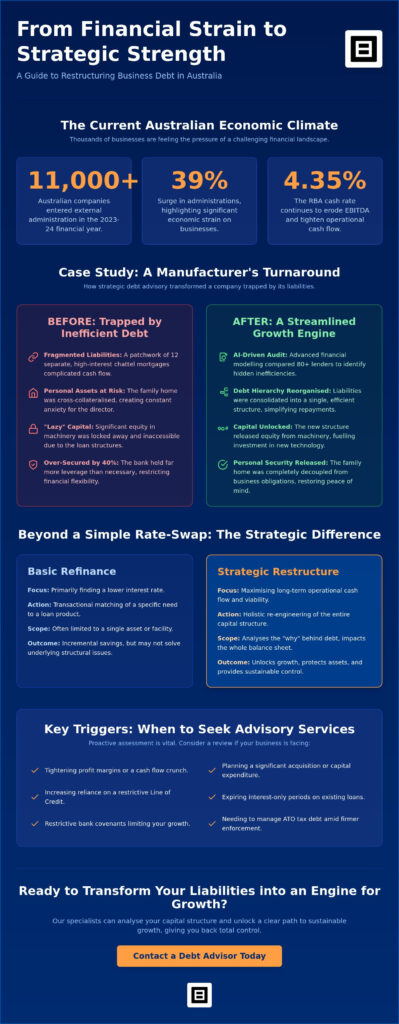

With over 11,000 Australian companies entering external administration in the 2023-24 financial year, a 39% surge that highlights the current economic strain, many directors feel they’re walking a financial tightrope. It’s exhausting to watch your EBITDA eroded by high interest rates while the RBA holds the cash rate at 4.35%. If you’re currently wrestling with restrictive bank covenants or the constant worry of cross-collateralised personal assets, you’re not alone in your frustration. Engaging professional debt advisory services is often the turning point where a business stops merely surviving and begins to thrive again.

We understand that your business is more than just a balance sheet; it’s your life’s work. This article demonstrates how the right strategic approach can transform complex liabilities into a streamlined engine for sustainable growth. We’ll walk through a real-world restructuring scenario to show you exactly how to lower your cost of capital, release personal security, and organise your repayment structures to give you back total control of your future.

Key Takeaways

- Learn how to pivot from defensive finance to proactive growth by reorganising liabilities to unlock immediate liquidity.

- Discover how specialist debt advisory services help you navigate RBA volatility while decoupling personal assets from business obligations.

- Explore a case study of an Australian manufacturing firm that successfully consolidated fragmented high-interest debt into a single, efficient structure.

- Master the distinction between a basic interest-rate refinance and a strategic restructure designed to maximise your operational cash flow.

- Access a clear roadmap for preparing your balance sheets and growth targets to ensure your business is ready for a capital injection.

Table of Contents

- Understanding Debt Advisory Services in the Australian Market

- Case Study: Restructuring for Growth and Asset Protection

- Comparing Debt Advisory Strategies: Restructure vs. Refinance

- Preparing Your Business for Debt Advisory

- Why Broker.com.au is Your Strategic Debt Partner

Understanding Debt Advisory Services in the Australian Market

In the current Australian economic climate, the term “debt” often carries a heavy emotional weight. However, at its core, debt is a tool that requires precise calibration to remain effective. Professional debt advisory services represent the strategic reorganisation of a company’s liabilities to improve liquidity and ensure long-term viability. This isn’t about simply finding the lowest rate. It’s about engineering a capital structure that supports your specific operational goals. With the Reserve Bank of Australia holding the official cash rate at 4.35% as of June 2026, many businesses find their existing arrangements are no longer fit for purpose. Relying solely on a legacy banking relationship can be limiting; traditional lenders are bound by their own internal risk appetites and narrow product suites. An independent advisor acts as a high-level fixer, bridging the gap between your balance sheet and a network of over 80 lenders to find the most efficient path forward. While some may initially look for basic credit counseling services to manage immediate pressure, strategic advisory goes much deeper into corporate structure and growth modelling.

The Difference Between a Broker and a Debt Advisor

It’s helpful to distinguish between a standard finance broker and a strategic advisor. A broker typically facilitates a transaction, matching a specific need to a loan product. In contrast, an advisor structures the overarching strategy. They look at the “why” behind the debt. This involves providing “inside access” to non-bank lenders and private capital markets that aren’t visible to the general public. For complex corporate debt, having an expert guide is critical. They don’t just fill out forms. They rebuild the debt hierarchy to release personal security and improve your EBITDA. This proactive approach transforms a liability into a streamlined engine for growth.

