What if the biggest obstacle to your company’s growth isn’t your competition, but the way you’re paying for your machinery? Many local business owners find themselves stuck between a rock and a hard place; they need the latest gear to stay competitive, yet traditional bank delays often mean missing out on vital contracts. That’s where a dedicated equipment finance broker sydney becomes your most valuable strategic partner. We understand that in a market where the RBA cash rate sits at 4.35%, every percentage point on your chattel mortgage matters to your bottom line.

It’s stressful to watch your working capital tied up in depreciated assets when it should be fueling your next big project. You likely feel that traditional lending is too rigid for the fast-paced Sydney market. This article shows you how to secure the best possible rates and preserve your cash reserves to scale your operations. You’ll discover how to get fast approvals through a wide panel of specialised lenders and learn to structure your debt to be as tax-effective as possible.

Key Takeaways

- Understand the critical differences between chattel mortgages and finance leases to select the most tax-effective structure for your business assets.

- Learn how an equipment finance broker sydney provides inside access to a wide panel of lenders, creating the competition needed to secure the best possible rates.

- Discover why moving away from heavy capital expenditure toward financed models helps preserve your working capital for essential daily operations.

- Identify the specific requirements for Low-Doc and Full-Doc application pathways to ensure a seamless and stress-free approval process.

- Explore how proprietary matching technology can instantly align your funding needs with the right lender to support your long-term scaling goals.

Table of Contents

- Navigating the Equipment Finance Landscape in 2026

- Choosing the Right Finance Structure: Chattel Mortgage vs Leasing

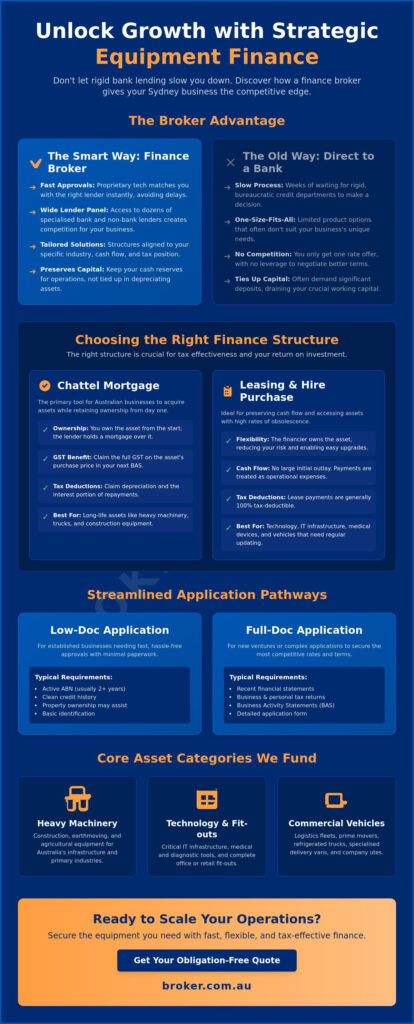

- The Broker Advantage: Why Sydney Businesses Avoid Direct Bank Applications

- Streamlining Your Approval: From Application to Settlement

- Scaling with Broker.com.au: Your Partner in National Asset Finance

Navigating the Equipment Finance Landscape in 2026

Equipment finance is a specialised credit facility designed to help your business acquire commercial assets without the immediate sting of a large cash outlay. In 2026, with the RBA cash rate sitting at 4.35 per cent, liquidity has become the number one priority for Sydney’s business owners. Rather than sinking hundreds of thousands of dollars into depreciating assets, smart operators are leveraging Asset-based lending to keep their cash reserves intact. This shift from capital expenditure (CapEx) to financed models allows you to pay for the equipment as it generates revenue, rather than paying for it all upfront.

Engaging an equipment finance broker sydney provides you with a strategic advantage that goes beyond just finding a low rate. It’s about securing a structure that aligns with your specific cash flow cycles. Whether you’re upgrading a transport fleet or installing high-end medical tech, the goal is to ensure your balance sheet remains healthy while your operational capacity grows. In a tight labour market where efficiency is everything, having the right tools can be the difference between winning a contract and being left behind.

Why Traditional Bank Lending is Falling Behind

Many Australian SMEs find that major banks have become increasingly rigid. Their one-size-fits-all credit policies often fail to account for industry-specific nuances or the rapid growth of modern businesses. This “bank-says-no” culture has led to a significant rise in non-bank lenders and private credit in the equipment space. These alternative providers are typically more agile, offering tailored terms that the big four banks often overlook. For a business needing to move quickly on a new contract, waiting weeks for a bank’s bureaucracy to grind through an application isn’t just an inconvenience. It’s a risk to your company’s growth.

