What if the long-term success of your new business had less to do with the logo on the door and more to do with the way you structured your entry debt? While joining a proven franchise system offers a sense of security, the financial reality in 2026 is increasingly complex. You’re likely feeling the weight of stricter lending criteria or the fear of hidden marketing levies and fit-out costs that can quickly drain your working capital. It’s a high-stakes environment where the difference between a thriving shopfront and a financial burden often comes down to your initial funding strategy.

We agree that the path to business ownership should feel like an exciting milestone, not a source of constant stress. Our goal is to help you master the financial complexities of the Aussie franchise sector and secure the best funding to kickstart your business journey. This guide provides a clear roadmap for your acquisition, offering inside access to competitive interest rates and a breakdown of the latest 2026 regulatory updates to ensure your business model is truly bankable.

Key Takeaways

- Understand the 2026 regulatory landscape and how the updated Franchising Code of Conduct protects your investment through mandatory disclosure.

- Learn to distinguish between the initial franchise fee and the total turnkey price to ensure you have sufficient capital for fit-out and legal costs.

- Discover how to present a bankable business case to lenders by reviewing the proven financial performance and goodwill of your chosen franchise brand.

- Compare the risk-adjusted success rates of established systems against independent startups to determine the most secure path for your entrepreneurial goals.

- Gain inside access to a network of over 30 specialized lenders and proprietary technology designed to streamline the funding process for a seamless acquisition.

Table of Contents

- What is a Franchise? Understanding the Australian Model in 2026

- The Real Cost of Entry: Structuring Your Franchise Capital

- Franchise vs. Independent Startup: A Risk-Adjusted Comparison

- The Road to Approval: Securing Your Franchise Loan

- How Broker.com.au Streamlines Your Franchise Journey

What is a Franchise? Understanding the Australian Model in 2026

The Australian franchise landscape is built on a foundation of shared risk and mutual reward. Unlike starting a business from scratch, this model allows you to step into a pre-existing operational framework. The Franchise Council of Australia (FCA) acts as the industry’s peak body, working alongside the ACCC to uphold the mandatory Code of Conduct. While the global definition of franchising focuses on the broad licensing of intellectual property, the Australian context is strictly regulated to ensure transparency. This regulatory environment is designed to protect your investment, ensuring that every franchisor-franchisee relationship is grounded in transparency and good faith.

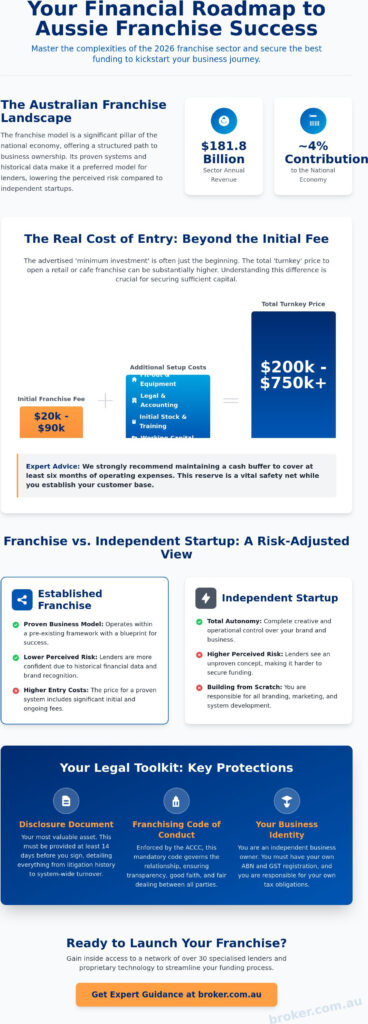

Lenders generally prefer the “proven system” model because it provides a historical blueprint for success. When you seek funding, a bank looks for predictability. An established franchise offers years of audited financial data, which significantly lowers the perceived risk compared to an unproven independent startup. This stability is a major reason why the sector’s annual revenue reached $181.8 billion in April 2026, contributing roughly 4% to the national economy. From high-turnover quick service restaurants to low-overhead home-based services, the diversity of the sector offers a path for almost any budget.

The Legal Framework: Rights and Responsibilities

Your most valuable asset isn’t the signage on the building; it’s the Disclosure Document. Under the current code, franchisors must provide this at least 14 days before you sign any agreement. It details everything from litigation history to system-wide turnover. You’ll also need to distinguish between the “Licence to Operate” and the physical assets you own. While you might own the equipment and fit-out, the brand remains the property of the franchisor. From a tax perspective, you’ll still need your own ABN and GST registration. You’re an independent business owner operating under a shared banner, which requires a clear understanding of your individual tax obligations.

