What if the secret to closing your next deal isn’t choosing the “best” lender, but rather refusing to choose just one? In the current 2026 market, the most successful Australian acquisitions don’t simply pick a side in the seller financing vs bank loan for business purchase debate. Instead, savvy buyers blend both to bridge valuation gaps and protect their personal assets. With the RBA holding the cash rate at 4.35 per cent and traditional business loan rates reaching as high as 9.81 per cent, the pressure on serviceability is real. You likely feel the weight of strict bank requirements, especially if you’re tired of being told your “goodwill” isn’t enough security or if you’re worried about hidden defects in the business you’re eyeing.

We’re here to help you move from uncertainty to a place of streamlined confidence. This guide will show you how to structure a funded acquisition that keeps repayments manageable and your equity protected. We’ll explore the critical differences in costs, the strategic advantages of vendor finance, and how to manage Australian PPSR registrations. Whether you’re looking at the government’s Economic Resilience Program or negotiating a private vendor carry-back, you’ll discover exactly how to secure your ideal business while ensuring a smooth transition from the previous owner.

Key Takeaways

- Understand why the debate of seller financing vs bank loan for business purchase in 2026 is less about choosing one side and more about de-risking your specific acquisition.

- Learn how a “clean break” bank loan provides lower long-term costs and market-linked rates for buyers with strong tangible assets.

- Discover how vendor finance effectively bridges the valuation gap when a bank’s assessment of business goodwill falls short of the asking price.

- See why “skin in the game” from the previous owner is a powerful tool to ensure a seamless handover and protect your new investment.

- Explore the strategic hybrid model that combines bank funding with seller debt to maximise your leverage while satisfying strict lending criteria.

Table of Contents

- Understanding Business Acquisition Finance in the Australian Market

- The Case for Bank Loans: Stability and Clean Breaks

- The Case for Seller Financing: Flexibility and Skin in the Game

- Direct Comparison: Bank Loan vs Seller Financing

- The Strategic Hybrid: How Broker.com.au Architect Your Deal

Understanding Business Acquisition Finance in the Australian Market

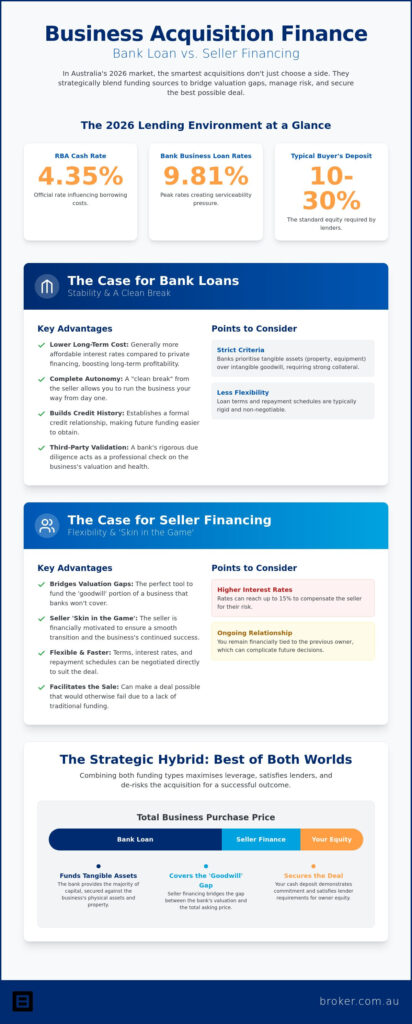

The Australian lending environment in 2026 presents a unique set of challenges for aspiring business owners. With the Reserve Bank of Australia holding the official cash rate at 4.35 per cent as of June 2026, the cost of capital remains a primary consideration for any acquisition. The fundamental choice between seller financing vs bank loan for business purchase often comes down to how a lender views the value of “goodwill.” In the current credit climate, Australian banks have tightened their belts, showing a clear preference for tangible assets over intangible reputation. This shift makes it harder to fund a purchase based solely on historical profit margins, forcing buyers to become more creative with their deal architecture.

Your choice of finance doesn’t just determine how you buy the business; it dictates how you’ll run it. High bank repayments can drain your working capital during those critical first six months of ownership. Conversely, a poorly structured vendor agreement could leave you legally exposed if the business underperforms. Success in 2026 requires matching your finance to the specific assets of the business, ensuring you have the operational freedom to grow after the keys change hands.

What is a Traditional Bank Loan for Business?

