What’s happening—and when?

The Albanese government has pulled ahead the debut of its expanded First Home Guarantee (part of the broader Home Guarantee Scheme), now kicking off 1 October 2025, instead of the originally planned January 2026 launch.

So, mark your calendars: from early October, all first-home buyers across Australia can step into the property market with just a 5% deposit, minus the sting of Lender’s Mortgage Insurance (LMI)—which the government will guarantee a chunk of.

What’s the deal for buyers?

1. Low deposit, no LMI

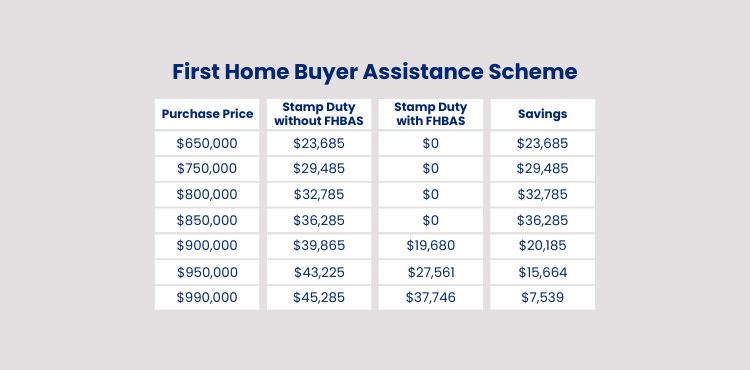

First-home buyers now need only 5% of the purchase price as a deposit. The federal government guarantees up to 15% of the loan, meaning no Lenders Mortgage Insurance—a cost that traditionally adds tens of thousands to your loan.

2. No more limits

Gone are the days of income caps, regional restrictions, or limited program spots. This scheme is open to all eligible first-home buyers—no income threshold, no application ceiling.

3. Upped property price caps

Property price caps have been elevated to reflect real-world prices across cities:

- Sydney: up to $1.5 million

- Melbourne: up to $950,000

- Brisbane: around $1 million

…and similar adjustments in other regions.

Step-by-step: How to get in on this from 1 October

- Check eligibility

You’ll need to be an Australian citizen or permanent resident, over 18, and no property ownership in the past 10 years. - Save your 5% deposit (and other upfront costs)

Keep your deposit between 5% and under 20% of the property’s value—use it wisely, and don’t exclude important expenses like stamp duty and legal fees from the calculation. - Find a participating lender

Housing Australia backs the scheme, but you still need to apply through a lender that participates in the First Home Guarantee. - Submit your loan and guarantee application

Once approved, you’ll enter into a loan for 95% of the property price, with the government guaranteeing the remaining 15%. You can start your application here to be ready for October. - Snag your home

The clock starts ticking—usually, you’ll need to make an offer and get the contract signed within a certain period (often 90 days), then finalize your loan.

What this means for you—and the market

For homebuyers: a serious leg-up

Saving a 20% deposit has long been a major hurdle. With only 5% required, and no LMI, this scheme slashes costs and makes homeownership a real possibility—sooner.

For the market: a tricky balance

Boosting access is great—right when demand is already hot in the spring market. Experts warn that inflating buyer demand without matching supply could push prices up sharply:

- A cautious 0.5% price rise (Treasury’s forecast) over six years

- A riskier short-term increase of 3.5% to 6.6% (or even up to 9.9% in some hotspots) per Lateral Economics

Former RBA experts warn this could be like pouring “gasoline on a fire” amid spring market activity, potentially adding 0.5% to home values within just six months.

The bigger picture & lasting legacies

Labor’s push goes beyond deposits. The government is also investing $10 billion to build 100,000 homes for first-home buyers, with construction beginning from 2026–27. This long-term play aims to ease shortages and stabilize prices.

But while that construction pipeline is vital, it takes time—and critics argue that short-term affordability gains could be drowned out by price spikes if supply doesn’t keep pace.

What you should do next (and what to watch)

- Talk to a mortgage broker or lender now—get prepped to apply when the scheme opens on 1 October.

Talk to a mortgage broker or lender now—get prepped to apply when the scheme opens on 1 October. Start your application here. - Make a game plan: get your 5% deposit ready and align your timeframe to lock in a loan and search houses in spring.

- Keep an eye on prices: rising demand could mean stiffer competition, so be ready to act smart (and fast).

- Watch supply-side developments: new homes coming online from 2026 will matter long-term.

Ready to take advantage of the 5% deposit scheme? Apply now through our simple online form here.