Core Asset Categories for SME Scaling

Several key asset classes are currently driving growth across the Australian economy. Each category requires a different approach to risk and residual value, which is why localised insight is so critical. The most common assets include:

- Heavy Machinery: Construction and earthmoving “yellow goods” remain essential for the ongoing infrastructure boom.

- Technology & Fit-outs: Critical infrastructure for medical practices, data centres, and modern office environments.

- Commercial Vehicles: Logistics fleets, refrigerated trucks, and specialised delivery vans.

A professional equipment finance broker sydney understands these categories deeply. They know which lenders have an appetite for specific assets, ensuring you don’t waste time on applications that don’t fit a lender’s profile. By matching your business with the right specialised credit facility, you can secure the gear you need while maintaining the financial flexibility required to scale.

Choosing the Right Finance Structure: Chattel Mortgage vs Leasing

Finding a low interest rate is a great start, but the structure of your loan is what ultimately determines your return on investment. If you choose the wrong facility, you could miss out on significant tax offsets or find yourself stuck with outdated gear. An expert equipment finance broker sydney helps you weigh up these options based on your specific tax position and growth plans. The decision often comes down to a choice between immediate ownership and long-term flexibility. Securing the right structure through an equipment finance broker sydney ensures your debt works for you, not against you.

The Chattel Mortgage: Ownership and Tax Benefits

For most Australian ABN holders, the Chattel Mortgage is the primary tool for asset acquisition. Under this arrangement, you own the asset from the day of purchase, with the lender taking a “mortgage” over the “chattel” as security. The primary drawcard is the GST treatment. You can usually claim the full GST amount on the asset’s purchase price in your next Business Activity Statement (BAS), providing an immediate cash flow injection. Additionally, you can claim depreciation and the interest component of your repayments as tax deductions. This is particularly effective for assets under the $20,000 instant asset write-off threshold applicable for the 2025-2026 financial year. It’s the ideal choice for heavy assets like excavators or trucks that have a long operational life.

Leasing and Hire Purchase: Flexibility and Cash Flow

When you’re dealing with assets that have high obsolescence, such as servers or specialised medical tech, leasing is often the smarter move. You might consider Leasing or buying vehicles and equipment depending on whether you want the asset on your balance sheet. A Finance Lease gives you the benefits of use without the risks of ownership. In contrast, an Operating Lease is essentially a rental that allows you to upgrade at the end of the term, keeping your technology stack current. Hire Purchase sits in the middle, offering a path to ownership with fixed repayments where the lender owns the asset until the final payment is made.

To keep monthly repayments manageable, many businesses opt for a balloon payment. This is a lump sum paid at the end of the term. By deferring a portion of the principal, you free up monthly cash flow for day-to-day operations. If you’re unsure which path suits your current financial modelling, you can discover more about tailored asset finance that fits your specific industry needs. Using a balloon payment can be a high-level fixer for tight margins, provided you’ve planned for the final settlement.

The Broker Advantage: Why Sydney Businesses Avoid Direct Bank Applications

There is a persistent myth that going directly to your long-term bank is the fastest path to a better deal. In reality, loyalty often comes with a “lazy tax.” When you walk into a local branch, you’re limited to a single set of rigid credit policies and one suite of products. If your business doesn’t fit their specific “box,” you’re either rejected or slapped with a higher rate. An equipment finance broker sydney flips this dynamic by creating a competitive environment where multiple lenders vie for your business. This inside access ensures you aren’t just another number in a bank’s queue; you’re a valued client with options.

Beyond the rate, a broker acts as a high-level fixer for your credit profile. Every direct application you make at a bank leaves a “hard enquiry” on your credit file. If you’re shopping around yourself and hit three or four banks, your credit score can take a significant hit, making you appear high-risk to future lenders. We protect your standing by conducting a preliminary assessment and only submitting your application to the lender most likely to offer a seamless approval. You stay in good hands while we navigate the bureaucracy on your behalf, ensuring the process remains stress-free.

Access to Specialised and Tier-2 Lenders

Many of the most competitive finance products in 2026 aren’t available to the general public. They’re offered by Tier-2 and specialised lenders who operate without expensive retail branches, passing those savings on through wholesale rates. These lenders often have a deep appetite for specific industries, such as transport, medical fit-outs, or heavy construction. By partnering with an equipment finance broker sydney, you gain entry to these exclusive panels. These specialists understand the residual value of your specific machinery better than a generalist bank, often leading to more flexible terms and lower monthly repayments.

