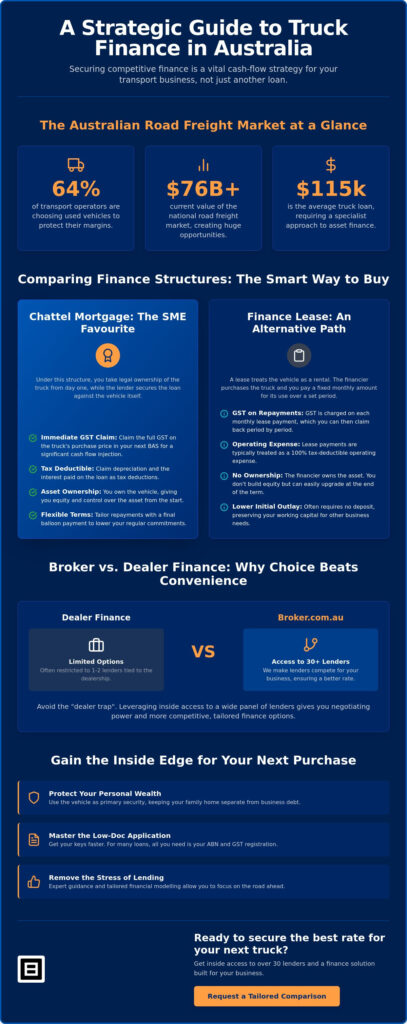

Did you know that 64% of Australian transport operators are currently choosing used vehicles over new ones to protect their margins? With the national road freight market now valued at over $76 billion, securing competitive truck finance is no longer just about getting a loan; it’s a vital cash-flow strategy. It’s completely understandable if you feel frustrated by high interest rates or confused by technical terms like chattel mortgages and balloon payments. You need a rig that earns money, not a debt that creates constant stress.

We know the anxiety of facing big banks that don’t understand the seasonal ebbs and flows of logistics income. This guide will help you master the complexities of heavy vehicle lending to secure the best rates and tax-effective structures for your business. We’ll provide a clear breakdown of the 2026 interest rate benchmarks, explain how the August 1 Heavy Vehicle National Law reforms impact your fleet, and show you how to access a panel of lenders who prioritise your growth. You’ll gain the inside access needed to turn your next vehicle acquisition into a streamlined, professional success.

Key Takeaways

- Understand why using the vehicle as primary security protects your personal wealth and home from business debt.

- Identify the specific GST and tax advantages of a chattel mortgage compared to traditional leasing structures.

- Learn how to avoid the “dealer trap” by leveraging inside access to over 30 lenders for more competitive truck finance.

- Master the low-doc application process to get your keys faster using only your ABN and GST registration.

- Discover how tailored financial modelling and expert guidance can remove the stress of lending, allowing you to focus on the road.

Table of Contents

- What is Truck Finance and Why Does Your Business Need a Specialist?

- Comparing Truck Finance Structures: Chattel Mortgage vs. Lease

- Broker vs. Dealer Finance: Why Choice Beats Convenience

- Navigating the Application: From Low-Doc to Approval

- Customised Truck Finance Solutions with Broker.com.au

What is Truck Finance and Why Does Your Business Need a Specialist?

Truck finance is more than just a line of credit; it’s a specialised form of asset funding designed for the unique demands of the heavy vehicle industry. Unlike a standard bank loan that might require your family home as collateral, dedicated logistics lending uses the vehicle itself as the primary security. This structure, often organised as a Chattel Mortgage, ensures that your personal assets remain protected while your business grows. In a market where the average truck loan sits at $115,000, having a tailored solution is essential for maintaining a healthy balance sheet and long-term peace of mind.

General business loans often fall short because they don’t account for the specific operational realities of transport. A traditional lender might look at seasonal income drops with suspicion, whereas a specialist understands that freight volumes fluctuate throughout the year. As we move through 2026, the Australian logistics landscape is shifting. With interest rates for business loans currently ranging from 7.49% to 15.00% p.a., the difference between a generic product and a strategic finance structure can represent tens of thousands of dollars in interest over the life of the loan. You need an expert guide who can help you identify the most efficient path forward.