When Should a Business Seek Strategic Advisory?

Timing is everything. You shouldn’t wait for a crisis to evaluate your position. A “cash flow crunch” often reveals itself through subtle signs, such as tightening margins or an increasing reliance on a restrictive Line of Credit. If you’re planning a business acquisition or significant capital expenditure, a proactive review of your current facilities is essential. With the ATO taking a firmer stance on enforcement in 2026, managing tax debt or preparing for expiring interest-only periods requires a sophisticated approach. Moving early allows you to transition from a state of uncertainty to one of streamlined confidence. Professional debt advisory services provide the clarity needed to make high-stakes decisions without the usual anxiety.

Case Study: Restructuring for Growth and Asset Protection

Consider the case of a mid-sized Victorian manufacturing firm, let’s call them Precision Engineering, that recently faced a common Australian hurdle. They had grown rapidly, but their balance sheet was a patchwork of twelve separate high-interest chattel mortgages and a restrictive Line of Credit. The owner felt trapped. Every time he wanted to invest in new technology, the bank tightened its grip on his personal assets. This cross-collateralisation meant his family home was effectively held hostage by the business’s daily operations. This is where professional debt advisory services move beyond simple brokerage to become a true growth partner. The emotional toll of having a family’s security tied to a fluctuating EBITDA cannot be overstated; it creates a state of persistent anxiety that clouds strategic decision-making.

The Audit Phase: Uncovering Hidden Inefficiencies

Our audit began with a deep dive using advanced financial modelling to identify “lazy” capital. We found that while the business had significant equity in its machinery, the fragmented nature of its equipment finance meant that capital was locked away. By reviewing the Simplified debt restructuring process framework, we identified opportunities to streamline their obligations without triggering the penalties the owner feared. We didn’t just look at the rates. We used AI-driven analysis to compare their existing loan terms against the broader market of over 80 lenders. This process highlighted that they were over-secured by nearly 40%, giving the bank far more leverage than was necessary for the risk involved.

The Solution: Tailored Debt Refinancing

The fix involved a complete reorganisation of their debt hierarchy. We moved the firm away from rigid secured business loans and into a more fluid Working Capital Finance facility. By leveraging our inside access to Tier 2 lenders who understand the manufacturing sector better than the big four banks, we negotiated terms that prioritised cash flow over rigid collateral requirements. This wasn’t just a simple swap; it was a high-level fix that required precise negotiation of new bank covenants. The result was a 15% reduction in monthly debt service costs and, most importantly, the full release of the owner’s family home from the security pool. Precision Engineering transitioned from a defensive posture to a proactive one. If you feel your current structure is holding you back, you might be surprised by how much equity is actually available when you get started with a professional review of your facilities. Professional debt advisory services ensure you are in good hands, moving you from a state of complexity toward streamlined confidence.

Comparing Debt Advisory Strategies: Restructure vs. Refinance

Many Australian directors use the terms “refinancing” and “restructuring” interchangeably, but they represent very different financial outcomes. A refinance is essentially a product swap. You replace an existing loan with a new one to capture a lower interest rate or better features. It’s a reactive move, often driven by a desire to trim monthly costs. In contrast, restructuring is a proactive, strategic overhaul of your entire debt hierarchy. This is where professional debt advisory services provide the most value. Restructuring focuses on optimising cash flow and aligning your liabilities with your 12-month growth objectives. While a refinance might save you a few basis points, a restructure can fundamentally change your business’s ability to scale by unlocking working capital previously trapped in rigid loan terms.

The choice between these strategies depends heavily on your business lifecycle. A mature, stable company with predictable revenue might only need a simple refinance to maintain efficiency. However, a firm in a rapid growth phase or one navigating an acquisition needs a restructure. This might involve using Asset Finance to leverage existing machinery or fit-outs, effectively balancing the balance sheet without exhausting cash reserves. Understanding what to look for in a debt advisory service is vital when making this distinction, as the wrong path can leave you with a lower rate but equally restrictive conditions.

The Pros and Cons of Debt Consolidation

Consolidating multiple facilities into a single, streamlined structure offers several advantages, but it isn’t a universal fix. Within the Australian regulatory framework, debt consolidation is defined as the process of combining multiple high-interest obligations into a single loan facility to simplify management and potentially reduce the total interest burden. The pros are clear: you gain better visibility over your commitments and often enjoy lower monthly repayments. However, you must consider the cons. Exit fees on existing chattel mortgages or business loans can be significant. Stretching short-term debt over a longer term might also increase the total interest paid over the life of the loan. A strategic advisor helps you calculate the “break-even” point to ensure the move makes financial sense.

