The traditional bank application you’ve been dreading might actually be the slowest way to grow your business in 2026. If you’re self-employed, you likely know the anxiety of being treated like a high-risk outsider just because your latest tax returns aren’t finalised or don’t reflect your true performance. It’s exhausting to watch a prime opportunity slip away while you’re stuck navigating endless red tape. However, modern low doc business loans have evolved into a strategic tool for agile Australian SMEs, allowing you to bypass the standard banking delays by using alternative documentation that actually reflects your current cash flow.

We’ll show you how to secure fast capital without the paperwork burden, ensuring you feel in good hands with a loan structure that matches your BAS or bank statements. This guide provides inside access to the latest lending landscape where pre-approvals can happen in as little as two hours and settlement often occurs within 48 hours. You’ll discover how to navigate the shift toward alt-doc financing to find a tailored solution that respects your time and fuels your next move.

Key Takeaways

- Learn why modern alternative lenders are filling the gap left by traditional banks for time-poor Australian business owners.

- Master the “Alt-Doc” hierarchy to secure low doc business loans using BAS or bank statements instead of complex tax returns.

- Compare the strategic benefits of secured versus unsecured funding to balance competitive interest rates with your business’s asset profile.

- Identify the essential eligibility markers, including why a clean credit history and 24 months of ABN registration are your strongest leverage points.

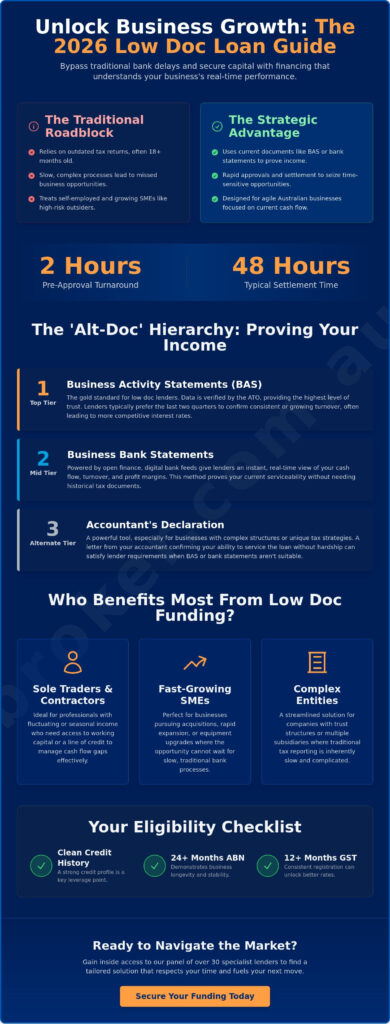

- Discover how inside access to a panel of over 30 specialist lenders can streamline your path to unconditional approval.

Table of Contents

- Understanding Low Doc Business Loans in the 2026 Australian Market

- Verification Methods: Proving Income Without Tax Returns

- Comparing Secured and Unsecured Low Doc Options

- Eligibility and Approval: Preparing for a Seamless Application

- Why Navigating the Market with Broker.com.au Makes Sense

Understanding Low Doc Business Loans in the 2026 Australian Market

For the modern Aussie entrepreneur, low doc business loans are no longer a fallback for those with “messy” books. Instead, they represent a high-level strategic choice. By understanding low-documentation loans in their current 2026 context, you can see how they bridge the gap between opportunity and capital. While traditional banks have historically relied on two years of certified tax returns, this data is often 18 months out of date by the time a loan is approved. In an economy that moves at the speed of digital commerce, waiting for your accountant to finalise last year’s figures can mean missing out on a vital acquisition or equipment upgrade.

The 2026 lending landscape has seen a distinct divergence. Major banks are tightening their criteria due to increased capital requirements, while boutique and fintech lenders are expanding their reach. These alternative providers focus on real-time viability rather than historical snapshots. With interest rates for these products starting from approximately 7.99% p.a. as of June 2026, the cost of capital is increasingly competitive. Choosing between fixed and variable terms now requires a look at the latest economic forecasts. Many savvy directors are opting for fixed terms to lock in certainty as the market adjusts to new regulatory environments, ensuring they remain in good hands throughout the loan term.