The Core Benefits of Dedicated Asset Finance

Asset finance functions as a strategic tool for preserving liquidity by ensuring your cash stays in the business rather than being tied up in depreciating metal. Liquidity is the lifeblood of any trucking operation. By opting for a dedicated facility, you preserve your working capital for essential day-to-day operational expenses like fuel, tyres, and maintenance. This approach also provides the flexibility to upgrade to newer, more fuel-efficient models more frequently. Staying competitive in 2026 requires a focus on total cost of ownership, and modern rigs offer data-driven efficiency that older models simply can’t match.

Who is Truck Finance For?

The Australian road freight market is valued at $76.9 billion, and this growth creates opportunities for operators of all sizes. Our tailored solutions are designed for:

- Owner-operators: Individuals looking to secure their first prime mover or rigid truck to transition from employee to business owner.

- Established transport companies: Large-scale operations needing to scale their fleet quickly to meet the sustained demand from Australia’s e-commerce boom.

- SMEs in construction and agriculture: Businesses that require specialised delivery vehicles or heavy machinery but want to keep their home equity separate from their business debt.

Whether you’re moving containers from the Port of Melbourne or delivering produce across the Nullarbor, having the right finance partner ensures you’re in good hands.

Comparing Truck Finance Structures: Chattel Mortgage vs. Lease

Deciding on a finance structure is often more important than the interest rate itself. While many lenders push standard products, a truly strategic approach to truck finance considers your specific tax profile and GST reporting requirements. For Australian businesses navigating the 2026 economic climate, including shifting fuel excise rates and the upcoming Heavy Vehicle National Law reforms, cash flow flexibility is paramount. Organisations like the Australian Trucking Association often highlight how regulatory compliance costs can impact bottom lines, making your choice of loan structure a critical lever for profitability.

Your choice between ownership and usage will define your balance sheet for years. It’s not just about the monthly bill; it’s about how the asset works for your tax position. If you want to see how these different structures look for your specific situation, you can request a tailored comparison from our specialist team.

The Chattel Mortgage: The SME Favourite

A chattel mortgage remains the most popular choice for small to medium-sized transport businesses across Australia. Under this arrangement, you take legal ownership of the truck from the moment of purchase, while the lender secures the loan against the vehicle. This ownership model allows you to claim the full GST amount on the truck’s purchase price in your very next Business Activity Statement (BAS), providing a significant and immediate cash flow injection. It also grants you the ability to claim depreciation and interest charges as tax deductions. Because you own the asset, you can tailor your repayments with a balloon payment at the end of the term, which keeps your monthly outgoings manageable during quieter seasons or periods of fleet expansion.

Leasing Options for Fleet Management

Leasing offers a different path, primarily focused on usage and fleet turnover rather than immediate equity. A finance lease gives you the use of the truck with the option to purchase it at a pre-determined residual value at the end of the term. In contrast, an operating lease functions more like a long-term rental. This is often an “off-balance sheet” solution for larger entities, as the financier retains the risk of disposal and maintenance. It’s an efficient way to keep a fleet modern and fuel-efficient without the long-term debt obligations of ownership. While you don’t get the same upfront GST claim as a mortgage, the lease payments are generally 100% tax-deductible if the vehicle is used solely for business.

Balloon payments, or residuals, play a vital role in logistics lending. By deferring a portion of the principal to the end of the loan, you can significantly lower your monthly commitments. This strategy is particularly effective for operators who plan to trade in their rig before the balloon falls due, effectively using the vehicle’s resale value to clear the final debt. It’s a professional way to manage high-value truck finance without strangling your daily operating budget.

Broker vs. Dealer Finance: Why Choice Beats Convenience

Walking into a dealership and driving out with a new rig and a signed contract feels efficient. However, this “one-stop shop” convenience often masks what industry veterans call the “dealer trap.” When you rely on dealer finance, you’re typically limited to a single captive lender or a very small panel. This lack of competition means you’re often stuck with standardised rates and rigid terms that benefit the manufacturer’s bottom line rather than your own cash flow. While the salesperson might be an expert on engine specs, they rarely have the specialised financial modelling skills required to structure a loan for long-term tax efficiency.

Choosing a specialist broker gives you inside access to a panel of over 30 lenders, including non-bank institutions that specifically cater to the Australian transport sector. We look beyond the sticker price to analyse the total cost of credit, including hidden fees and charges that dealerships often gloss over. Our goal is to move you from a state of uncertainty to a position of streamlined confidence. By comparing multiple truck finance products, we ensure the structure aligns with your business goals, whether you’re prioritising immediate GST claims or long-term equity growth.