Top Tier vs. Emerging Brands

Securing Business Acquisition Funding is often more straightforward with “Top Tier” brands. These household names have a bankable track record that simplifies the approval process. However, entry costs are often significantly higher, reflecting the lower risk profile. In contrast, “disruptor” franchises in the 2026 market, such as specialised mobile services or boutique fitness studios, offer lower overheads and faster paths to positive cash flow. While they may carry more risk in a lender’s eyes, their agility appeals to a new generation of entrepreneurs. Your choice between an established giant or an emerging brand will directly dictate your debt structure and the type of lenders willing to support your journey.

The Real Cost of Entry: Structuring Your Franchise Capital

Don’t let the ‘minimum investment’ figure on a brochure lead you into a capital trap. In the Australian franchise market, there’s a significant gap between the initial fee and the total turnkey price. While the upfront franchise fee typically ranges between $20,000 and $90,000, the cost to actually open the doors of a retail or cafe outlet often reaches between $200,000 and $750,000. This turnkey figure covers everything from the lease bond to the first day’s milk delivery, and failing to account for it is a common pitfall for new owners.

Beyond the obvious, you must account for ‘hidden’ costs that aren’t always front-of-mind. Professional legal fees are non-negotiable for a thorough review of your obligations under the Franchising Code of Conduct. You’ll also face costs for mandatory training, which might involve interstate travel and accommodation. We strongly advise maintaining a cash buffer to cover at least six months of operating expenses. This reserve acts as a vital safety net while you build your local customer base and fine-tune your staff roster.

Fit-out and Equipment Finance

Retail and hospitality ventures live or die by their physical presentation. Using Fit-out Finance allows you to preserve your cash for day-to-day operations rather than sinking it all into floorboards and counters. Structuring this debt is a precise exercise; your loan term should never exceed your initial lease period. This alignment prevents you from paying for a shopfront you no longer occupy. Additionally, Asset Finance for essential machinery or Equipment Finance for specialised tools often provides useful tax advantages, allowing you to manage depreciation more effectively while keeping your working capital liquid.

Working Capital and Marketing Levies

Ongoing costs are the second half of the capital puzzle. Ongoing royalties, typically between 4% and 9% of gross revenue, and marketing levies of 1% to 4% are non-negotiable costs that fund the brand’s national presence. These aren’t just ‘fees’; they’re investments in the system’s longevity. To manage the inevitable ebbs and flows of seasonal trade, a Line of Credit is an essential tool. It provides a safety net for those months when the marketing levy is due but foot traffic is lean. If you’re ready to see how these costs fit into your personal profile, you can explore your funding options to find a structure that supports long-term growth.

Franchise vs. Independent Startup: A Risk-Adjusted Comparison

Choosing between a blank slate and a proven system is the first major hurdle for any Australian entrepreneur. While an independent startup offers total creative freedom, it lacks the historical data that banks crave. When you buy into a franchise, you aren’t just purchasing a business; you’re acquiring a refined operational manual and a built-in customer base. This “Goodwill” factor is often the difference between a struggling first year and immediate cash flow. According to the Franchise Council of Australia, the sector’s contribution of $181.8 billion to the national economy is a testament to the resilience of this structured model.

The trade-off for this security is a loss of creative control. You won’t be able to change the logo, the menu, or the core service offering. For many, this is a small price to pay for a lower risk profile. Lenders agree. They view the predictability of a system as a safeguard against the high failure rates seen in the independent small business sector. This perceived stability allows you to move from a state of uncertainty toward a feeling of streamlined confidence.

Bank Appetite and Lending Ratios

Banks maintain an internal “Bank List” of accredited brands that have already passed their rigorous risk assessments. If your chosen brand is on this list, you’ll often find that lenders are more willing to offer higher Loan-to-Value Ratios (LVR). This means you might only need a 20% or 30% deposit, whereas an independent startup might require 50% or more. Having this inside access to the best rates can drastically change your initial capital requirements.

You’ll also need to decide between Secured Business Loans and Unsecured Business Loans. As of June 2026, secured rates are sitting between 6.5% and 14% p.a., providing a more cost-effective way to fund your dream if you have property to leverage. Unsecured options offer faster access to funds but come with higher interest rates, typically ranging from 8.5% to 24% p.a. for those without physical collateral.