The Importance of Covenant Management

Bank covenants are the “tripwires” of your finance agreement. If you breach your Debt-to-Equity ratio or fall below a certain Interest Cover requirement, the lender can call in the loan. As the RBA holds the cash rate at 4.35%, these ratios are under more pressure than ever. Our role as an expert guide is to stress-test your business against future rate rises before you sign a new agreement. We work to negotiate more “founder-friendly” terms with alternative lenders who offer more flexibility than traditional banks. By proactively managing these covenants, we move you away from the anxiety of a potential breach and toward a state of streamlined confidence. Professional debt advisory services ensure your debt remains a tool for progress, not a source of constant risk.

Preparing Your Business for Debt Advisory

Transitioning from financial uncertainty to a position of strength requires more than just a desire for change; it demands rigorous preparation. When you engage debt advisory services, the quality of your initial data determines the speed and success of the outcome. Think of this phase as building a “data room” that tells the story of your business’s resilience and potential. Lenders don’t just look at where you’ve been. They want to see where you’re going and how you plan to get there. By organising your records early, you reduce the inherent anxiety of the process and move toward a state of streamlined confidence.

- Step 1: Organise your financial statements. Ensure your P&L, Balance Sheet, and Aged Receivables are current. Clean data is the foundation of trust with any new lender.

- Step 2: Define your 12-month growth objectives. Be specific about your capital needs. Are you funding a business acquisition, purchasing new equipment, or seeking a more flexible Line of Credit?

- Step 3: Identify all existing collateral. List every asset currently tied to a loan, including personal guarantees. This helps your advisor identify opportunities to release security, as seen in our earlier case study.

- Step 4: Engage a specialist. Partner with a broker who possesses deep corporate advisory experience and “inside access” to the Australian lending landscape.

The Role of Technology in Modern Debt Advisory

Gone are the days of manual spreadsheets and weeks of waiting. We use AI-driven technology to accelerate the preparation of your lender submission. These digital tools allow us to stress-test your financials against the criteria of 80+ lenders in minutes. This efficiency ensures that when we approach a Tier 2 or alternative lender, the application is accurate and tailored. It also protects your credit score by avoiding multiple “hard” credit enquiries that can occur when you shop around blindly. This streamlined approach moves you closer to your “dream” outcome with minimal friction.

Common Pitfalls to Avoid

The most dangerous mistake is waiting too long. Many directors fall into the “too little, too late” trap, seeking help only when a cash flow crunch becomes a full-blown crisis. With the ATO taking a firmer stance on enforcement as of June 2026, failing to disclose tax liabilities or contingent debts can derail a restructuring plan instantly. You must also be wary of the fine print. Ignoring early exit penalties on existing chattel mortgages can turn a seemingly good refinance into a costly mistake. If you’re ready to move toward a more efficient capital structure, it’s time to get started with a professional review of your current facilities. Specialist debt advisory services ensure you’re in good hands, providing the high-level fixing required for complex corporate needs.

Why Broker.com.au is Your Strategic Debt Partner

Broker.com.au isn’t just another digital portal. We’re an award-winning Australian firm that bridges the gap between sophisticated financial modelling and genuine human empathy. Our debt advisory services leverage proprietary AI-driven efficiency to scan the market, yet every strategy is fine-tuned by a seasoned professional who understands the local landscape. This unique blend ensures you get the speed of modern technology without losing the boutique level of personal attention your business deserves. Whether you need a complex Line of Credit, Invoice Finance to smooth out cash flow, or specialised SMSF Loans, we provide inside access to structures that traditional banks often overlook.

Our “I’m interested” approach is designed to be the start of a low-pressure conversation rather than a high-stakes sales pitch. We know you’re likely tired of the banking run-around and the anxiety of restrictive covenants. Our goal is to move you toward a state of streamlined confidence by acting as a high-level fixer for your balance sheet. We don’t just find a loan; we engineer a path to relief.

Best-in-Class Finance Solutions

You’re never just a file number here. When you work with us, you’re in good hands with experts like Matt, Kylie, and Flavio. They act as your Expert Guide, navigating the complexities of the Australian lending market to find a tailored fix for your specific needs. Remember Precision Engineering, the manufacturing firm we discussed earlier? Today, they’re a thriving enterprise. By releasing their family home from the security pool and consolidating their fragmented debt, they’ve expanded their operations and reclaimed their peace of mind. That’s the tangible result of a strategy that prioritises the founder’s needs over the bank’s rigid requirements.