Unlocking Better Rates Through Competition

A broker’s primary role is to create a competitive environment where lenders must bid for your business. This is particularly important in 2026, where interest rates for logistics lending vary significantly between 7.49% and 15.00% p.a. based on the lender’s risk appetite. We have access to specialised transport lenders that do not deal directly with the public, offering wholesale rates that aren’t available on the showroom floor. Whether you have a long-established ABN or a more complex credit history, we can identify the specific lender most likely to offer a competitive approval without damaging your credit score with multiple direct applications.

The Long-Term Partnership Advantage

Unlike a dealership transaction that ends when you drive off the lot, working with a firm like Broker.com.au is the start of a strategic partnership. We act as your expert guide, helping you plan for future fleet expansion and providing advice on when to refinance as your business matures. You’ll have a dedicated advisor, such as Matt or Flavio, who understands the nuances of your operation and handles the heavy lifting of the paperwork. This boutique level of personal attention ensures that as your fleet grows, your truck finance remains flexible and efficient, leaving you free to focus on the road ahead.

Navigating the Application: From Low-Doc to Approval

Securing the right truck finance shouldn’t feel like a bureaucratic hurdle. We’ve refined the journey into five streamlined stages to move you from uncertainty to the driver’s seat. The process begins with a strategic consultation where we identify your fleet requirements. Next, our proprietary AI technology scans our panel of over 30 lenders to match your profile with the most competitive products. We then handle the heavy lifting of packaging and submitting your application. Once formal approval is secured, we manage the final documentation and coordinate settlement with the seller. This structured approach ensures you remain in good hands throughout the entire transaction.

For many Australian operators, the “Low-Doc” path is the most efficient way to scale. To qualify, lenders typically look for an active ABN held for at least two years and current GST registration. If you are a property owner, you may access even more favourable terms and higher lending limits. If you don’t meet these specific criteria, perhaps because you are a newer entity, we pivot to a “Full-Doc” application. This involves providing your recent Business Activity Statements (BAS), profit and loss statements, and tax returns. Our expertise lies in presenting these financials to highlight your business’s strength, ensuring a professional result even for complex situations.

Fast-Tracked Approvals for ABN Holders

Lenders prioritising speed look for indicators of stability. A clean credit history is the primary driver for instant approval on both new and used rigs. If your ABN has been active for less than two years, you can still qualify for competitive truck finance by demonstrating significant industry experience or offering a larger upfront deposit. We specialise in finding solutions for situations that fall outside the traditional lending norm, providing the local insights needed to navigate these hurdles. You can start your truck finance application today to discover which fast-track options suit your current business structure.

The Final Mile: Settlement and Delivery

The final stage is where our role as a “high-level fixer” truly adds value. Before you sign on the dotted line, we meticulously review the loan contract to identify any hidden early exit fees or annual charges that could impact your long-term costs. We then liaise directly with the dealership or private seller to ensure all compliance and insurance requirements are met for a seamless payout. Settlement can often occur within 24–48 hours of approval. This efficient turnaround means your new asset is on the road and earning revenue without unnecessary delays.

Customised Truck Finance Solutions with Broker.com.au

Securing a loan for a heavy vehicle shouldn’t be a source of anxiety. At Broker.com.au, we’ve replaced the traditional, cold banking experience with a sophisticated approach that blends high-level technology with boutique personal attention. Our proprietary AI doesn’t just scan for the lowest rates; it identifies the specific lender on our panel whose risk appetite perfectly matches your truck type and business profile. Whether you’re acquiring a single rigid truck or a fleet of prime movers, our system ensures you gain inside access to the most efficient structures available in 2026. This transparency means you’ll always understand the total cost of ownership before you commit.

We pride ourselves on being more than just a digital portal. We act as your expert guide, handling the complex financial modelling and lender negotiations so you can stay focused on your daily operations. Moving from uncertainty to a streamlined, approved finance plan is about having the right partner in your corner. We’ve seen how the right truck finance strategy can transform a small family business into a national logistics player; we’re committed to providing that same level of elite support to every client we serve.

Award-Winning Service for Australian Businesses

Our award-winning team understands that every logistics operation is unique. A traditional bank might struggle to value a specialised asset like a refrigerated van or a heavy haulage rig, but we thrive on these complexities. We’ve helped countless owner-operators scale their fleets by looking beyond the balance sheet to understand the true potential of their business. Testimonials from our clients frequently highlight the “can-do attitude” of team members like Matt and Kylie, who often go above and beyond to secure approvals for situations that fall outside the norm. This human-led advisory model ensures that you feel supported and informed at every turn.

