What if the biggest risk to your 2026 financial strategy isn’t a potential rate hike, but the way your debt is currently structured? With the RBA holding the cash rate at 4.35% in June, many borrowers feel a temporary sense of relief, yet the latest interest rate predictions Australia is seeing suggest we aren’t out of the woods just yet.

It’s understandable if you’re feeling overwhelmed by the conflicting signals coming from the major banks. You’re likely balancing the rising costs of business operations with the need for stable debt servicing, all while Westpac forecasts a climb to 4.85% and other lenders suggest cuts are still a year away. We’re here to provide the professional insight you need to move from a state of uncertainty toward streamlined confidence.

This article delivers a comprehensive look at the RBA’s likely trajectory and the specific forecasts from the Big Four. You’ll also discover how recent policy changes like the permanent instant asset write-off can improve your cash flow. By the end, you’ll have a clear, actionable plan to protect your finances and secure a long-term debt structure that works for your unique goals.

Key Takeaways

- Understand the RBA’s current “wait-and-see” stance and why the 4.35% cash rate might remain steady despite slowing GDP growth.

- Compare the latest interest rate predictions Australia’s big four banks are signalling, from Westpac’s hike warnings to CBA’s more optimistic 2027 relief timeline.

- Identify the factors beyond the cash rate, such as international bond markets, that could trigger an out-of-cycle rate increase on your facilities.

- Learn how to restructure high-interest debt into a single, managed facility to improve your monthly cash flow and business resilience.

- Discover how working with an expert guide provides inside access to tailored rates and finance solutions that aren’t available on the open market.

Table of Contents

- The 2026 Interest Rate Landscape: Where We Stand Now

- Big Four Bank Predictions: Comparing CBA, NAB, ANZ, and Westpac

- Beyond the Cash Rate: Why Your Rate Might Move Anyway

- Strategic Debt Management for Business Owners in 2026

- How an Award-Winning Broker Navigates the Noise

The 2026 Interest Rate Landscape: Where We Stand Now

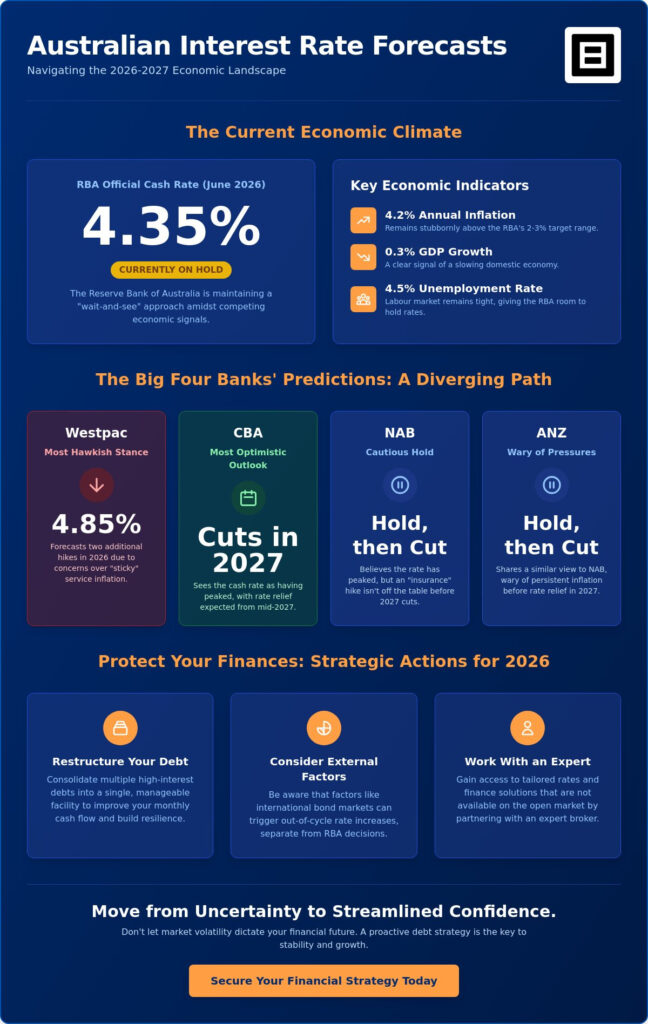

The Australian economic climate in 2026 has been defined by a stubborn tug-of-war between cooling growth and persistent price pressures. Following three successive hikes in the first half of the year, the Reserve Bank of Australia (RBA) opted to hold the official cash rate at 4.35% during its June 16 meeting. This pause offered a moment of quiet for households and businesses, but it remains a fragile peace. While the 0.3% GDP growth recorded in the March quarter suggests the economy is slowing, the RBA’s primary mandate of price stability means they won’t pivot to rate cuts until inflation is firmly back within the 2 to 3% target range.