The Evolution of Alternative Income Verification

Tax returns are lagging indicators. They show where your business was, not where it’s going. Modern credit assessment now prioritises Business Activity Statements (BAS) and digital bank feeds. This shift is powered by open finance, which allows lenders to verify turnover and profit margins instantly. It’s an efficient, professional way to prove serviceability without the stress of a full forensic audit. This streamlined approach means that low doc business loans are now judged on current cash flow, reflecting the true health of your enterprise today.

Who Benefits Most from Low-Doc Funding?

This funding model is tailored for specific high-growth scenarios where speed and flexibility are paramount. You might find this structure particularly effective if you fall into one of these categories:

- Sole traders and contractors: Professionals with fluctuating seasonal income who need a Line of Credit or Working Capital Finance to bridge gaps.

- Fast-growing SMEs: Businesses pursuing Business Acquisition Funding or rapid fit-outs where the opportunity won’t wait for traditional bank red tape.

- Complex entities: Companies with trust structures or multiple subsidiaries where traditional tax reporting is naturally slow and complicated.

By moving away from the “sub-prime” stigma of the past, these loans have become a legitimate tool for proactive cash-flow management. They allow you to maintain momentum without being anchored by administrative burdens that don’t fit your business model.

Verification Methods: Proving Income Without Tax Returns

Proving your income shouldn’t feel like a cross-examination. In the current lending environment, the “Alt-Doc” hierarchy determines how lenders view your risk profile. While traditional institutions remain rigid, alternative lenders have established a clear ladder of trust. At the top of this hierarchy sit Business Activity Statements (BAS) and business bank statements, followed by accountant declarations. These documents provide a transparent view of your current trading performance, allowing you to access low doc business loans without waiting for your annual compliance to catch up.

When Comparing Secured and Unsecured Low Doc Options, the level of documentation you provide often dictates your interest rate. Lenders generally offer more competitive pricing to businesses that can show at least 12 months of consistent GST registration. This longevity, paired with verified turnover, signals stability. If your documentation is slightly thinner, you might find that boutique lenders are more receptive to an accountant’s letter, provided it confirms your ability to service the debt without hardship.

BAS vs. Accountant Declarations

Choosing between a BAS and an accountant declaration often comes down to your specific tax strategy. BAS-based lending is frequently the path to lower rates because the data is verified by the Australian Taxation Office. Most lenders prefer to see the last two quarters of BAS to confirm that your turnover is trending upwards. Conversely, an accountant declaration is a powerful tool for businesses with complex structures or those who have recently pivoted. It serves as a professional endorsement of your financial health, often acting as the “gold standard” for specialist lenders who look beyond the numbers.

Bank Statement Analysis and AI

The speed of modern approval is driven by sophisticated AI technology. Most alternative lenders now require 6 to 12 months of bank statements, which are analysed via secure digital feeds. This process identifies real-time serviceability by looking at your daily credits and debits. AI lenders define net cash flow as the total business revenue minus all recurring operating expenses and existing debt repayments over a rolling six-month period. To ensure a seamless experience, it’s vital to maintain a “clean” account. Lenders look for red flags such as excessive dishonours, round-sum transfers that look like undisclosed loans, or significant gambling spend. If you’re unsure how your statements might be viewed, you can start a conversation with our team to review your options before you apply.

Comparing Secured and Unsecured Low Doc Options

Choosing between a secured or unsecured structure is often the most significant financial decision you will make when seeking capital. It is a fundamental trade-off between the interest rate you pay and the level of asset security you are willing to provide. In the 2026 Australian market, low doc business loans have become highly specialised, offering tailored paths depending on whether you want to protect your assets or minimise your monthly repayments. While an unsecured loan offers rapid access to funds, a secured loan often unlocks the door to more substantial, long-term growth by leveraging the equity you have already built.

A hybrid approach is also gaining traction among savvy directors. By using specific equipment or vehicles as collateral via Asset Finance or Equipment Finance, you can find a middle ground. This allows for lower rates than a purely unsecured product without necessarily encumbering your primary commercial or residential property. It is a strategic way to keep your business moving while maintaining a manageable risk profile.

Secured Low-Doc Loans: Leveraging Equity

Utilising residential or commercial property to back your finance is the most efficient way to drive down the cost of capital. Lenders typically look for a Loan-to-Value Ratio (LVR) of 70% to 80% in a low-doc context. By providing this security, you can often access 30-year terms and significantly higher borrowing amounts, which are essential for Business Acquisition Funding or large-scale Commercial Property Loans. This structure provides the stability needed for major transitions, ensuring you are in good hands with a repayment plan that respects your long-term cash flow.

