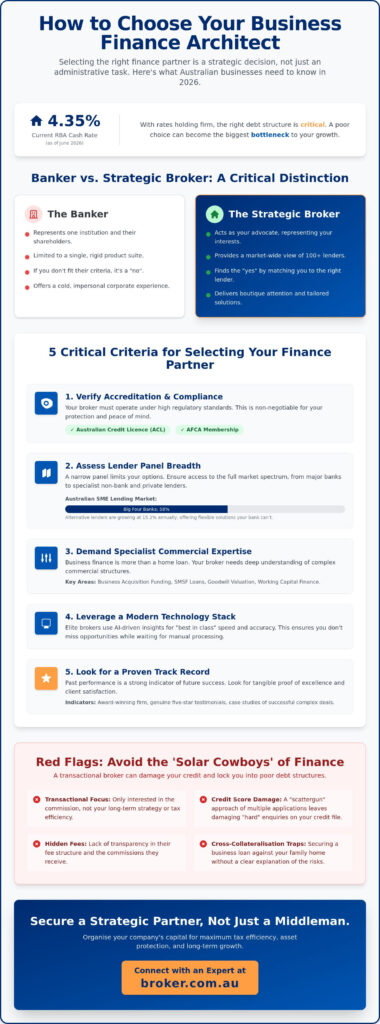

What if the person you hire to find your business capital is actually the biggest bottleneck to your growth? Many Australian business owners treat the search as a simple administrative task, but learning how to choose a business loan broker is actually about finding a strategic architect rather than just a middleman. It’s natural to feel a sense of dread over complex fee structures or the fear that a few misplaced credit enquiries could damage your score. With the RBA cash rate holding at 4.35% as of June 2026, the stakes for your bottom line have never been higher.

We understand that you want more than just a loan; you want a competitive edge. This guide will show you how to identify a high-level finance partner who provides inside access to the best market rates and organises your debt for maximum tax efficiency. We will walk you through the essential credentials and panel diversity required for a seamless, stress-free application process that protects your credit and fuels your long-term success.

Key Takeaways

- Distinguish between a residential mortgage broker and a dedicated commercial specialist to secure more sophisticated debt structures.

- Master how to choose a business loan broker by assessing the breadth of their lender panel across Tier 1, 2, and 3 institutions.

- Verify essential credentials like an Australian Credit Licence and AFCA membership to ensure your finance partner meets high-level regulatory standards.

- Leverage 2026 AI-driven insights to achieve a “best in class” application speed that remains tailored to your specific business goals.

- Identify the red flags of transactional brokers to avoid hidden fees and ensure your debt is organised for maximum tax efficiency.

Table of Contents

- What is a Business Loan Broker and Why Does Your Choice Matter?

- 5 Critical Criteria for Selecting Your Finance Partner

- The Speed of Certainty: AI and Technology in 2026 Brokerage

- Red Flags and Transparency: Avoiding the “Solar Cowboy” Equivalent

- Why Broker.com.au is the Logical Choice for Australian Businesses

What is a Business Loan Broker and Why Does Your Choice Matter?

To understand What is a Business Loan Broker, you must look beyond the simple act of filling out forms. A commercial finance broker is a specialist intermediary who designs tailored debt solutions to match your specific commercial goals. While many people are familiar with residential mortgage brokers who help families secure a home, a business finance specialist operates in a much more complex arena. They focus on balance sheets, EBITDA, and serviceability rather than just personal income. They are the architects of your company’s capital structure.

In the 2026 Australian economic climate, a broker acts as a strategic architect who ensures your capital structure remains resilient against market volatility and shifting RBA cash rates. They serve as an Expert Guide, navigating a panel of over 100 Australian lenders to find the perfect fit for your needs. This is crucial when you consider that the “Big Four” banks still hold 58% of the SME lending market share, yet alternative lenders are growing at 15.2% annually. Knowing how to choose a business loan broker means finding someone who understands this shifting landscape and can unlock doors that remain closed to the general public.