A traditional bank loan involves an institutional lender providing a lump sum to cover the purchase price, usually secured against the business assets or your personal property. Australian banks evaluate your application through the “Three Cs”: Character (your experience), Capacity (the business’s ability to repay), and Collateral (what the bank can seize if you default). Most lenders will require a General Security Agreement (GSA) over all business assets. With Westpac’s Business Development Rate at 9.02 per cent and BankSA’s Business Loan Rate at 9.23 per cent as of mid-2026, these loans offer stability but require significant equity, typically a deposit of 10 to 30 per cent.

What is Seller Financing (Vendor Finance)?

Seller financing occurs when the person selling the business agrees to let you pay a portion of the purchase price over time. Essentially, the seller acts as the bank. It’s helpful to understand what seller financing is in a legal sense; it is a debt instrument where the seller carries the risk of your success. Australian sellers often offer this to achieve a higher total sale price or to facilitate a faster exit in a competitive market. Common structures include promissory notes for a fixed sum, earn-outs based on future performance, or equity retainers where the seller keeps a small stake until they are fully paid out.

The Case for Bank Loans: Stability and Clean Breaks

For many Australian entrepreneurs, the appeal of a traditional bank loan lies in the “clean break” it provides. Unlike vendor finance, which often requires a multi-year relationship with the previous owner, a bank-funded deal allows you to take the keys and move forward with full autonomy. This independence is vital if you plan to pivot the business strategy or rebrand immediately. When financing a business acquisition, the primary appeal of a bank loan is often the lower long-term cost. While seller interest rates can climb as high as 15 per cent, current 2026 bank rates like Westpac’s 7.91 per cent Small Business Loan Rate offer a more manageable path to profitability.

Securing a bank loan also establishes a vital credit footprint. By successfully managing a major acquisition facility, you position your new enterprise for future growth. This relationship makes it significantly easier to access Business Acquisition Funding or equipment finance down the track. Additionally, the bank’s rigorous due diligence serves as an extra layer of protection. If a tier-one lender refuses to fund the deal because the figures look inflated, it’s a loud signal that you might be overpaying. In the seller financing vs bank loan for business purchase debate, the bank’s “yes” is a professional validation of the business’s health.

Secured vs Unsecured Bank Funding

The interest rate you pay often depends on your willingness to provide collateral. Using commercial or residential property as security can drastically reduce your margin, providing a safety net for your cash flow. Conversely, unsecured loans are available for high-performing businesses with strong histories, though they carry higher rates. Serviceability refers to the borrower’s demonstrated ability to meet all interest and principal repayments from the business’s projected net cash flow after accounting for existing debts and living expenses. Choosing the right structure ensures you don’t over-leverage your personal assets while keeping the business’s debt service cover ratio healthy.

The Application Process: Speed and AI

Traditional bank applications are notorious for stalling in the “black hole” of credit departments. We alleviate this anxiety by using proprietary AI to streamline the processing of your application. This technology identifies potential roadblocks before they reach the lender’s desk. Success depends heavily on professional financial modelling. Presenting a 3-way forecast that clearly shows the bank how you will repay the debt is the difference between a rejection and a fast approval. Our expert guides manage this complex paperwork, providing you with inside access to the best rates across a national panel, making the entire journey feel stress-free and efficient.

The Case for Seller Financing: Flexibility and Skin in the Game

While traditional lenders provide stability, they often struggle to fund the full value of a thriving business’s intangible assets. This is where the debate of seller financing vs bank loan for business purchase shifts in favour of the vendor. If a bank values a business at $1.5 million but the seller insists on $1.8 million based on future growth projections, a “valuation gap” emerges. Seller financing allows you to bridge this $300,000 divide without needing extra cash upfront. It also provides the ultimate “skin in the game.” A seller who carries a portion of the debt is highly motivated to ensure the handover is seamless. They won’t want to see the business fail if their own repayment depends on its ongoing success.

Repayment flexibility is another major drawcard that banks simply cannot match. Unlike rigid institutional schedules, vendor finance can be tailored to your specific cash flow needs. You might negotiate an interest-only period for the first six months while you find your feet, or align payments with seasonal revenue peaks. This level of customisation is rarely found in an Australian government guide to business funding, which typically focuses on more standardised debt products. Additionally, while a bank approval cycle can drag on for four to eight weeks, a vendor deal can be finalised in days, allowing you to move quickly on urgent opportunities.

Earn-outs and Performance Hurdles

Structuring payments through earn-outs is a brilliant way to protect yourself against “revenue fluffing,” which is the practice of temporarily inflating profits before a sale. By tying a portion of the purchase price to future profit targets, you align your interests with the departing founder. If the business hits its numbers, they get paid; if not, your debt is reduced. To stay secure, you must ensure all security interests are correctly registered on the Personal Property Securities Register (PPSR). This protects your position and clarifies who has a legal claim over the business assets if the transition doesn’t go as planned.