Unsecured Low-Doc Loans: Speed and Flexibility

When speed is your primary objective, unsecured low doc business loans are the ideal tool for seizing immediate opportunities. These products are perfect for short-term Working Capital Finance or establishing a Line of Credit to manage seasonal fluctuations. Because there is no property valuation required, settlement can often occur within 24 to 48 hours. However, the risk-based pricing means the cost of capital is typically higher than secured options. The primary advantage here is the avoidance of cross-collateralisation risks; your personal assets remain separate from your business debt, providing a layer of protection and streamlined confidence for the self-employed entrepreneur.

Eligibility and Approval: Preparing for a Seamless Application

Securing low doc business loans in 2026 requires more than just a healthy turnover; it demands a clean digital narrative. While the documentation burden is lower, the scrutiny on your personal credit history remains high. Lenders view your personal credit score as a primary indicator of character and reliability. A “clean credit” file, free from recent defaults or excessive enquiries, is often the difference between a rapid approval and a frustrating rejection. Our role as expert guides is to help you polish this narrative before it reaches the lender’s desk, ensuring you feel in good hands from the very first step.

Experience shows that 24 months of active ABN registration is the sweet spot for most competitive lenders. This timeframe proves your business has moved past the volatile startup phase and has established a sustainable rhythm. Additionally, being GST registered for at least 12 months is a vital threshold. It provides the third-party verification lenders need to trust your reported turnover without demanding full tax returns. Organising your digital footprint, from your bank statements to your ATO portal, is the best way to move from uncertainty toward a streamlined approval.

The Pre-Application Checklist

Success in the low-doc market is built on proactive preparation. Before starting your application, ensure you have ticked these essential boxes:

- Step 1: Confirm your ABN and GST status are active and reflect your current business structure.

- Step 2: Check your ATO Integrated Client Account for any outstanding debt. If a payment plan is in place, ensure it has been followed meticulously for at least six months.

- Step 3: Gather 6 to 12 months of business bank statements. Ensure these are “clean,” meaning they show consistent trading and no significant overdraws.

Common Pitfalls and How to Avoid Rejection

One of the most damaging mistakes a business owner can make is “enquiry shopping.” Applying at multiple lenders simultaneously creates several hits on your credit file, which modern AI algorithms interpret as a sign of financial distress. It’s also vital to distinguish between a “No-Doc” loan and low doc business loans. In a regulated market, true no-doc loans are virtually non-existent; you must provide some form of alternative verification to satisfy responsible lending requirements. To avoid these traps, we can “pre-flight” your application. This process identifies the right lender for your specific industry and credit profile before a formal enquiry is recorded. If you want to protect your credit score while exploring your options, I’m interested in a professional pre-flight assessment.

Why Navigating the Market with Broker.com.au Makes Sense

Finding the right capital shouldn’t be a gamble. Our proprietary AI technology gives you an immediate advantage by identifying the “inside track” for your specific industry. While a single bank only sees a set of numbers, our system scans a diverse panel of over 30 lenders to find the most efficient path. This includes everything from the major banks to boutique specialists who understand the nuances of low doc business loans. We don’t just find a product; we provide a tailored solution that looks beyond the surface to your business’s true potential. Our goal is to move you from a state of complexity toward a feeling of streamlined confidence.

Beyond Traditional Brokerage

We operate as a corporate advisory partner rather than a simple digital portal. This means we specialise in “outside the norm” situations, such as debt restructuring, M&A, or complex Asset Finance. If a traditional bank has already said no, we take the role of the “High-Level Fixer.” You’ll work with real people like Matt and Kylie who lead the process from start to finish. They understand that your dream doesn’t always fit into a standard box. Our team brings local insights and technical expertise in areas like SMSF loans and fit-out finance to every consultation. By providing inside access to the best rates and structures, we ensure your application for low doc business loans is positioned for relief and results. This elite level of personal attention ensures you’re always in good hands, regardless of how complex your tax structure might be.

