Would you believe that a median house in Brisbane now requires over $17,000 more in annual household income to service a mortgage than it did just five months ago? With the RBA cash rate sitting at 4.35 per cent and property values in Sydney and Melbourne dipping slightly in June 2026, many Australians feel stuck in a cycle of financial uncertainty. It’s completely normal to feel anxious about interest rate volatility or the complex new APRA debt-to-income limits that have reshaped the lending landscape this year.

We understand that you want more than just a rough estimate; you need a strategy. This expert guide will teach you how to use a home loan mortgage calculator to forecast your repayments accurately while accounting for hidden costs like LMI and the impact of the latest 2026 regulations. You’ll discover how extra repayments and offset accounts can drastically reduce your interest, giving you the confidence to stop guessing and start property hunting with a clear budget. We’re going to explore the benefit of tailored financial modelling so you can step into your next broker conversation with total clarity.

Key Takeaways

- Learn how to use a home loan mortgage calculator as a strategic compass to navigate 2026 property trends and forecast your repayments with precision.

- Discover the essential data points required for an accurate estimate, including why adding a 2 per cent buffer rate is vital for stress-testing your financial resilience.

- Understand why generic digital tools often fall short for business owners and how professional financial modelling can better reflect your actual borrowing capacity.

- Master the mechanics of offset accounts and extra repayments to shave years off your loan term and save thousands in interest.

- Transition from digital estimates to a tailored strategy by leveraging award-winning broker insights that go beyond simple calculations.

Table of Contents

- Home Loan Mortgage Calculator: Visualising Your Path to Ownership

- Key Inputs: How to Use a Mortgage Calculator Effectively

- Why Generic Calculators Often Miss the Mark for Business Owners

- Strategies to Reduce Your Mortgage Repayments and Interest

- From Calculation to Keys: How Broker.com.au Secures Your Dream

Home Loan Mortgage Calculator: Visualising Your Path to Ownership

Entering the 2026 property market feels like stepping onto a moving target. With the RBA cash rate at 4.35 per cent and capital city values fluctuating, it’s easy to feel overwhelmed by the sheer scale of the commitment. A home loan mortgage calculator serves as more than just a digital abacus; it’s a strategic budgeting tool that transforms abstract anxiety into a concrete action plan. Mortgage calculators are essential for anyone wanting to see how different loan structures, such as Principal and Interest (P&I) versus Interest-Only repayments, will affect their daily cash flow. While P&I loans focus on chipping away at the debt from day one, Interest-Only options might suit investors or those looking for lower initial costs, though they don’t reduce the loan balance over time.

At Broker.com.au, we’ve moved beyond the basic mathematical outputs offered by traditional banks. Our AI-enhanced home loan mortgage calculator provides market-aligned estimates that consider current lending standards and the specific nuances of the Australian landscape. This level of precision helps you visualise your path to ownership without the guesswork, ensuring you’re in good hands before you even attend your first open home.

Why Repayment Frequency Matters

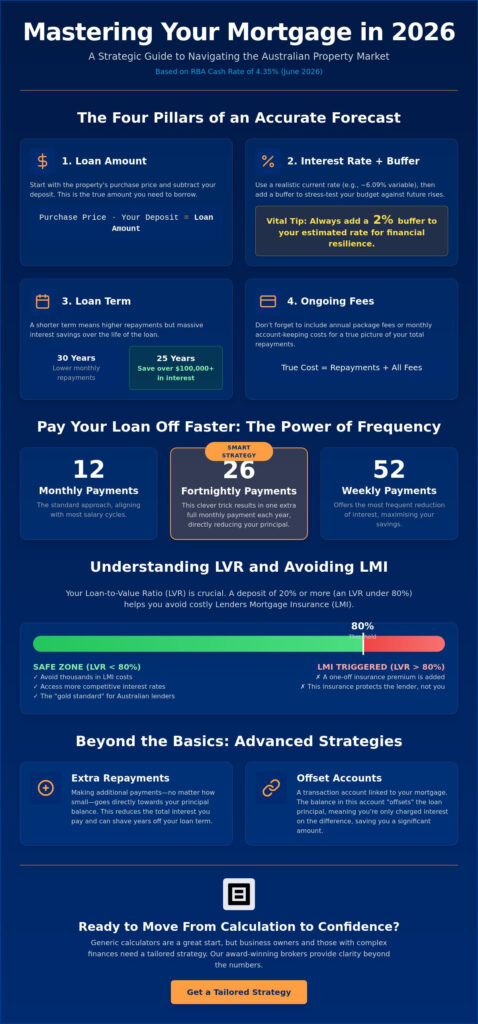

Choosing between monthly, fortnightly, or weekly schedules is a powerful lever for interest savings. Most borrowers default to monthly, but switching to fortnightly can be a game-changer. Consider the following breakdown:

- Monthly: 12 payments per year, matching most salary cycles.