Negotiating the Vendor Note

Expect to pay a premium for this bespoke flexibility. Typical interest rates for seller financing in Australia range from 6 per cent to 15 per cent per annum, usually sitting about 2 to 4 per cent above standard bank rates. However, this cost is often offset by the “Right of Offset” clause. This allows you to deduct money from your repayments if the seller is found to have breached warranties or hidden defects after the sale. A comprehensive Letter of Intent must specify these financing terms early to ensure both parties are aligned on the debt structure before expensive legal drafting begins.

Direct Comparison: Bank Loan vs Seller Financing

Deciding between a bank and a vendor isn’t just about finding the lowest interest rate. It’s about weighing speed against cost and security against flexibility. When evaluating seller financing vs bank loan for business purchase, you’ll find that banks offer market-linked rates, currently ranging from 7.91 per cent to 9.81 per cent, but they demand a rigid, often slow approval process. Sellers, by contrast, are far more negotiable. While they might charge a premium of 10 to 15 per cent, they can often sign off on a deal in a fraction of the time it takes a credit committee to meet. This speed is essential when you’re competing against other buyers in a hot market.

The security requirements also differ significantly. A bank will almost certainly require a General Security Agreement (GSA) and may ask for a mortgage over your personal property. A seller is usually satisfied with a charge over the business assets themselves, registered on the Personal Property Securities Register (PPSR). This creates a collaborative relationship rather than a purely transactional one. Because the seller has a vested interest in your success, they’re often more willing to provide ongoing mentorship during the handover, whereas a bank’s interest begins and ends with your monthly repayment statement.

Impact on Cash Flow and Serviceability

Your ability to manage debt is measured by the Debt Service Cover Ratio (DSCR). Banks typically look for a ratio of 1.25x or higher, meaning your business must generate $1.25 in profit for every $1.00 of debt repayment. Bank loans often come with strict covenants that can restrict your operational spending if your margins dip. Vendor notes are generally more forgiving. If you hit a rough patch, a seller might agree to defer a payment to protect their long-term investment, while a bank’s automated systems may trigger a default notice. Understanding these nuances is key to maintaining a stress-free cash flow during your first year of trade.

The Hidden Risks of Cross-Collateralisation

One of the most significant risks in Australian business lending is cross-collateralisation. This happens when a bank ties your business loan to your family home. If the business fails, your primary residence is at risk. We believe you shouldn’t have to put your house on the line just to chase your professional goals. Our experts specialise in structuring deals that keep your personal and business assets separate, often by utilising Unsecured Business Loans or asset-backed finance that doesn’t touch your home equity. We provide the inside access needed to protect your family’s future while you grow your new enterprise.

If you’re ready to see which structure fits your acquisition strategy, I’m interested in helping you architect a deal that works for your specific needs.

The Strategic Hybrid: How Broker.com.au Architect Your Deal

Most buyers view the choice between a bank and a vendor as a binary one. However, the most sophisticated acquisitions in 2026 don’t settle for just one path. We specialise in architecting “hybrid funding” structures that utilise a bank loan for 50 to 70 per cent of the purchase price, with the remaining balance covered by vendor finance. This approach is often the most efficient way to navigate the seller financing vs bank loan for business purchase dilemma. It allows you to leverage lower bank interest rates for the bulk of the deal while using the seller’s “skin in the game” to satisfy the bank’s strict equity requirements. When a bank sees that a seller is willing to wait for a portion of their money, it signals immense confidence in the business’s future health, often making the approval process much smoother.

Our role goes beyond simply finding a lender. We provide best-in-class corporate advisory to ensure your deal structure is resilient. By utilising our inside access to a national panel of lenders, including those who understand the value of business goodwill, we help you bridge the gap between your dream acquisition and a funded reality. This strategic modelling ensures that your post-sale cash flow isn’t choked by repayments, giving you the breathing room needed to implement your growth strategy from day one.

The 5-Step Process to a Funded Acquisition

We’ve refined a clear path to move you from uncertainty to a place of streamlined confidence. This structured approach removes the anxiety often associated with high-stakes finance.

- Initial Discovery: We begin by assessing your current borrowing power and conducting a deep dive into the target business’s financial health.

- Strategic Modelling: Our experts determine the ideal split between bank debt and vendor notes to maximise your cash flow.

- Lender Selection: We access our national panel to find the specific bank or non-bank lender that fits your industry and deal size.

