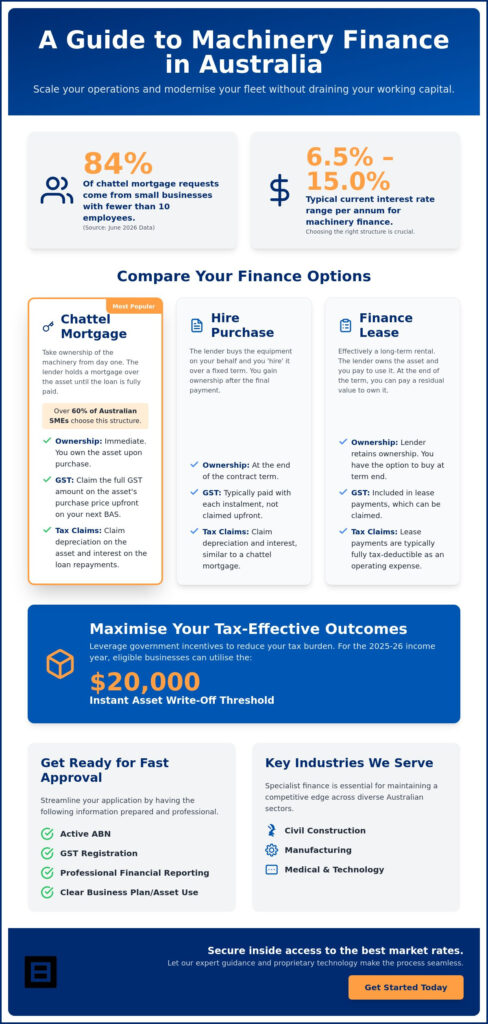

Did you know that 84% of chattel mortgage requests in Australia come from small businesses with fewer than ten employees? This June 2026 data highlights a vital truth: savvy operators aren’t waiting for “perfect” cash reserves to upgrade their fleet. You likely understand the frustration of navigating complex bank applications or the anxiety of high interest rates, which currently range from 6.5% to 15.00% p.a. It’s a high-stakes environment where choosing the wrong structure can feel like a costly mistake. Finding the right machinery finance australia solution shouldn’t be a source of stress.

We’re here to ensure you feel in good hands as you modernise your operations. This guide will show you how to leverage tailored finance to scale your business without draining your precious working capital. We’ll explore how to navigate the $20,000 instant asset write-off threshold for the 2025–26 income year and compare structures like chattel mortgages and hire purchases to find your best fit. You will discover a clear, professional roadmap to securing fast approvals and tax-effective outcomes that move your business forward.

Key Takeaways

- Discover how to leverage machinery finance australia to scale your operations without exhausting your working capital or risking personal assets.

- Compare the unique advantages of chattel mortgages, hire purchases, and leases to select a structure that aligns with your specific cash flow needs.

- Maximise your tax-effective outcomes by navigating the latest 2026 depreciation schedules and instant asset write-off thresholds.

- Streamline your application for fast approval by ensuring your ABN, GST registration, and financial reporting are professional and ready for review.

- Learn how expert guidance and proprietary technology can secure inside access to the best market rates, making the entire process seamless and stress-free.

Table of Contents

- Understanding Machinery Finance in the Australian Business Landscape

- Comparing Finance Structures: Chattel Mortgages, Hire Purchases, and Leases

- Navigating Tax Benefits and Asset Depreciation for 2026

- How to Organise Your Machinery Finance Application for Fast Approval

- Partnering with Broker.com.au for Best-in-Class Asset Solutions

Understanding Machinery Finance in the Australian Business Landscape

At its core, machinery finance australia is a specialised asset finance solution designed to help you acquire industrial, agricultural, or commercial equipment without the burden of a massive upfront payment. It acts as a bridge between your current operations and your future growth. Instead of depleting your cash reserves, you pay for the equipment as it generates revenue for your business. This strategic approach ensures that your liquidity remains intact, allowing you to manage daily expenses like payroll and inventory with total confidence.

The year 2026 has emerged as a pivotal time for Australian businesses to modernise. With technological advancements in automation and energy efficiency accelerating, the cost of operating legacy equipment is often higher than the cost of financing a new, high-performance fleet. While traditional bank loans frequently involve rigid terms and intrusive security requirements, specialist asset finance focuses on the equipment itself. This means you can often secure the funding you need without risking your personal assets or home, providing a much-needed sense of relief and security.

Why Finance Instead of Buying Outright?