- Fortnightly: 26 payments per year, which effectively equals making 13 monthly payments.

- Weekly: 52 payments per year, offering the highest frequency of interest reduction.

The “hidden” benefit of 26 fortnightly payments is that the extra month goes directly toward the principal. This simple change can shave years off a 30-year term and save you a fortune in compounding interest. It’s a stress-free way to build equity faster without significantly altering your lifestyle.

Understanding the LVR and LMI Thresholds

Your Loan-to-Value Ratio (LVR) is the percentage of the property’s value that you’re borrowing. In the Australian market, staying below the 80 per cent LVR threshold is the gold standard. Once you borrow more than 80 per cent, lenders usually trigger Lenders Mortgage Insurance (LMI). This is a one-off cost that protects the bank, not you. A practical tip for 2026 buyers is to aim for that slightly larger deposit; reaching 20 per cent equity can save you thousands in LMI premiums and often unlocks access to more competitive interest rates.

Key Inputs: How to Use a Mortgage Calculator Effectively

To get the most out of a home loan mortgage calculator, you need to look beyond the basic sticker price of a property. Accuracy is the antidote to anxiety. The effectiveness of your results depends entirely on the quality of the data you input. Start with your total loan amount, but remember to subtract your deposit from the purchase price first. Next, enter a realistic interest rate. With the RBA cash rate sitting at 4.35 per cent as of June 2026, many variable rates from the Big Four banks start around 6.09 per cent. However, we always recommend adding a 2 per cent “buffer” to your calculation. This stress tests your budget against potential future volatility, ensuring you’re in good hands regardless of market shifts.

The loan term is another critical lever. While a 30-year term is the standard for many Australians because it lowers immediate monthly repayments, a 25-year term drastically reduces the total compound interest you’ll pay over the life of the debt. On a typical mortgage in Sydney or Melbourne, that five-year difference can save you well over $100,000. Finally, don’t forget to factor in ongoing costs. Many lenders charge annual service fees or monthly account keeping fees. Including these in your model provides a true cost estimate rather than a best-case scenario.

Fixed vs Variable Interest Rates

The 2026 lending environment offers a complex choice between stability and flexibility. Current data shows 2-year fixed rates as low as 6.29 per cent, while variable rates remain more reactive to RBA decisions. A calculator allows you to compare these paths side by side. Many of our clients opt for a “split loan” structure, which hedges your bets by fixing a portion of the debt for certainty while keeping the rest variable to utilise features like offset accounts. If you’re unsure which path fits your specific financial modelling, speaking with a specialist can help clarify your options.

The Role of the Deposit

Your deposit is more than just a down payment; it’s your ticket to “inside access” for better rates. A larger deposit reduces your LVR, which signals lower risk to the bank and often unlocks tiered pricing discounts. When using your calculator, ensure you’ve set aside a separate cash buffer for upfront costs. Between stamp duty, legal fees, and application charges that range from $150 to $750, these “hidden” expenses can quickly erode your deposit if you haven’t planned for them with professional precision.

Why Generic Calculators Often Miss the Mark for Business Owners

If you run your own show, a standard home loan mortgage calculator can often feel like a blunt instrument. The most common objection we hear from entrepreneurs is: “My income isn’t a simple payslip, so how can I trust these numbers?” It is a valid concern. Most online tools are built for PAYG earners with predictable weekly wages. When your financial life involves company profits, dividends, or director drawings, a generic tool might suggest you can afford much less than your actual capacity allows. This discrepancy often leads to unnecessary stress during the property search.

Lenders typically take a conservative view of business tax returns, but our specialists at Broker.com.au look deeper. We utilise the “Add-back” method to reveal your true borrowing power. This involves identifying non-cash expenses, such as depreciation or significant one-off equipment purchases, and adding them back into your total income. By reframing these figures, we provide a more accurate picture of how much house you can afford. In the 2026 market, where APRA’s debt-to-income limits are strictly enforced, having an expert guide to navigate these “outside of the norm” structures is essential for a successful application.