Current interest rate predictions australia wide are heavily influenced by global factors that remain outside of local control. Volatility in the Middle East and ongoing international supply chain disruptions have kept petrol and energy prices high, contributing to an annual inflation rate of 4.2% as of April 2026. For the RBA, these “cost-push” factors are particularly difficult to manage. Raising rates doesn’t lower the global price of oil, yet the central bank must ensure these high costs don’t become embedded in local wage and price expectations. This leaves the June “hold” looking more like a high-altitude plateau than the start of a downward slope.

Inflation vs. Employment: The RBA’s Balancing Act

The RBA is currently walking a narrow path between curbing inflation and protecting the labour market. With the unemployment rate sitting at 4.5% in April 2026, the market is still considered tight by historical standards. This resilience in employment actually gives the RBA more “room” to keep rates higher for longer without fearing a total economic collapse. However, with trimmed mean inflation at 3.4%, there’s still a significant gap to close. All eyes are now on the August 11 RBA board meeting, which is shaping up to be the most critical date on the 2026 financial calendar for anyone managing debt.

Current Market Sentiment for Australian Borrowers

Confidence among Australian consumers remains at very low levels as we move through mid-2026. Mortgage stress is no longer a fringe issue; it’s a central reality for the middle-market, where many families are seeing their monthly cash flow evaporate. Business owners are facing a unique double-hit, as they struggle with the rising cost of commercial debt alongside their personal home loans. Relying on a “hope for a hike” or waiting for an imminent cut is becoming a dangerous strategy. With corporate insolvencies trending above pre-pandemic levels in the construction and retail sectors, proactive debt management is the only way to move from uncertainty to streamlined confidence.

Big Four Bank Predictions: Comparing CBA, NAB, ANZ, and Westpac

The current divergence among the major banks has created a complex environment for borrowers. While the RBA’s official cash rate target sits at 4.35%, the path forward is far from unanimous. CBA, NAB, and ANZ generally agree that the cash rate has reached its peak, with expectations for rate relief to begin in 2027. CBA remains the most optimistic of the group, eyeing mid-2027 for the first significant downward move. Conversely, Westpac has taken a more hawkish stance, forecasting two additional hikes in 2026 that could see the rate climb to 4.85%. This split highlights why interest rate predictions australia wide are currently so volatile.

NAB and ANZ economists remain wary of persistent price pressures. While their baseline is a hold, they’ve suggested that an “insurance” hike in late 2026 shouldn’t be ruled out if inflation doesn’t retreat toward the target range quickly enough. Despite these differing short-term views, a broader consensus is forming for 2027. Three of the four major banks anticipate that the economic slowdown will eventually force the RBA’s hand, leading to a series of cuts by the middle of next year. This suggests that while the immediate future is bumpy, there’s a light at the end of the tunnel for those who can manage their debt through this final plateau.

Why the Experts Disagree

The split in forecasts often comes down to how each bank weights specific economic indicators. CBA and NAB are watching consumer spending data closely, noting that high living costs are finally curbing retail activity. ANZ and Westpac, however, are more concerned with “sticky” service inflation and wage growth, which rose by 3.3% in the year to the March 2026 quarter. When household savings buffers are factored in, some economists believe the economy can withstand higher rates for longer, while others fear a “hard landing” if the RBA doesn’t pivot soon.

What This Means for Your Refinancing Timeline

For many Australian borrowers, this uncertainty leads to analysis paralysis. Waiting for the “perfect” bottom of the market can be a costly mistake, especially if Westpac’s prediction of further hikes proves correct. If you’re managing a home loan or a commercial facility, now is the time to assess your exposure. Timing a transition to a fixed rate or restructuring your debt shouldn’t be a guessing game. If you’re feeling the pressure of current repayments, simply saying “I’m interested” in a professional debt review can provide the clarity you need to move forward with confidence.

Beyond the Cash Rate: Why Your Rate Might Move Anyway

It is a common misconception that your interest rate is tethered solely to the decisions made in Martin Place. While the RBA’s role in monetary policy sets the baseline for the economy, banks frequently make “out-of-cycle” moves. These shifts happen behind the scenes, driven by international bond markets and the rising cost of wholesale funding. If it costs an Australian bank more to source capital from overseas markets, they’ll likely pass those costs on to their customers. This autonomy is a core reason why interest rate predictions australia can be so difficult to pin down for the average borrower, as your local rate might climb even when the official cash rate remains on hold.

There’s also the reality of the “loyalty tax” to consider. Industry data often indicates that existing customers pay approximately 0.5% more than new borrowers on the exact same product. Banks use “front book” discounts to lure new business, while “back book” customers are left on higher legacy rates. Competition for deposits also plays a significant role; when banks are forced to offer higher returns to savers to maintain their capital levels, they often squeeze their lending margins. To balance the books, they may quietly nudge up interest rates for debt holders, regardless of what the central bank is doing.