- Negotiation Support: We assist you in “selling” the hybrid structure to the vendor, explaining why it facilitates a faster, more secure exit for them.

- Seamless Settlement: We manage the heavy lifting of the paperwork, using AI-driven applications to ensure a stress-free close.

Why an Expert Broker is Your Best Asset

Buying a business is one of the most significant financial moves you’ll ever make. You shouldn’t have to manage the complexities of credit policies and PPSR registrations alone. We act as your expert guide, handling the intense bank negotiations while you focus on the practicalities of the business handover. Our goal is to move you toward a feeling of relief, knowing that your acquisition is backed by a professional team and a tailored strategy. If you’re ready to secure your next venture with a structure that protects your equity, I’m interested in a tailored finance strategy to help you get started.

Secure Your Acquisition with Streamlined Confidence

Choosing between seller financing vs bank loan for business purchase doesn’t have to be a source of anxiety. The most successful Australian acquisitions in 2026 leverage a hybrid approach, blending the lower interest rates of traditional lenders with the flexible, risk-sharing nature of vendor notes. By structuring your deal correctly, you protect your personal equity and ensure the departing owner remains committed to a seamless handover. Whether you’re navigating the complexities of the PPSR or seeking to avoid cross-collateralising your family home, the right architecture makes all the difference.

As award-winning business loan specialists, we provide inside access to over 50 Australian lenders and use proprietary AI technology to accelerate your approval. You don’t have to handle the heavy lifting of financial modelling and bank negotiations on your own. We’re here to guide you through every step, moving you from a state of uncertainty toward a funded, successful future. If you’re ready to take the next step in your entrepreneurial journey, I’m interested in exploring my finance options. Your ideal business purchase is within reach, and we’re here to make sure you’re in good hands.

Frequently Asked Questions

Is seller financing legal in Australia for business purchases?

Yes, seller financing is entirely legal and a common practice across Australia. It involves a private contractual agreement where the vendor agrees to receive the purchase price in instalments rather than as a single lump sum at settlement. To protect both parties, these arrangements should be documented by a solicitor and the security interest registered on the Personal Property Securities Register (PPSR).

What interest rate should I expect for a business acquisition loan in 2026?

In the current 2026 market, bank interest rates generally range from 7.91 per cent to 9.81 per cent per annum, depending on your collateral and the lender. For example, Westpac’s Small Business Loan Rate sits at 7.91 per cent while BankSA’s Commercial Base Rate is 9.81 per cent. If you choose vendor finance, expect to pay a premium, with rates typically ranging between 6 per cent and 15 per cent.

Can I combine a bank loan with seller financing in the same deal?

You can certainly combine both, and many lenders actually encourage this hybrid approach. Using a seller financing vs bank loan for business purchase strategy in tandem helps bridge valuation gaps and reduces the bank’s risk. When a seller retains a financial interest in your success, it gives the bank more confidence to approve the remaining 50 to 70 per cent of the funding.

What happens if I default on a seller finance agreement?

If you default, the consequences depend on the specific terms of your vendor note and security registrations. If the seller has registered a security interest on the PPSR, they may have the legal right to repossess business assets or even take back control of the company. It’s vital to have a clear “Right of Offset” clause to protect yourself if the seller breached warranties before the default occurred.

Do I need to put my house up as security for a business loan?

Not necessarily, as there are several ways to fund an acquisition without risking your family home. While banks often prefer real estate as collateral to offer lower rates, we provide inside access to unsecured business loans and asset finance options. These structures focus on the business’s cash flow and equipment rather than your personal property, keeping your home equity protected.

How long does it take to get a business acquisition loan approved through a broker?

While traditional bank applications can drag on for up to eight weeks, our proprietary AI technology and expert guidance can significantly trim this timeline. Most well-prepared applications reach a formal approval stage within two to four weeks. Having professional financial modelling ready at the start of the process is the most effective way to ensure a seamless and fast result.

What is an earn-out and how does it protect me as a buyer?

An earn-out is a financing structure where a portion of the purchase price is only paid if the business hits specific profit targets after the sale. This protects you from paying for “inflated” historical earnings that don’t materialise once you take over. It keeps the seller motivated to provide a thorough handover and ensures the price you pay reflects the actual value of the business under your management.

Why would a seller agree to finance the person buying their business?

Sellers often agree to finance a buyer to achieve a higher total sale price or to secure a faster exit in a competitive market. It’s a strategic tool that helps them find a suitable successor when traditional bank funding is difficult for a buyer to obtain. Additionally, it can provide the seller with a steady stream of interest income at rates higher than they would receive from a standard bank deposit.