Choosing to finance rather than buy outright is about more than just keeping cash in the bank. It’s about avoiding the “opportunity cost” of tied-up capital. If you spend $200,000 on a new harvester or CNC machine today, that money is no longer available to hire new staff, launch a marketing campaign, or cover an unexpected repair. By spreading the cost over several years, you align your outgoings with the income the asset produces. This creates a sustainable cycle where the machine essentially pays for itself while you maintain a healthy buffer for growth.

Common Industries Utilising Machinery Finance

Different sectors across Australia use these tools to maintain a competitive edge. We see diverse applications including:

- Civil Construction: Earthmoving and excavation firms often utilise various finance lease structures to ensure their fleet remains current and compliant with modern safety standards.

- Manufacturing: Industrial processing lines require constant upgrades to improve output. Specialist finance allows for seamless integration of new robotics or packing systems.

- Medical and Technology: From diagnostic imaging machines to high-end servers, these sectors rely on machinery finance australia to access cutting-edge tools that would otherwise be cost-prohibitive.

Whether you’re a small family business or a large-scale operation, having an expert guide to help you choose the right path makes the entire process feel straightforward. You’re not just getting a loan; you’re building a foundation for long-term success.

Comparing Finance Structures: Chattel Mortgages, Hire Purchases, and Leases

Choosing the right path for your machinery finance australia isn’t just about finding the lowest interest rate. It’s about matching the financial structure to your specific tax strategy and cash flow requirements. Most Australian SMEs navigate three primary options: chattel mortgages, hire purchases, and leases. Each carries distinct rules regarding who owns the asset and how the Australian Taxation Office (ATO) views your repayments. Understanding these nuances ensures you remain in good hands and avoid any nasty surprises at tax time.

One of the most critical factors is the treatment of GST. Depending on your choice, you might claim the GST on the purchase price upfront or pay it incrementally over the life of the agreement. Additionally, many businesses opt for a “balloon payment” at the end of the term. This lump sum reduces your monthly instalments, which is excellent for preserving daily working capital, though it does increase the total interest paid over the life of the loan. Balancing these factors is where an expert guide becomes invaluable.

The Chattel Mortgage: Ownership from Day One

The chattel mortgage is the most popular choice in Australia, accounting for over 60% of equipment finance among SMEs. Under this structure, your business takes ownership of the machinery immediately. The lender simply secures the loan by taking a “mortgage” over the asset. This is often the preferred route for ABN holders because you can generally claim the full GST amount on the purchase price in your next Business Activity Statement (BAS). It allows for immediate depreciation claims and interest deductions, making it a powerful tool for businesses looking to offset taxable income quickly.

Finance Leases and Operating Leases

If your industry requires equipment that becomes obsolete quickly, a lease might be your best fit. An operating lease functions much like a long-term rental; you use the machinery for a set period and return it at the end, avoiding the risk of owning outdated technology. Finance leases are slightly different. While you don’t own the asset during the term, you typically have the option to acquire it at the end for a residual value. Lease payments are generally treated as an operating expense (OpEx), which can keep your balance sheet looking lean and professional.

Deciding which path aligns with your 2026 growth targets doesn’t have to be complex. Our team can help you navigate these choices by providing inside access to the best rates and structures tailored to your specific industry needs. Whether you’re looking for the security of ownership or the flexibility of a lease, we ensure the process remains seamless and stress-free.

Navigating Tax Benefits and Asset Depreciation for 2026

Understanding the tax landscape is vital for any business owner looking to modernise their fleet without overextending their budget. For the 2025–26 income year, the Australian Government has maintained specific incentives that make machinery finance australia a powerful driver for growth. By choosing the right finance structure, you don’t just get new equipment; you create a strategic tax shield that can lower your business’s overall taxable income. This sophisticated approach ensures your capital remains focused on expansion while the tax office essentially subsidises your technological upgrades through depreciation and interest deductions.

The interaction between your chosen loan structure and current tax laws is complex. While a broker provides inside access to the best market rates and structures, your accountant ensures these choices align with your broader financial modelling. Working with both professionals ensures you’re in good hands, moving from a state of uncertainty toward streamlined confidence. This partnership is the key to ensuring every dollar spent on interest or principal works as hard as possible for your bottom line.

Maximising the Instant Asset Write-off

For the current 2025–26 financial year, the instant asset write-off threshold is set at $20,000. This applies to small businesses with an aggregated turnover of less than $10 million. To take full advantage, the asset must be first used or installed ready for use by 30 June 2026. If you’re acquiring equipment through a chattel mortgage, you can often claim this deduction immediately, providing a significant boost to your cash flow. Assets costing $20,000 or more aren’t left out; they can be placed into the small business simplified depreciation pool. These assets are depreciated at a rate of 15% in the first income year and 30% in subsequent years, ensuring a steady stream of deductions over the life of the machinery.