Low Doc and Alt-Doc Loans for Entrepreneurs

Traditional banks often demand two years of full tax returns before they will even consider a loan. If your recent filings aren’t finalised, a standard home loan mortgage calculator estimate might be discouragingly low. This is where alternative documentation, or Alt-Doc loans, come into play. By using Business Activity Statements (BAS) or six months of bank statements, we can often unlock significantly more borrowing power than a basic web tool suggests. Alt-Doc loans provide a flexible solution for self-employed Australians who need to move quickly in a cooling market.

The Complexity of Trust Structures

Purchasing property through a family or unit trust adds a layer of sophistication that no generic portal can calculate. Trust distributions and the resulting tax implications require a high-level fixer to ensure the debt is structured for maximum efficiency. Our team members, such as Matt or Flavio, provide the corporate advisory needed to align your personal debt with your business goals. They offer local insights and tailored financial modelling that a digital tool simply cannot replicate, ensuring your strategy is robust and your interests are protected.

Strategies to Reduce Your Mortgage Repayments and Interest

Once you have used a home loan mortgage calculator to establish your baseline, the real value lies in manipulating those variables to your advantage. You aren’t locked into a 30-year sentence. By applying strategic pressure to your loan structure, you can dramatically reduce the total interest paid and own your home years sooner. The most effective starting point is the offset account. Every dollar you keep in this linked transaction account is a dollar that isn’t charged interest. If you have a $600,000 loan but keep $50,000 in your offset, the bank only calculates interest on $550,000. It’s a seamless way to maintain liquidity while ensuring your cash works as hard as possible.

For business owners and sophisticated investors, we often discuss the “Debt Recycling” strategy. This involves using equity to pay down non-deductible home debt and replacing it with deductible investment or business debt. It is a high-level move that requires professional oversight, but it can transform your tax position over time. When choosing between an offset account and a redraw facility, keep the tax implications in mind. While redraw facilities allow you to pull back extra repayments, an offset account is usually superior for those who might eventually turn their home into an investment property. To see how these strategies fit your specific goals, you can book a tailored home loan review with our team.

We recommend a “mortgage health check” every 12 to 18 months. The 2026 market is fast-moving, and what was a competitive rate last year might now be eclipsed by new products. Staying proactive ensures you don’t fall victim to the “loyalty tax,” where lenders reserve their best offers for new customers while existing ones pay a premium.

The Impact of Extra Repayments

The “snowball effect” of extra repayments is often underestimated. Even an additional $100 per month can shave years off a standard mortgage. Because interest is calculated daily, reducing the principal balance early in the loan life has a massive compounding benefit. However, always check the fine print on fixed-rate products. Some lenders impose “early exit fees” or limit the amount of extra cash you can tip in each year. A quick check of your home loan mortgage calculator will show you exactly how much time and money a small increase in repayments can save you.

Refinancing for a Better Deal

If your calculator results show a significant gap between your current rate and the market leaders, it’s time to consider refinancing. Banks frequently offer “inside access” to unadvertised rates to attract high-quality borrowers. Refinancing isn’t just about a lower number; it is an opportunity to restructure your debt, consolidate other high-interest loans, or unlock equity for business growth. At Broker.com.au, we handle the heavy lifting, ensuring the transition is stress-free and aligned with your long-term wealth strategy.

From Calculation to Keys: How Broker.com.au Secures Your Dream

While a home loan mortgage calculator provides the essential numbers, it cannot account for the emotional weight of a property purchase or the intricate lending policies that change by the day. We believe that technology should empower our clients, not replace the need for expert human insight. Our award-winning approach combines AI-enhanced speed with the boutique personal attention you deserve. Whether you are in Perth, Sydney, or a regional centre, our national reach ensures you have inside access to the best rates and structures currently available in the Australian market. We take care of the heavy lifting, from initial financial modelling to final settlement, making the entire journey feel stress-free and streamlined.

The transition from a digital estimate to a signed contract requires a partner who understands the nuances of the 2026 lending environment. Our team acts as your expert guide, navigating the latest APRA debt-to-income limits and RBA shifts so you don’t have to. We don’t just find a loan; we engineer a solution that fits your specific life stages and business goals. This proactive attitude is why we are considered a high-level fixer for Australians who want more than just a generic bank experience. You can trust that your aspirations are being handled with professional precision and genuine care.