Take the Next Step Toward Financial Relief

Starting the process is straightforward and entirely stress-free. You don’t need to have every answer right now; you just need a partner who knows where to look. We’ll handle the heavy lifting, from data room preparation using our AI tools to final negotiations with alternative lenders. It’s time to stop feeling trapped by your liabilities and start using your capital as a tool for your next big dream. Reach out today to see how we can transform your business’s financial future.

I’m interested — Let’s discuss your debt strategy

Transform Your Liabilities into Growth Capital

Navigating the Australian lending landscape requires more than just searching for a lower interest rate. It’s about engineering a structure that protects your personal assets while providing the liquidity needed for your next expansion. By distinguishing between a basic refinance and a strategic restructure, you can effectively decouple your family home from your business obligations and organise a repayment schedule that actually fits your cash flow. Your life’s work deserves a capital structure that supports your vision rather than one that holds you back.

Engaging professional debt advisory services ensures you’re no longer tackling these high-stakes decisions alone. As an award-winning business loan broker, we provide inside access to over 80 Australian lenders and use proprietary AI to achieve 99% application accuracy. This combination of high-level technology and human-led expertise moves you from a state of financial complexity toward a feeling of total confidence. We’re ready to help you turn your current financial challenges into a streamlined engine for future success.

I’m interested in a strategic debt review

Frequently Asked Questions

What exactly are debt advisory services for businesses?

These services involve the strategic reorganisation of a company’s liabilities to improve liquidity and ensure the capital structure aligns with long-term goals. It’s a proactive approach that goes beyond simply finding a loan. Professional debt advisory services focus on engineering a balance sheet that supports growth while minimising the cost of capital and reducing the risks associated with restrictive bank covenants.

How does a debt advisory broker differ from a traditional bank manager?

A bank manager is restricted to the narrow product suite and specific risk appetite of a single institution. In contrast, an independent advisor works for you, providing inside access to a network of over 80 Australian lenders. This allows for a much broader range of solutions, including Tier 2 and alternative lenders who often offer more flexible terms and founder-friendly covenants than the big four banks.

Will debt advisory affect my business credit score?

Engaging an advisor actually helps protect your credit score. Rather than applying blindly to multiple lenders, which creates “hard” enquiries that can damage your rating, we use proprietary technology to match your business with the right lender first. This targeted approach ensures that applications are only submitted when there’s a high probability of success, maintaining your credit integrity throughout the process.

Can debt advisory help with ATO tax debt?

Yes, strategic advisory is a highly effective way to manage and clear ATO obligations. By restructuring existing facilities or introducing new solutions like Invoice Finance or Working Capital Finance, businesses can often settle their tax debt in full. This is frequently a better long-term strategy than a standard ATO payment plan, as it can stop the accrual of high interest and penalties while improving your overall standing with lenders.

Is debt advisory only for companies in financial distress?

Not at all; it’s a powerful tool for growth-oriented companies. While it’s vital for restructuring during a cash flow crunch, many thriving businesses use debt advisory services to fund acquisitions, manage major capital expenditure, or release personal security from the business pool. It’s about capital optimisation at every stage of the business lifecycle, not just during periods of stress.

How long does the debt restructuring process typically take in Australia?

The timeline depends on the complexity of your current debt hierarchy and how quickly you can organise your financial data. A straightforward refinance might be completed in two to four weeks. However, a comprehensive corporate restructure involving multiple lenders and asset classes usually takes between four and eight weeks. Our use of AI-driven tools helps speed up the audit phase to ensure a seamless transition.

What documents do I need to provide for a debt advisory audit?

To begin a professional audit, you’ll generally need your most recent Profit and Loss statements, a current Balance Sheet, and an Aged Receivables report. We also require copies of your existing loan contracts and a clear outline of your 12-month growth objectives. Having this “data room” ready allows us to stress-test your business against the market and identify hidden inefficiencies quickly.

How much do debt advisory services cost for an Australian SME?

Fees for advisory services vary depending on the complexity of the restructure and the total amount of debt being managed. Most businesses find that the costs are significantly offset by the long-term savings achieved through lower interest rates and improved cash flow. We recommend a preliminary conversation to discuss your specific needs; this allows us to provide a clear, tailored outline of the value we can deliver for your business.