Scalability and Exit Strategy

A significant advantage of the franchise model is the ease of resale. Selling a recognised brand is often much simpler than trying to find a buyer for a unique, independent shop. Buyers feel more confident stepping into a system where the training and supply chains are already established. This makes your exit strategy far more predictable from day one.

If your goal is to become a “Multi-Unit” owner, you must structure your initial Business Acquisition Funding with expansion in mind. We help you organise your debt so that your first location’s equity can eventually support the purchase of a second or third site. Just remember that your exit strategy is partially governed by the franchisor; they usually have the right to approve any incoming buyer to ensure the system’s standards remain high.

The Road to Approval: Securing Your Franchise Loan

Securing a loan for your new business requires a shift in perspective. You’re no longer just a borrower; you’re a partner in a proven system. Lenders don’t just look at your bank balance. They look at the brand’s track record. Banks maintain strict “accreditation lists” that dictate whether a franchise is bankable. If your chosen system isn’t on that list, your path to approval becomes significantly steeper. We help you move from a state of uncertainty toward a feeling of streamlined confidence by matching you with lenders who already know and trust your brand.

The approval process generally follows five critical steps:

- Step 1: Prepare a comprehensive personal financial statement and check your credit history for any red flags.

- Step 2: Audit the franchisor’s financial performance. A lender will want to see that the system itself is profitable and sustainable.

- Step 3: Develop a robust three-year cash flow forecast. This is where financial modelling proves your ability to service the debt.

- Step 4: Decide between a Secured Business Loan or using Asset Finance for specific equipment.

- Step 5: Choose your lender. Specialist lenders understand the sector’s nuances far better than generalist bank managers.

The Importance of Financial Modelling

Credit managers are trained to look for holes in your plan. “Best case” scenarios won’t win them over. Your forecast must be grounded in reality, factoring in current benchmarks like the Westpac small business loan rate of 7.91% effective June 1, 2026. Our proprietary AI technology now allows us to stress-test your business plan against thousands of historical data points to ensure your forecast holds up under pressure. This level of preparation signals to the bank that you’re a professional operator who understands the risks as well as the rewards.

Avoiding the Cross-Collateralisation Trap

One of the biggest risks for new owners is tying the family home to the business debt. While Secured Business Loans offer lower interest rates, they often require personal property as collateral. We often suggest strategies to secure funding using the business assets alone. By using Unsecured Business Loans or specific Equipment Finance, you can protect your personal wealth from business volatility. This corporate advisory approach ensures that your “dream” doesn’t become a nightmare for your family’s financial security. If you want to see which lenders are currently favouring your chosen brand, get started with a preliminary assessment today.

How Broker.com.au Streamlines Your Franchise Journey

Securing the right funding for a franchise acquisition shouldn’t feel like a second full-time job. Our role as your Expert Guide is to handle the heavy lifting with the banks while you focus on building your new team. With inside access to over 30 lenders tailored for SMEs, we ensure you aren’t limited by the narrow criteria of a single big-four bank. We specialise in Business Acquisition Funding and loan restructuring, ensuring your debt is organised for maximum tax efficiency and long-term scalability.

Speed is often the deciding factor in a competitive market. Our proprietary AI technology moves you from “I’m interested” to “Approved” faster by instantly matching your profile against thousands of lending policies. This efficiency eliminates the guesswork and provides a seamless, stress-free path to ownership. You’re in good hands with a team that treats your business dream as our own priority, moving you from uncertainty toward a state of streamlined confidence.

Tailored Finance for Aussie Entrepreneurs

Consider a local entrepreneur we recently assisted. They were looking to secure Fit-out Finance for a flagship retail site but were met with hesitation from traditional lenders due to the brand’s relatively new entry into the Australian market. By leveraging our award-winning brokerage network and local insights, we secured a tailored package that included Equipment Finance and a Line of Credit to protect their initial cash flow. This isn’t just about finding a loan; it’s about providing a professional solution that fits your specific needs.

Our “I’m interested” philosophy is the core of our service. We don’t believe in high-pressure sales tactics. Instead, we offer low-pressure, high-insight consultations that empower you with the facts. You’ll work with seasoned advisors like Matt or Kylie, who act as your personal advocates in every negotiation. This human-led approach ensures you get the best rates available in the 2026 market without the cold, impersonal feel of a traditional large-scale bank.

Ready to Start Your Franchise Journey?