Structuring for Multi-Asset Growth

Big banks often try to “cross-collateralise” your loans, securing your new equipment against your commercial property or even your family home. This is a strategic trap that can stifle your future agility. If you want to sell a property or refinance your mortgage later, having your business gear tied to those titles creates a massive administrative headache. We prioritise keeping your equipment finance standalone. A dedicated broker organises your debt across a diverse panel of lenders to ensure your total borrowing power is maximised for future expansion.

Streamlining Your Approval: From Application to Settlement

The gap between identifying the right asset and actually putting it to work is the approval process. For many business owners, this is where the momentum stalls due to endless requests for more information. The most successful Sydney businesses treat their finance application like a strategic tender. By having your documentation ready, you allow an equipment finance broker sydney to present your business in the best possible light to the right lenders. This proactive approach is what turns a “maybe” into a “yes” while securing rates in the prime 5.79 per cent to 7.99 per cent range for established operators.

Lenders generally offer two pathways: Low-Doc and Full-Doc. Low-Doc applications are a “high-level fixer” for time-poor SMEs, often requiring only a clean credit history and a valid ABN without the need for full tax returns. However, if you’re looking for larger credit limits or have complex company structures, a Full-Doc application involving detailed financial modelling may be required. Regardless of the path, having your GST registration active for at least two years remains a key benchmark for accessing Tier 1 pricing in the 2026 market.

Preparation: What Your Broker Needs

To ensure your application is “best in class” before it hits a credit officer’s desk, you’ll need to gather a few essential items. Being prepared makes the entire journey stress-free and significantly faster. Your broker will typically require:

- Identification: Current Director’s ID and ABN details.

- Asset Details: A formal quote or pro-forma invoice from the supplier.

- Trading History: Proof of at least 2 years of active trading for Tier 1 rates, though specialist lenders can often assist newer startups.

- Credit Standing: A clear credit file is essential, as lenders in 2026 are placing heavy emphasis on repayment history.

The 5-Step Approval Process

We’ve refined the journey from initial enquiry to asset delivery into a seamless, five-step programme. This structure ensures you’re always in good hands and fully informed of your progress.

- Initial Consultation: We assess your asset needs and cash flow requirements.

- Lender Matching: We use proprietary insights to match you with a lender from our panel whose credit appetite fits your industry.

- Submission: Your application is lodged, often utilising AI-driven tools to bypass manual bank queues.

- Formal Approval: You receive a formal offer and sign the digital loan documents.

- Settlement: We coordinate with the supplier to pay them directly, allowing you to take delivery of your equipment immediately.

If you’re ready to upgrade your machinery without the usual bank headaches, you can get started with an expert assessment today. Our team ensures that your application is handled with the professional authority required to get the deal settled fast.

Scaling with Broker.com.au: Your Partner in National Asset Finance

Scaling a business in the current Australian market requires more than just a lender; it requires a strategic partner with national reach and local insights. As an award-winning leader in the finance sector, Broker.com.au provides the sophisticated financial modelling and inside access needed to fund complex, outside-the-box scenarios. Whether you are looking for a dedicated equipment finance broker sydney to fund a single vehicle or you need to coordinate a multi-state machinery rollout, our team is equipped to handle the heavy lifting. We act as your high-level fixer, ensuring that your capital remains fluid while your operational capacity expands across the country.

We understand that the anxiety of high-stakes financial decisions often stems from the unknown. That is why we’ve positioned ourselves as an expert guide, moving you from a state of uncertainty toward streamlined confidence. By choosing an equipment finance broker sydney with a national footprint, you benefit from a “can-do” attitude that traditional banks often lack. We pride ourselves on being proactive partners who prioritise your specific business dreams over impersonal credit algorithms.

AI-Enhanced Accuracy and Speed

Elite technology meets boutique service in our approval process. We utilise best in class proprietary AI to match your application with the right lenders instantly, significantly reducing the human error that often leads to bank delays or rejections. This technology allows us to provide faster turnaround times without sacrificing the tailored feel of our advice. Our “I’m interested” approach ensures that every interaction feels like the start of a low-pressure conversation rather than a rigid sales pitch. It is about giving you the information you need to make an informed choice at your own pace.