Starting the Conversation

We believe in low-pressure conversations that lead to high-impact results. Our “I’m interested” approach is designed to reduce the anxiety of high-stakes financial decisions. When you reach out, you can expect a concise, 15-minute strategy call. We’ll discuss your goals, review your current BAS or bank statement position, and outline a clear path to resolution. It’s about moving you from uncertainty toward streamlined confidence. We handle the administrative red tape so you can focus on running your business. Ready to scale? I’m interested in exploring low doc options to see how we can help your business thrive.

Secure Your Business Future with Confidence

The Australian lending landscape has shifted toward flexibility. You don’t need to be restricted by outdated tax returns or the slow pace of traditional banks. By using modern verification methods like BAS and bank statements, you can access the capital required to scale your operations. Whether you’re pursuing a secured long-term facility or a rapid unsecured line of credit, the right low doc business loans serve as a strategic bridge to your next milestone. Success in 2026 is defined by agility and the ability to act when an opportunity arises.

At Broker.com.au, we pride ourselves on being the expert guide you need to bypass the red tape. As award-winning finance specialists, we provide inside access to a panel of over 30 leading Australian lenders. Our proprietary AI technology ensures faster approvals by matching your specific profile with the most receptive credit teams in the country. You’re in good hands with a team that prioritises your business potential over simple paperwork. We’re ready to help you move from uncertainty toward a state of streamlined growth.

I’m interested in a low doc loan

Your business deserves a partner who goes above and beyond to make your dreams a reality. Let’s start the conversation today.

Frequently Asked Questions

What is the maximum I can borrow with a low doc business loan?

You can typically borrow between $5,000 and $250,000 for unsecured options, though secured loans can access significantly higher amounts depending on the equity in your assets. The final limit is determined by your business turnover and the strength of the alternative documentation you provide. We work with a diverse panel of lenders to ensure you get the maximum capacity required for your specific growth or acquisition needs.

Do low doc business loans have higher interest rates than full doc loans?

Yes, interest rates for low doc business loans are generally higher than full-documentation loans because the lender accepts a higher level of perceived risk. As of June 2026, rates for these products start from approximately 7.99% p.a. Many business owners find this a professional trade-off, as the slightly higher cost is balanced by the ability to bypass months of bank red tape and seize immediate market opportunities.

Can I get a low doc loan if I have a new ABN?

Most competitive lenders require at least 24 months of active ABN registration to qualify for a low-doc structure. While some boutique specialists might consider businesses with 12 months of trading history, an ABN under six months is rarely eligible for alternative income verification. Having a consistent GST registration for at least 12 months will also significantly improve your chances of moving from uncertainty to an unconditional approval.

What documents do I actually need for a low doc application?

You typically only need to provide your ABN, identification, and 6 to 12 months of business bank statements or your most recent Business Activity Statements (BAS). Some lenders may also accept a signed accountant’s declaration as a professional endorsement of your serviceability. This streamlined approach avoids the need for two years of certified tax returns, ensuring the application remains efficient and fits the fast-paced nature of your business.

Is my family home at risk if I take out an unsecured low doc loan?

An unsecured loan does not use your family home as direct collateral, so the lender does not hold a mortgage over your property. However, you should be aware that most lenders require a personal guarantee from the directors. This means you remain personally liable for the debt if the business defaults, even though your residential property isn’t specifically listed as security on the loan contract itself.

How long does the approval process take with Broker.com.au?

Our proprietary technology allows us to provide a pre-approval in as little as 2 to 4 hours. Once your digital bank feeds or BAS documents are verified, unconditional approval and settlement often occur within 24 to 48 hours. This speed ensures you’re in good hands when timing is critical, allowing you to settle equipment purchases or business acquisitions without the stress of traditional banking delays.

Can I use a low doc loan for commercial property acquisition?

Yes, you can use secured low doc business loans for commercial property acquisition by leveraging the equity in the asset you’re purchasing. These loans often offer terms up to 30 years and typically require a Loan-to-Value Ratio (LVR) of between 70% and 80%. It’s an ideal solution for directors with complex trust structures who need a tailored approach that looks beyond standard tax return reporting.

What is the difference between a low doc and a no doc loan?

The difference lies in the verification required; low-doc loans use alternative evidence like BAS or bank statements, whereas “no doc” loans historically required no income proof at all. In the 2026 Australian market, true no-doc loans are virtually non-existent due to responsible lending regulations. Lenders must now conduct a credit assessment, making “low doc” or “alt doc” the legitimate strategic choice for self-employed professionals.