The Difference Between a Banker and a Broker

A bank manager is an employee of one institution. Their loyalty lies with their employer, and they can only offer the specific product suite that the bank provides. If your situation falls even slightly outside their rigid criteria, the answer is usually a “no.” A broker provides a market-wide view. They offer inside access to non-bank lenders and private credit funds that banks simply cannot reach. Instead of a cold, impersonal corporate experience, you receive boutique attention from a partner who is incentivised to find you the best possible outcome across the entire market.

Why One-Size-Fits-All Lending is a Risk for SMEs

Generic lending products often lead to dangerous debt structures. One common mistake is cross-collateralisation, where a lender secures a business loan against your family home without you fully realising the risk. A high-level fixer prevents these traps by ensuring your debt is structured for tax efficiency and asset protection. They also protect your credit score. Every time you apply directly to a bank, it leaves a “hard” enquiry on your file. A broker performs a single assessment and only submits your application when they are confident of a “yes.” This strategic approach is a key reason why understanding how to choose a business loan broker is vital for your long-term financial health.

5 Critical Criteria for Selecting Your Finance Partner

Selecting a partner to manage your company’s debt is a high-stakes decision. If you are wondering how to choose a business loan broker, you must look for specific markers of quality that separate elite advisors from transactional middlemen. It isn’t just about who can get you a “yes”; it’s about who can secure the best rates while protecting your long-term interests.

- Verify Accreditation: Every legitimate Australian broker must hold an Australian Credit Licence (ACL) or be a credit representative of a licensee. They should also be members of the Australian Financial Complaints Authority (AFCA) for your peace of mind.

- Lender Panel Breadth: Ensure they have access to Tier 1, 2, and 3 lenders. A narrow panel limits your options and often leads to higher costs or restricted terms.

- Specialist Expertise: Assess their ability to handle complex scenarios like Business Acquisition Funding or SMSF loans. These products require more than a basic application; they require a deep understanding of commercial structures.

- Technology Stack: Elite brokers use proprietary AI to provide “Quick and Accurate” feedback. This ensures you don’t miss market opportunities while waiting for manual data entry.

- Proven Track Record: Look for an “Award-Winning” firm with genuine five-star testimonials. These should speak to their “Best in class” service and ability to deliver in tight timeframes.

Industry Specialisation and Acquisition Expertise

A significant gap in the market is the lack of brokers who truly understand business purchases. When you buy an existing company, you aren’t just buying equipment. You are buying “Goodwill” and future cash flow. This requires a deeper level of financial modelling to account for debt serviceability from future earnings rather than just historical data. A high-level fixer will help you structure Working Capital Finance into the deal to ensure your first 90 days are stable. If you’re looking for this level of detail, I’m interested in helping you explore your options.

Lender Panel Depth: Beyond the “Big Four”

While the Big Four banks hold about 58% of the SME lending market share, the real innovation is happening in the alternative lending space. This sector is projected to grow by 15.2% annually, reaching US$23.07 billion by the end of 2026. A deep lender panel gives you access to fintechs and private credit funds that offer “Best in class” flexibility. These boutique relationships are vital for ensuring Red Flags and Transparency are addressed in your loan terms. Many of these lenders look past traditional security requirements to focus on your actual business performance, providing tailored solutions that a standard bank simply cannot match.

The Speed of Certainty: AI and Technology in 2026 Brokerage

In the current financial climate, speed is no longer just a luxury; it’s a competitive necessity. Australian businesses often operate on tight windows of opportunity, whether it’s a snap acquisition or a sudden need for working capital. When evaluating how to choose a business loan broker, you must look closely at their digital infrastructure. The “old-school” method of manual data entry and week-long wait times won’t suffice in a market where alternative lending is growing by 15.2% annually. You need a partner who uses proprietary AI to provide quick and accurate feedback, ensuring you don’t miss out on vital growth capital.

A tech-led brokerage delivers a seamless and stress-free experience by removing the friction points of traditional lending. Digital document collection allows you to upload sensitive financial data once, rather than repeating the process for every lender on the panel. This efficiency doesn’t just save time; it provides a best in class level of accuracy. By the time you reach the final application stage, the broker has already used technology to filter out unsuitable options, leaving only the most competitive rates and structures. This level of professional precision is why many brokers are accredited by the Finance Brokers Association of Australia (FBAA), ensuring they maintain high standards while using these advanced tools.

