big Four

In the 2026 Australian market, non-bank lenders have developed a significant appetite for providing an unsecured business overdraft. These lenders often provide more flexible eligibility criteria than the major banks, particularly for businesses with strong digital accounting records and real-time data feeds. Working with a broker gives you inside access to wholesale rates and tailored products that aren’t advertised to the general public. This exclusive advantage allows you to secure a facility that balances high limits with manageable costs, ensuring your working capital remains efficient and your personal assets remain protected from unnecessary cross-collateralisation.

Getting Started with Broker.com.au

We believe that high-stakes financial decisions should be met with streamlined confidence rather than pressure. When you reach out to us, you’ll be connected with seasoned experts like Matt or Kylie who understand the complexities of the local lending landscape. Our “I’m interested” approach is designed to be the start of a low-pressure conversation where we prioritise your specific dreams and needs. You’ll quickly see that you’re in good hands, with a team committed to going above and beyond to find the right fit for your business. Let us manage the complexities while you focus on leading your enterprise toward a successful 2026.

I’m interested in a business overdraft tailored for my growth

Secure Your Business Future with Confidence

Managing lumpy cash flow shouldn’t feel like a constant battle against the clock. You now have the roadmap to understand how a business overdraft acts as a strategic safety valve, providing the flexibility to bridge gaps without the rigid structure of a term loan. Whether you choose an unsecured facility to protect your personal assets or a secured option to maximise your borrowing power, being prepared with a clean application is your first step toward financial freedom.

As an award-winning business loan broker, we provide inside access to a wide panel of bank and non-bank lenders that the average consumer simply can’t reach. Our proprietary AI technology ensures your application is handled with precision and speed, moving you from uncertainty toward streamlined relief. You don’t have to navigate the shifting 2026 lending landscape alone. Our team is ready to act as your expert guide, helping you turn your financial goals into a reality.

I’m interested in exploring business overdraft options

Your business growth is within reach, and we are here to ensure you stay in good hands every step of the way.

Frequently Asked Questions

Is a business overdraft better than a business loan?

An overdraft is superior for short term, revolving needs, whereas a term loan suits one off asset purchases. If you need to manage weekly payroll or small supplier gaps, the flexibility of the revolving limit is the right choice. For a major equipment upgrade or property purchase, a structured loan with a fixed repayment term usually offers more long term stability and lower overall costs.

What are the typical fees associated with a business overdraft in Australia?

Typical costs include an establishment fee, a monthly or quarterly line fee for keeping the facility open, and interest charged only on the funds you actually use. Some Australian lenders might also apply an unused limit fee if the facility sits idle for an extended period. We help you compare these complex layers to ensure your business overdraft remains a cost effective tool for your growth.

Can I get a business overdraft if I am a new start-up?

While most lenders prefer at least 12 to 24 months of trading history, start-ups can occasionally secure a facility with strong revenue projections or property security. It is generally more challenging for brand new ventures to access an unsecured option without a proven track record of cash flow. We can explore alternative working capital solutions if your business is still in its infancy stages.

Does a business overdraft affect my credit score?

Yes, the initial application involves a credit check which can temporarily impact your score. Once the facility is active, your conduct is reported to credit bureaus. Maintaining clean account conduct and staying within your approved limit can actually demonstrate financial reliability to future lenders. It is a powerful way to build a professional credit profile when managed with care and precision.

What happens if the bank cancels my overdraft on demand?

Most overdraft contracts include an on demand clause, meaning the bank can technically ask for full repayment at any time. While this is rare for businesses with clean conduct and stable revenue, it highlights the importance of having a diverse lending strategy. If this occurs, we act as your high level fixer to help you refinance or restructure your debt through our wide panel of lenders.

How much can I typically borrow with an unsecured business overdraft?

Unsecured limits are typically calculated as a percentage of your annual turnover, often ranging from $10,000 to $250,000. According to industry data from 2026, the average approved facility for Australian small businesses is approximately $92,140. Your specific limit will depend on your cash flow stability, the industry you operate in, and your overall credit profile as a director.

Can I use a business overdraft to pay for tax or BAS obligations?

Yes, using a business overdraft to manage BAS or tax obligations is a common and strategic use of the facility. It allows you to meet your ATO deadlines on time while waiting for outstanding client invoices to clear. This proactive approach prevents late payment penalties and ensures your business remains in good standing with the tax office throughout the financial year.

Do I need to provide a personal guarantee for an unsecured overdraft?

Directors are almost always required to provide a personal guarantee for an unsecured facility. This provides the lender with the necessary assurance that the debt will be managed responsibly even without physical assets like property being pledged as security. It is a standard requirement in the Australian market that we help you navigate with total clarity and professional insight.