A Personalised Advisory Approach

While our technology is cutting-edge, our heart is human-led. Having a dedicated expert like Matt, Kylie, or Flavio on your side means you have a partner who truly understands the nuances of the Sydney business landscape. We provide corporate advisory services that extend far beyond a simple equipment loan, assisting with broader refinancing needs and strategic asset management. You stay in good hands with a team that goes above and beyond to ensure your finance structure remains as efficient as possible as you grow.

Ready to take the next step in your business journey? You can enquire about your equipment finance options with Broker.com.au today and experience a more seamless way to fund your future.

Secure Your Business Growth with Strategic Funding

Your company’s expansion shouldn’t be limited by rigid bank policies or outdated funding models. It is clear that the right structure, whether a chattel mortgage for long-term ownership or a flexible lease for rapid tech upgrades, is essential for preserving your vital working capital. Partnering with an expert equipment finance broker sydney allows you to bypass the “lazy tax” of traditional lenders while ensuring your credit score remains protected throughout the process.

As an award-winning brokerage with national reach, Broker.com.au combines the speed of proprietary AI with the nuanced insight of seasoned advisors. We specialise in those “outside the box” financial scenarios that the big banks often overlook, providing a seamless path from application to settlement. You’ve done the hard work of building your business; let us handle the complexities of the lending landscape on your behalf.

I’m interested in equipment finance solutions

We are ready to help you turn your next operational goal into a reality. You can move forward with confidence knowing your business is in good hands.

Frequently Asked Questions

What is the difference between an equipment finance broker and a bank?

A bank offers only its own limited suite of products, whereas an equipment finance broker sydney provides inside access to a wide panel of lenders. This creates a competitive environment where lenders vie for your business, ensuring you aren’t stuck with a rigid “one-size-fits-all” policy. While a bank representative is limited by their employer’s specific risk appetite, a broker acts as an expert guide to find the most tailored fit for your needs.

How much can I borrow for business equipment in Australia?

You can generally borrow up to 100 per cent of the asset’s purchase price, including GST and delivery costs. The total borrowing capacity depends on your business’s trading history, credit score, and the specific type of asset being financed. For established businesses with strong financials, lenders often provide limits that allow for multiple asset acquisitions over a financial year without requiring a new application for every item.

What are the tax benefits of a Chattel Mortgage for my SME?

A Chattel Mortgage allows you to claim the full GST amount on your next Business Activity Statement because you own the asset from the day of purchase. You can also claim tax deductions for the asset’s depreciation and the interest component of your loan repayments. Under the current 2025-2026 rules, small businesses can often utilise the $20,000 instant asset write-off for eligible equipment, providing a significant boost to cash flow.

Can I get equipment finance if my ABN is less than two years old?

Yes, you can still secure funding with an ABN under two years old through specialised “New Venture” or Tier 2 lenders. While prime rates are typically reserved for businesses with two years of trading history, an equipment finance broker sydney can identify lenders who have an appetite for startups. You may simply need to provide a small deposit or show additional proof of your previous industry experience to qualify.

What is a balloon payment and should I include one in my loan?

A balloon payment is a lump sum paid at the end of your loan term to reduce your monthly repayment amounts. It’s a strategic tool for managing cash flow, especially when the equipment generates revenue that can be used to settle the final amount. You should include one if you prefer lower ongoing costs and have a clear plan to either pay the lump sum or refinance the asset at the end.

How long does the equipment finance approval process typically take?

Approval times typically range from 24 to 48 hours for standard applications. Utilising proprietary AI and digital document signing has significantly streamlined this process, often allowing businesses to reach settlement within a few business days. More complex scenarios involving large-scale machinery or specialised medical fit-outs may take slightly longer as lenders conduct deeper financial modelling to ensure the structure is sustainable.

Do I need to provide a deposit for commercial equipment finance?

Many lenders offer $0 deposit options for businesses with a strong credit profile and at least two years of active trading history. This allows you to acquire essential gear without touching your working capital. However, if you’re a startup or purchasing a highly specialised asset with a low resale value, a lender might request a deposit of 10 to 20 per cent to offset their risk.

What happens if I want to upgrade my equipment before the loan term ends?

You can upgrade your equipment at any time by paying out the remaining balance of the loan or trading the asset in. Most lenders allow for early termination, though it’s important to check your specific contract for any break fees. A broker can help you structure a new facility that incorporates the payout of your old asset, ensuring a seamless and stress-free transition to newer technology.