The Impact of Net Interest Margins (NIM)

Banks are commercial entities with a primary duty to protect their Net Interest Margin (NIM). This is the gap between the interest they pay to depositors and the interest they collect from borrowers. During economic shifts, larger institutions might raise rates to safeguard their profits against rising operational costs. Conversely, smaller, “best in class” lenders often become more aggressive with cuts to steal market share. However, you should always be wary of “honeymoon rates.” These introductory offers look attractive on paper but can revert to much higher costs once the initial period ends, leaving you in a worse position long-term.

Commercial vs. Residential Rate Variance

Business loan rates typically move with more speed and volatility than residential home loans. Lenders apply a specific “risk premium” to products like business acquisition funding or working capital finance based on the current economic climate. In the high-rate environment of 2026, lenders are scrutinising business cases with more intensity than ever. Smart operators are increasingly turning to asset finance to secure essential equipment without draining their liquid reserves. This strategy allows them to preserve cash flow and maintain a sense of streamlined confidence, even when the broader interest rate landscape is shifting beneath their feet.

Strategic Debt Management for Business Owners in 2026

For many Australian business owners, the current economic climate feels like a two-front war. You’re likely managing a residential home loan while simultaneously servicing commercial debt, all while interest rate predictions australia remain split between a long-term plateau and Westpac’s forecast of further hikes. To build genuine resilience, you must move from a defensive posture to a strategic one. Restructuring multiple high-interest debts into a single, managed facility can immediately alleviate the pressure on your monthly cash flow and provide a clearer path to debt reduction.

One powerful tool in this high-rate environment is debt recycling. By carefully structuring your finances, you can effectively turn non-deductible home debt into tax-deductible business debt. This doesn’t just reduce your tax liability; it accelerates your ability to clear personal debt using the resulting savings. Additionally, as we face the risk of a late-2026 hike, a split loan strategy allows you to hedge your bets. By fixing a portion of your debt, you protect yourself against further increases while keeping the remainder variable to benefit from the potential 2027 cuts predicted by CBA and NAB.

Don’t overlook the simple power of offset accounts. With the cash rate at 4.35%, every dollar “parked” in an offset account is essentially earning a tax-free return equal to your lending rate. For a business with seasonal cash flow, this is the most efficient defence against rising debt-servicing costs.

Optimising Business Cash Flow

A Line of Credit serves as a vital safety net, allowing you to access funds only when needed without the immediate interest cost of a standard term loan. If your business is hampered by slow-paying clients, invoice finance can bridge the gap without the need for high-interest working capital loans. With the $20,000 instant asset write-off becoming permanent on July 1, 2026, it’s also an ideal time to review your equipment finance and chattel mortgages. Aligning these facilities with new tax incentives ensures your capital is working as hard as possible.

The “Stress-Free” Refinance Checklist

Refinancing in 2026 involves more than just chasing the lowest headline rate. Lenders now use sophisticated AI-driven models to assess risk, so having your financials organised and up-to-date is essential. You need to compare more than just the interest; look at fees, redraw flexibility, and the lender’s appetite for your specific industry. Because self-employed income is often viewed through a different lens by major banks, working with a specialist who understands these nuances is the key to moving from uncertainty to streamlined confidence. If you’re ready to see how these strategies apply to your specific situation, you can get started with a tailored debt review today.

How an Award-Winning Broker Navigates the Noise

In a climate where interest rate predictions australia are as varied as the lenders themselves, trying to find the right path on your own is exhausting. While Westpac signals further hikes to 4.85% and other majors eye 2027 for relief, the sheer volume of conflicting data can lead to costly hesitation. This is where the Broker.com.au advantage becomes your greatest asset. We utilize proprietary AI to scan the entire market for “best in class” rates, but we don’t stop at the digital surface. Our team provides the inside access you need to uncover tailored finance solutions that often remain hidden from public comparison websites.

Our approach is built on a sophisticated blend of professional authority and reassuring accessibility. We understand that your debt structure isn’t just a series of numbers; it’s the foundation of your business’s future or your family’s security. By moving beyond simple algorithms, we provide a personalised advisory service that prioritises your specific goals. Whether you are looking to secure a commercial property loan or organise equipment finance, our mission is to move you from a state of uncertainty toward streamlined confidence.

The “I’m interested” philosophy is at the heart of everything we do. We don’t believe in high-pressure sales tactics or aggressive “apply now” buttons. Instead, we start with a low-pressure conversation focused on your needs. This human-led advisory ensures you feel in good hands from the very first interaction, making the entire refinancing or lending process feel completely stress-free.