The Broker.com.au Difference

Our reputation as a “Best in class” finance partner is built on more than just securing a competitive rate. We focus on structuring your debt to align with your specific future, whether that involves growing a business or building a property portfolio. Our five-star testimonials reflect a commitment to going above and beyond for every client, especially those with complex needs that fall outside of the norm. Kylie and the crew are ready for a low-pressure, informative chat to help you interpret your home loan mortgage calculator results. You are in good hands with a team that prioritises your specific needs over a simple transaction.

Your Next Steps to Home Ownership

It is time to move from a state of uncertainty to one of streamlined confidence. You have done the research and crunched the numbers; now you need a seasoned partner to turn that data into a reality. Our “I’m interested” philosophy means there is no pressure to sign on the dotted line. We start with a low-pressure conversation to understand your goals and provide professional insight that no digital tool can replicate. Take the first step toward your next property today and experience the boutique attention that sets us apart.

I’m interested — let’s find your best rate

Take Control of Your Property Journey Today

Mastering your long-term budget involves more than just entering numbers into a home loan mortgage calculator; it requires a strategic vision for your wealth. You’ve seen how a 2 per cent buffer rate can stress-test your finances and how utilising offset accounts can dramatically shorten your loan term. For those with complex business structures, professional financial modelling is the only way to ensure your borrowing power is fully realised in this shifting market.

As award-winning brokers, we combine AI-proprietary technology for faster approvals with the personal touch of a boutique firm. You don’t have to navigate the 2026 lending landscape alone. Whether you need a high-level fixer for a trust structure or a simple health check on your current rate, you have direct access to Matt, Kylie, and Flavio for expert guidance. We are here to ensure your transition from calculation to keys is seamless and successful. Your dream property is within reach when you have the right team behind you.

I’m interested — let’s find your best rate

Frequently Asked Questions

How accurate is a home loan mortgage calculator?

A home loan mortgage calculator provides a highly accurate mathematical baseline for your monthly commitments. It uses standard compounding interest formulas to show how your loan amount and interest rate interact over time. However, it cannot account for specific lender credit policies or your individual financial health. Use it as a reliable starting point for your budget before moving to a tailored professional review.

Can I use a mortgage calculator if I am self-employed or a business owner?

Business owners can certainly use these tools, but the input requires a more nuanced approach. Instead of using your net profit, you should input your income including “add-backs” such as depreciation or one-off expenses. Standard web tools often underestimate what a specialist lender will allow. Speaking with an expert guide can help you identify your true borrowing capacity beyond what a simple digital portal shows.

What is the difference between a repayment calculator and a borrowing power calculator?

A repayment calculator determines the ongoing cost of a specific loan amount, whereas a borrowing power calculator estimates the total amount a bank might lend you. One helps you manage your weekly or monthly cash flow. The other establishes your maximum purchase price based on your income, expenses, and the current 2026 lending regulations. Both are essential for a complete property hunting strategy.

Does using a mortgage calculator affect my credit score?

No, using an online home loan mortgage calculator does not impact your credit score in any way. These tools are designed for anonymous educational engagement and don’t involve a “hard pull” on your credit file. You can test as many different scenarios, interest rates, and loan terms as you like without leaving any footprint on your financial record. It’s a completely stress-free way to explore your options.

Should I calculate my repayments based on a 25 or 30-year term?

We recommend testing both scenarios to see the long-term impact on your wealth. A 30-year term is the Australian standard because it keeps your initial repayments lower and more manageable. However, a 25-year term significantly reduces the total interest paid over the life of the loan. Seeing the difference in total cost often gives our clients the confidence to choose a shorter path to ownership.

How do I account for stamp duty in my mortgage calculations?

Stamp duty is an upfront government cost and should be factored into your total purchase budget rather than your loan repayments. Most buyers subtract stamp duty and legal fees from their total savings before entering their remaining cash as a deposit in the calculator. Because these costs vary by state, ensure you use local insights for your specific region to maintain an accurate budget.

What interest rate should I put into the calculator for 2026?

With the RBA cash rate at 4.35 per cent as of June 2026, you should use current variable rates starting around 6.09 per cent for your baseline. We also strongly advise adding a 2 per cent buffer to this figure. This stress-tests your budget against potential future rate hikes, ensuring you stay in good hands even if the economic environment shifts during your loan term.

Can a calculator show me how much I save with an offset account?

Yes, many advanced tools allow you to model the interest-saving power of an offset account. By entering your expected average balance, you can see how every dollar kept in the account reduces the interest-bearing balance of your mortgage. This visual representation often highlights why an offset account is a superior strategy for many Australians compared to a basic redraw facility, especially for future tax flexibility.