AI vs. Manual Processing: What it Means for Your ROI

Proprietary AI identifies the best fit lender in minutes, not days. It scans thousands of data points across Tier 1, 2, and 3 lenders to match your specific risk profile with the right appetite. This reduces human error in complex financial modelling and serviceability checks. For you, this means a higher return on investment because you aren’t wasting weeks on applications that were never going to be approved. Instead, you gain inside access to current market rates and debt structures tailored to your long-term success.

Security and Privacy in the Digital Age

As technology advances, so do the risks. ASIC has identified technology-driven consumer harm, including risks from automated decisions, as a key systemic risk for 2026. A high-level fixer prioritises data integrity as much as loan approval. Top-tier brokers protect your information through secure, encrypted portals that offer seamless integration with accounting software like Xero or MYOB. This ensures that your sensitive business data is handled with the boutique attention it deserves, keeping you in good hands throughout the entire application process. When you understand how to choose a business loan broker, you’ll realise that their commitment to your privacy is just as important as the rate they secure.

Red Flags and Transparency: Avoiding the “Solar Cowboy” Equivalent

The “solar cowboy” phenomenon isn’t limited to renewable energy; it exists in the finance world too. These are brokers who focus on volume rather than value, often leaving business owners with poorly structured debt and higher-than-necessary interest rates. Learning how to choose a business loan broker requires you to distinguish between a “Transactional” middleman and a “Strategic” advisor. A transactional broker often rushes the process, pushing you toward a single lender because it’s the path of least resistance for them. If a broker fails to present a range of options from a diverse panel of Tier 1, 2, and 3 lenders, it’s a major red flag.

In Australia, transparency is a regulatory necessity. A professional broker must provide a Credit Proposal Document (CPD) that clearly explains all fees and charges before you commit. They are also required to disclose the commissions they receive from lenders. This disclosure ensures you understand exactly how your partner is being compensated, removing any suspicion of bias. Transparent commission disclosure is a fundamental part of the Best Interests Duty that protects Australian SMEs from predatory practices.

The Danger of “Hard” Credit Enquiries

One of the most damaging mistakes a business owner can make is applying to multiple lenders simultaneously. Each “hard” enquiry is recorded on your credit file. If you rack up too many in a short window, your credit score drops, and lenders may view your business as being in financial distress. A seasoned partner protects your borrowing power by conducting a “soft” pre-assessment first. They use their expertise to determine which lender is most likely to approve the loan before a single formal enquiry is made. This Expert Guide approach ensures your credit file remains clean and your reputation with lenders stays intact.

Understanding Fee Structures: No More Hidden Costs

An elite broker is never shy about their fees. They will break down the difference between their brokerage fee, the lender’s application fee, and any ongoing commissions. This level of honesty is what provides a stress-free experience. You shouldn’t be surprised by a bill at the end of the process. Award-winning firms are comfortable being upfront because their ability to secure better rates and more efficient debt structures provides a clear, measurable return on investment. If you want a partner who values transparency as much as you do, I’m interested in helping you secure your next round of funding.

Why Broker.com.au is the Logical Choice for Australian Businesses

Deciding how to choose a business loan broker is a decision that defines your company’s financial trajectory. Broker.com.au stands as your Expert Guide, combining national reach with deep local insights across the Australian market. Our award-winning status isn’t just a trophy; it’s a reflection of our commitment to best in class technology and a can-do attitude that ensures you’re in good hands. We don’t just find loans. We design capital structures that alleviate financial anxiety and pave the way for your long-term success.

While many competitors focus on simple transactions, we pride ourselves on being a high-level fixer for complex scenarios. Whether you’re navigating an intricate M&A deal or seeking SMSF loans for commercial property, our team has the technical expertise to handle situations that fall outside of the norm. We use our proprietary AI to ensure the process remains seamless, providing you with inside access to the best rates without the typical stress of a large-scale bank application. You’ll feel the difference that boutique attention makes from the very first interaction.