The Human Element in a Digital World

While our technology is elite, our people are the true “high-level fixers” for your finance needs. Experts like Matt, Kylie, and the wider team provide local insights with a national reach, ensuring you benefit from an exclusive advantage. We’ve helped countless business owners save thousands by restructuring complex debt portfolios that other brokers found too difficult to handle. For those involved in business acquisition funding or intricate M&A scenarios, our corporate advisory service acts as a seasoned partner, managing the technical modelling and lender negotiations so you can focus on your core operations.

Your Next Steps to Rate Security

The best defence against market volatility is preparation. You can use our repayment calculators to model various “what-if” scenarios, such as how your cash flow would be affected if the August 11 RBA meeting results in a hold or a hike. Once you have a feel for the numbers, a 15-minute discovery call with our team is the most efficient way to gain clarity. We will discuss your current debt structure, your long-term dreams, and how we can provide the inside access you deserve. If you are ready for a professional, stress-free review of your finances, I’m interested in seeing my options and securing a more resilient financial future.

Taking Control of Your Debt in a Volatile 2026

The 2026 economic landscape is one of careful navigation. The RBA’s decision to hold the cash rate at 4.35% provides a temporary pause, but the underlying volatility in global markets and domestic inflation suggests that stability is far from guaranteed. Whether you’re a business owner managing commercial property loans or a homeowner looking to protect your cash flow, the divergence in interest rate predictions australia underscores the need for a tailored, professional strategy rather than a passive approach.

You don’t have to face this uncertainty alone. At Broker.com.au, we provide Award-Winning Finance Solutions that move you from complexity to streamlined confidence. By using our proprietary AI for market-leading accuracy and leveraging inside access to over 50+ Australian lenders, we find the “best in class” facilities that simply don’t appear on standard comparison sites. If you’re ready to move beyond the noise and secure your long-term debt structure, I’m interested in a debt review. Our low-pressure conversations are designed to put your dreams first, ensuring you’re in good hands for whatever the economy signals next.

Frequently Asked Questions

Will the RBA cut interest rates in 2026?

Current forecasts suggest that a rate cut in 2026 is unlikely. While CBA and NAB anticipate relief could arrive by mid-2027, the RBA remains focused on bringing inflation back to its 2 to 3% target range. These interest rate predictions australia is currently seeing indicate a “higher for longer” plateau is the most probable path for the remainder of the year.

What is the current RBA cash rate in Australia?

The official cash rate is currently 4.35%. This rate was held steady at the RBA board meeting on June 16, 2026. Borrowers should keep a close eye on the next scheduled meeting on August 11, 2026, as the board continues to assess the impact of persistent service inflation and global economic volatility.

How much will my repayments increase if rates go up by 0.25%?

On a standard 30-year home loan, a 0.25% increase typically adds between $15 and $20 per month for every $100,000 of debt. For a $600,000 mortgage, this results in an additional monthly cost of approximately $90 to $120. Business owners with larger commercial facilities or equipment finance should model these changes carefully to protect their working capital.

Is it better to fix my interest rate now or stay variable?

The choice depends on whether you prioritise certainty or flexibility. Fixing your rate now offers protection against the further hikes predicted by Westpac, ensuring your repayments remain stress-free. Conversely, a variable rate allows you to benefit immediately if the RBA moves toward cuts earlier than 2027. Many borrowers find a split loan provides the best of both worlds in an uncertain climate.

What are the Big Four banks predicting for the end of 2026?

The major banks are currently split in their outlooks. CBA, NAB, and ANZ predict the cash rate has peaked at 4.35% and will remain at this level through the end of 2026. Westpac takes a more hawkish view, forecasting two additional hikes that would see the rate reach 4.85% before the year concludes.

How does the RBA decision affect business loans differently than home loans?

Business loan rates are often more sensitive to market shifts and can move faster than residential mortgage rates. Lenders apply a specific risk premium to commercial products like business acquisition funding or unsecured business loans. This means your commercial rates might increase due to rising lender funding costs even if the RBA decides to hold the official cash rate steady.

Can I refinance if my property value has stayed flat?

Yes, refinancing is still possible provided you maintain sufficient equity in your property. Most lenders offer their most competitive “best in class” rates to borrowers with a Loan-to-Value Ratio (LVR) of 80% or less. If your property value hasn’t grown, an expert guide can help you find lenders with more flexible valuation criteria or tailored products for self-employed individuals.

What is debt recycling and can it help me in a high-interest environment?

Debt recycling is a strategy that involves converting non-deductible debt, such as a home loan, into tax-deductible debt for business or investment purposes. In a high-interest environment, this improves your tax efficiency and helps you clear personal debt faster. It is an efficient way to manage your overall debt portfolio while maintaining streamlined confidence in your long-term financial structure.