Understanding Balloon Payments and Tax

Many businesses utilise balloon payments to keep their monthly repayments manageable during high-growth phases. A balloon payment reduces your monthly financial commitment by deferring a portion of the principal to the end of the term, which consequently increases the total interest charged over the life of the loan. From a tax perspective, this structure can be highly effective. The interest paid on the loan is typically tax-deductible, and because the balloon payment lowers your monthly principal repayments, you preserve more working capital for other tax-deductible business expenses. When the term ends, you can choose to pay out the balloon or refinance it into a new machinery finance australia agreement, allowing you to continue your depreciation benefits on the remaining balance.

- The rule preventing small businesses from re-entering the simplified depreciation regime after opting out is suspended until 30 June 2027.

- Any simplified depreciation pool balance under $20,000 at the end of the 2025–26 year can be fully written off.

- Consulting with an expert guide ensures your balloon payment is set at a level that meets ATO “market value” guidelines.

How to Organise Your Machinery Finance Application for Fast Approval

Securing machinery finance australia in 2026 is a significantly faster process than in previous years. AI-driven credit assessments now allow for rapid verification of your financial position; however, the speed of your approval still depends on how well you’ve organised your paperwork. Before you even look at equipment, ensure your ABN and GST registration are active and accurate. This simple step confirms your status as a professional trading entity and ensures you’re eligible for the tax-effective structures we’ve already explored. When your records are in order, you’re already halfway to a “yes”.

Lenders are increasingly looking for a clear “business case” alongside your numbers. They want to see that the new asset isn’t just a purchase, but a strategic investment that will drive revenue or reduce overheads. When you can demonstrate exactly how a new piece of machinery will improve your output, you move from being a standard applicant to a high-value partner in the eyes of the credit team. This proactive approach alleviates the typical anxiety of high-stakes borrowing and places you in a position of strength.

The Essential Documents Checklist

To ensure your application moves through the system without hitches, you’ll need a professional dossier ready for review. Having these items on hand allows our team to provide that “inside access” to the best rates quickly. Most lenders will require:

- Identification: 100 points of ID for all directors and proof of business ownership.

- Serviceability Evidence: Recent bank statements, typically covering the last six months, to prove consistent cash flow.

- Financial Statements: Up-to-date Balance Sheets and Profit & Loss statements for larger or more complex acquisitions.

- Asset Details: Firm quotes or pro-forma invoices from reputable Australian suppliers that clearly outline the machinery’s specifications.

Low-Doc vs Full-Doc Applications

If you’re a well-established business with a clean credit history, you might qualify for a “low-doc” application. This path allows you to secure machinery finance australia without providing full tax returns or comprehensive financial statements, which is ideal for fast-moving opportunities. The trade-off is often a slightly higher interest rate compared to “full-doc” lending, where you provide every detail of your financial history to secure the most competitive terms available. You can use our equipment finance calculator to test your serviceability and see how different loan amounts might impact your monthly commitments.

Whether you need the speed of a low-doc approval or the precision of a full-doc structure, our expert guides are here to handle the complexity for you. If you’re ready to modernise your fleet with a process that is entirely stress-free, get started with a tailored quote today and let us do the heavy lifting.

Partnering with Broker.com.au for Best-in-Class Asset Solutions

When you choose to secure machinery finance australia through our platform, you’re gaining more than just a loan. You’re accessing a sophisticated engine powered by proprietary technology that scans a panel of over 40 lenders. This network includes everyone from the big four banks to boutique financiers who specialise in niche industrial asset classes. Our award-winning team acts as your expert guide, handling every technical hurdle so you can keep your focus entirely on scaling your operations. We take pride in being high-level fixers who can navigate situations that fall outside the norm, ensuring your business never misses a growth opportunity.

We believe that high-stakes financial decisions don’t have to be overwhelming. By moving the complexity of the Australian lending landscape into our hands, you can transition from a state of uncertainty to one of streamlined confidence. Whether you’re looking for specialised equipment or a broader fleet upgrade, our goal is to make the entire process feel seamless and professional. You’re in good hands with a partner who prioritises your specific dreams and operational needs over simple transactions.

Inside Access to Competitive Rates

Our value lies in the “inside access” we provide to the Australian market. Because of our deep-seated industry relationships, we often unlock doors and rates that aren’t available to the general public. We don’t just find a generic product; we tailor a finance structure that mirrors your business’s specific seasonal cycles and cash flow patterns. This long-term advisory approach ensures that your machinery finance australia remains a strategic asset rather than a liability as your business evolves through 2026 and beyond. We look for the best-in-class solutions that provide the most significant advantage for your unique circumstances.