Tailored Solutions for Every Stage of Growth

Your business needs change as you scale. We provide tailored solutions that grow with you, from Unsecured Business Loans for immediate working capital to large-scale Development Finance for major projects. We also understand that your personal and professional lives are often linked. That’s why we support business owners with Home Loans and asset finance for vehicles or equipment. By having a single partner who understands your entire financial modelling, you ensure that every piece of debt is organised for maximum efficiency and tax benefit. We stay proactive so you can focus on running your business.

Get Started with a Low-Pressure Conversation

We believe the best partnerships start with a dialogue, not a sales pitch. Our “I’m interested” philosophy is designed to reduce the pressure often felt when seeking commercial finance. When you reach out, you aren’t just a number in a digital portal. You’ll connect with experienced human advisors like Matt, Kylie, or Flavio, who take the time to understand your specific dreams and needs. We are here to simplify the complexity of the 2026 lending landscape and get you moving toward your goals with confidence. It’s time to experience a finance process that actually works for you.

I’m interested — Let’s discuss your business goals

Secure Your Commercial Future with Confidence

You now have the strategic framework to distinguish a high-level advisor from a transactional middleman. Remember that your choice impacts everything from your daily cash flow to your long-term tax efficiency. Mastering how to choose a business loan broker is about finding a partner who balances national expertise with a boutique feel. It’s about ensuring your debt is organised for growth and resilience in an evolving economic landscape.

At Broker.com.au, we combine award-winning finance solutions with proprietary AI for 2026 speed. This ensures your application is both quick and accurate while protecting your credit score from unnecessary enquiries. We aim to take the anxiety out of high-stakes financial decisions, placing you in the hands of seasoned specialists who prioritise your specific business needs. If you’re ready to secure the best rates and move forward with streamlined confidence, let’s start a conversation. I’m interested in a tailored finance solution and look forward to helping you achieve your next milestone.

Frequently Asked Questions

Is it better to go to a bank or a business loan broker?

A broker is generally the superior choice because they offer a market-wide view across over 100 lenders. While a bank manager can only sell you their own institution’s products, a broker acts as an Expert Guide to find the best fit for your specific needs. This level of choice is essential when learning how to choose a business loan broker who can secure competitive rates and flexible terms.

How do business loan brokers get paid in Australia?

Brokers are typically paid via a commission from the lender once your loan settles. In some cases, they may also charge an upfront brokerage fee for complex advisory work or financial modelling. All compensation must be transparently disclosed in your Credit Proposal Document to ensure you understand exactly what you’re paying for before the process begins.

Can a broker help if I have a complex business structure or SMSF?

Yes, specialist brokers are equipped to handle complex entities including trusts, multi-company groups, and SMSF lending. They act as high-level fixers who understand the legal and tax implications of these structures. This expertise ensures your debt is organised correctly for long-term compliance and maximum tax efficiency.

What documents do I need to provide to a business loan broker?

You’ll usually need to provide your most recent financial statements, including a Profit and Loss and a Balance Sheet. Lenders also require tax returns for the business and directors, along with several months of bank statements to verify cash flow. Having these documents organised early makes for a seamless and stress-free application process.

Will using a broker affect my business credit score?

A professional broker actually protects your credit score by performing a “soft” assessment before any formal submission. This prevents the “poisoning” of your credit file that occurs when you make multiple direct applications to different banks. Understanding how to choose a business loan broker involves finding a partner who prioritises your borrowing power and reputation with lenders.

How long does the business loan application process typically take?

The timeframe varies significantly based on the type of finance you require. Simple unsecured business loans can be approved and funded in as little as 24 to 48 hours through fintech lenders. Conversely, complex commercial property loans or development finance may take several weeks to reach settlement due to more intensive valuation and legal requirements.

What is the difference between a secured and unsecured business loan?

A secured loan requires an asset, such as commercial property or equipment, to be used as collateral. This usually results in lower interest rates because the lender has more security. An unsecured loan doesn’t require physical collateral but instead relies on the strength of your business’s revenue and consistent cash flow to prove serviceability.

How do I know if a business loan broker is reputable?

Reputable brokers must hold an Australian Credit Licence and maintain membership with the Australian Financial Complaints Authority (AFCA). You should also check for accreditation from professional bodies like the FBAA or MFAA. Genuine client testimonials and industry awards are excellent indicators that you are in good hands with a competent professional.