There’s never been a better time to move from employee to employer. The 2026 economic landscape favours agile, system-backed businesses that can scale quickly. Having a “High-Level Fixer” in your corner during negotiations gives you a distinct advantage, especially when dealing with complex lease agreements or franchisor requirements. We’re here to ensure your entry into the franchise sector is professional, efficient, and ultimately successful. If you’re ready to explore your options, I’m interested in franchise funding and would like to start the conversation today.

Turning Your Franchise Ambitions into Reality

The path to business ownership is a significant milestone that requires both vision and a solid financial foundation. You’ve learned that success in the Aussie franchise sector depends on more than just brand recognition; it requires a deep understanding of turnkey costs and the strategic use of fit-out finance. By prioritising a bankable business model and protecting your personal assets from cross-collateralisation, you’re already ahead of the curve. This proactive approach ensures you’re moving from a state of uncertainty toward a feeling of streamlined confidence.

As an award-winning business loan broker, we specialise in business acquisition and debt structuring to ensure your journey is as seamless as possible. Our proprietary AI technology allows for quick and accurate applications, matching you with the right lenders from our extensive network. We’re here to act as your expert guide, providing the local insights needed to secure the best possible rates. If you’re ready to transition from employee to employer with confidence, I’m interested in franchise funding and would like to start the conversation. Your future as a business owner is within reach, and we’re here to help you secure it.

Frequently Asked Questions

Is it hard to get a business loan for a franchise in Australia?

Obtaining a loan for a franchise is often more straightforward than for an independent startup because lenders value the proven track record of the brand. If you choose a brand that is already accredited on a bank’s internal list, the approval process is significantly smoother. However, you’ll still need to demonstrate a solid personal credit history and provide a realistic three-year cash flow forecast to satisfy the bank’s risk assessment criteria.

How much deposit do I need to buy a franchise?

You generally need a deposit ranging from 30% to 50% of the total turnkey cost, though this varies based on the brand’s reputation and your choice of lender. For highly rated, top-tier brands, some banks may offer a higher Loan-to-Value Ratio (LVR), potentially allowing you to start with a 20% deposit. It’s vital to remember that this deposit must cover the total investment, including fit-out and initial stock, not just the upfront fee.

Can I use my superannuation (SMSF) to buy a franchise?

While you can use a Self-Managed Super Fund (SMSF) to purchase the commercial property where your business operates, you generally cannot use it to fund the daily operations of a business you run yourself. This is due to the “sole purpose test” regulated by the ATO, which ensures super funds are maintained only for retirement benefits. We can help you explore SMSF Loans if you’re looking to acquire the premises for your new venture as part of a long-term wealth strategy.

What happens if the franchisor goes bust?

If a franchisor enters insolvency, your rights are governed by the Franchising Code of Conduct and the specific terms of your agreement. The 2025 updates to the code have strengthened disclosure requirements, giving you more transparency regarding the franchisor’s financial health before you sign. In some cases, franchisees may be able to continue operating independently or as a collective, but you’ll likely lose access to the brand’s national marketing and supply chain benefits.

Do I need a secured or unsecured business loan for a franchise?

The choice between a secured or unsecured loan depends on your available collateral and your risk appetite. Secured Business Loans offer lower interest rates, often between 6.5% and 14% p.a. in June 2026, but require you to leverage an asset like your family home. Unsecured Business Loans provide faster access to capital without requiring physical collateral, though they carry higher interest rates to account for the increased risk to the lender.

How long does the franchise finance approval process take in 2026?

The timeline for finance approval in 2026 varies greatly between traditional banks and modern fintech lenders. Using our proprietary AI technology, we can often secure a preliminary “I’m interested” response or a formal approval in as little as 48 hours. Conversely, traditional big-four banks may still take four to six weeks to process a complex business acquisition application, as they require a more manual review of the franchisor’s audited accounts.

What is the difference between a franchise fee and a royalty fee?

The initial fee is a one-off payment, typically between $20,000 and $90,000, that grants you the right to join the system and use the brand’s intellectual property. Royalty fees are ongoing monthly payments, usually between 4% and 9% of your gross revenue, that cover the cost of continuous support and system updates. You must also factor in a marketing levy, which is a separate ongoing contribution used for national brand advertising and promotional campaigns.

Should I use a specialist franchise broker instead of my local bank?

Using a specialist broker gives you inside access to over 30 different lenders, whereas your local bank can only offer you their own specific products. A specialist understands which lenders currently have an appetite for particular franchise brands and can help you avoid the “cross-collateralisation trap” that often ties your home to your business debt. We act as your expert guide, handling the heavy lifting and negotiations to ensure you secure the most competitive rates and terms available.