Start Your Stress-Free Application Today

We believe that exploring your options should be a low-pressure conversation. Our “I’m interested” philosophy is designed to reduce the stress of high-stakes financial decisions. Instead of an aggressive sales pitch, we offer a professional consultation to see how we can best support your goals. You can use our integrated repayment calculators to estimate your potential ROI and see how different structures impact your monthly cash flow. When you’re ready to move forward, you’ll find that our process is seamless, efficient, and entirely centred on your needs. I’m interested in truck finance options and want to see how the right structure can drive my business forward.

Drive Your Logistics Growth in 2026

Mastering the intricacies of heavy vehicle lending is a vital step toward protecting your business margins and ensuring sustainable growth. By choosing a tax-effective structure like a chattel mortgage and leveraging the competitive environment created by a specialist broker, you avoid the common traps of limited dealer finance. Whether you’re scaling a fleet or securing your first prime mover, the right truck finance strategy ensures your capital remains liquid for the road ahead.

As an award-winning business loan broker, we offer the professional authority and local insights required to streamline your next acquisition. We provide inside access to over 30 specialist lenders and use proprietary AI for faster, accurate matching, removing the anxiety of high-stakes financial decisions. You’re in good hands with a team that prioritises your specific needs and handles the heavy lifting on your behalf.

I’m interested in tailored truck finance

Take the next step with confidence and get your business moving with a structure built for success.

Frequently Asked Questions

Can I get truck finance with a new ABN?

Yes, you can secure truck finance with a new ABN, though the criteria are often more stringent than for established businesses. Most lenders prefer an ABN to be active for at least two years; however, we have inside access to specialist lenders who consider new operators with significant industry experience. You may need to provide a larger deposit or additional proof of income to offset the perceived risk of a new venture.

What is a balloon payment and should I include one in my truck loan?

A balloon payment is a lump sum owed to the lender at the end of your loan term. Including one can significantly lower your monthly repayments, which helps preserve your daily cash flow for operational costs like fuel and maintenance. It’s a strategic choice if you plan to trade in the vehicle before the term ends or if you expect higher revenue later to cover the final payout.

Do I need to provide a deposit for truck finance?

You don’t always need a deposit to secure funding for a heavy vehicle. While a 10% to 20% deposit can reduce your interest charges and monthly commitments, many of our specialist lenders offer 100% finance for established ABN holders with a clean credit history. If you are a property owner, your chances of securing a no-deposit loan increase, allowing you to keep your working capital intact for business growth.

Is it better to lease or buy a truck for tax purposes in Australia?

The choice depends on your specific GST reporting and cash flow needs. Buying via a chattel mortgage typically allows you to claim the full GST on the purchase price in your next BAS, which is a major upfront benefit. Conversely, leasing payments are usually 100% tax-deductible as an operating expense. We recommend professional financial modelling to determine which structure offers the most efficient result for your current tax profile.

Can I finance a used truck from a private seller?

Yes, you can finance a used truck purchased from a private seller rather than a dealership. This process requires a few extra steps, such as a formal vehicle inspection and a valuation to ensure the asset’s worth matches the loan amount. Our team acts as a high-level fixer in these scenarios, coordinating directly with the seller to ensure all paperwork and title transfers are seamless and professional.

How long does the truck finance approval process take?

The approval process can be incredibly efficient, often taking between 24 and 48 hours for well-prepared applications. Using our proprietary AI technology, we can match you with a lender almost instantly, significantly speeding up the initial assessment. Once you provide the necessary documents, such as your BAS or bank statements, our expert guides work proactively to move your application from inquiry to formal approval without unnecessary delays.

What is a chattel mortgage and how does it benefit my business?

A chattel mortgage is a loan structure where you take ownership of the truck from day one while the lender uses the vehicle as security. The primary benefit is the ability to claim the full GST upfront and deduct both depreciation and interest charges from your taxable income. It’s a popular choice for SMEs because it offers the flexibility of balloon payments while keeping your personal assets protected from business debt.

Will my home be used as security for a truck loan?

No, your home is typically not required as security for a truck loan. Specialist asset finance is designed so that the vehicle itself serves as the primary collateral, which protects your personal property from business risks. This is a key reason why many operators prefer dedicated logistics lending over a general bank loan, as it keeps your business and personal financial worlds clearly separated and secure.