Get Started with a Low-Pressure Conversation

We understand that you’re looking for expert insights, not a high-pressure sales pitch. That’s why we invite you to start with a low-pressure conversation. Our process is designed to be human-led; you’ll work with dedicated team members who understand the nuances of your industry and the local Australian landscape. From your initial enquiry to the moment your machinery is delivered and ready for use, we ensure every step is efficient, transparent, and entirely stress-free. We handle the paperwork and the lender negotiations, providing you with a clear path to resolution.

If you’re ready to see how a strategic partnership can transform your fleet and preserve your working capital, I’m interested in exploring machinery finance options and discovering a more professional way to grow your Australian business.

Driving Your Business Forward in 2026

Modernising your fleet is no longer just an operational choice; it’s a strategic move to secure your competitive edge. By mastering the nuances of machinery finance australia, you can align your asset acquisition with your revenue cycles and take full advantage of current tax incentives. Whether you opt for the immediate ownership of a chattel mortgage or the flexibility of a lease, the right structure ensures your working capital remains ready for the next big opportunity. You don’t have to navigate these technical decisions alone.

As an award-winning business loan broker, we provide inside access to a panel of over 40 Australian lenders. Our proprietary AI-driven application technology streamlines the entire journey, moving you from a state of complexity to one of total confidence. If you’re ready to transform your equipment into a growth engine while keeping the process entirely stress-free, I’m interested in machinery finance solutions. We’re here to help you realise your vision with a partner who prioritises your success. Your business’s future is in good hands.

Frequently Asked Questions

What is the difference between machinery finance and a standard business loan?

Machinery finance uses the equipment itself as security, whereas a standard business loan often requires broader collateral like property. This structure means you don’t have to risk your family home or other personal assets to secure funding. Because the loan is tied to the asset, lenders can often offer more competitive rates and terms than they would for a generic unsecured loan.

Can I get machinery finance for used or second-hand equipment in Australia?

You can certainly finance used or second-hand equipment through machinery finance australia providers. Most lenders will approve gear from reputable dealers or private sellers, provided the asset’s age doesn’t exceed certain limits; usually ten to fifteen years by the end of the loan term. It’s an excellent way to access high-quality machinery at a lower entry price while still enjoying tax-effective structures.

How long does the approval process typically take for machinery finance?

Approval for machinery finance australia is often remarkably fast, frequently taking between 24 and 48 hours for standard applications. Our use of proprietary technology and AI-driven assessments streamlines the verification process, allowing for rapid credit decisions. If your ABN and financial records are organised as discussed in our application guide, you could move from initial enquiry to machinery delivery in just a few business days.

What is a balloon payment, and should I include one in my machinery loan?

A balloon payment is a pre-determined lump sum you pay at the end of your loan term. Including one is a strategic way to lower your monthly repayments, which helps preserve your daily working capital for other operational needs. While it increases the total interest paid over the life of the loan, it provides the breathing room many businesses need to scale up their revenue before the final payment is due.

Are there specific tax benefits for machinery finance in the 2026 financial year?

The 2026 financial year offers specific benefits including the $20,000 instant asset write-off for eligible small businesses. Assets exceeding this threshold can be placed into a simplified depreciation pool, allowing for a 15% deduction in the first year and 30% thereafter. These rules, combined with interest and GST claimable on chattel mortgages, make financing a highly tax-effective way to modernise your fleet.

Do I need to provide a deposit for machinery finance?

You don’t always need a deposit; 100% finance is quite common for established Australian businesses with a strong credit history. This allows you to acquire the machinery you need without any initial capital outlay, keeping your cash reserves intact for unexpected opportunities. Some lenders might request a 10% to 20% deposit for specialised assets or if your business has been trading for less than two years.

Can I finance machinery if my business is a new start-up?

Financing is available for new start-ups, though lenders typically view these applications with more scrutiny. You’ll likely need to provide a solid business plan, a clean personal credit history, and potentially a larger deposit to mitigate the lender’s risk. Being in good hands with an expert guide can help you present a professional case that highlights your industry experience and projected cash flow.

What happens if I want to upgrade my machinery before the loan term ends?

You can upgrade your machinery before the loan term ends by either paying out the remaining balance or refinancing into a new agreement. This is a common strategy for businesses in fast-moving sectors where technology becomes obsolete quickly. We can help you navigate the payout figures and structure a new facility that incorporates your trade-in value, ensuring your transition to newer gear is seamless and professional.