Why would you continue paying off a landlord’s mortgage when your own superannuation fund could be your landlord instead? It’s a common frustration for Australian business owners who see substantial rent payments leave their business every month, providing no long-term benefit to their own retirement. You likely already recognise that an smsf commercial property loan is the key to turning that expense into a wealth-building asset, yet the fear of strict ATO regulations and high deposit requirements often keeps this strategy out of reach.

We understand that the lending landscape in 2026 feels complex, especially with the major banks no longer offering these specialist products. This guide provides the tailored insight you need to regain control, offering a clear path through the technicalities of Limited Recourse Borrowing Arrangements and bare trusts. You’ll learn how to manage the current 70% to 80% LVR thresholds and utilise the A$32,500 concessional contribution cap to build a robust portfolio. We’ll explore the specific steps to secure your premises, ensuring your wealth creation strategy is both tax-effective and perfectly aligned with the latest ATO benchmarks.

Key Takeaways

- Learn why the 2026 market conditions favour commercial assets for higher yields and how to transition from paying rent to building your own equity.

- Understand the protective structure of a Limited Recourse Borrowing Arrangement (LRBA) and how it shields your fund’s existing assets from risk.

- Master the essential steps to secure an smsf commercial property loan, including the correct setup of Bare Trusts and meeting modern lending criteria.

- Discover the financial advantages of “Net Leases” where tenants cover outgoings, creating a more efficient and tax-effective investment stream.

- Find out how to bypass the restrictive criteria of standard banks by accessing a specialist panel of over 30 lenders through a single, professional application.

Table of Contents

- Understanding the SMSF Commercial Property Loan Landscape in 2026

- The Mechanics: How Limited Recourse Borrowing Arrangements (LRBA) Work

- How to Secure an SMSF Commercial Property Loan: A Step-by-Step Guide

- Commercial vs Residential: Why Business Owners Favour Commercial Assets

- Navigating the Complexity: Why an Expert Broker Beats a Standard Bank

Understanding the SMSF Commercial Property Loan Landscape in 2026

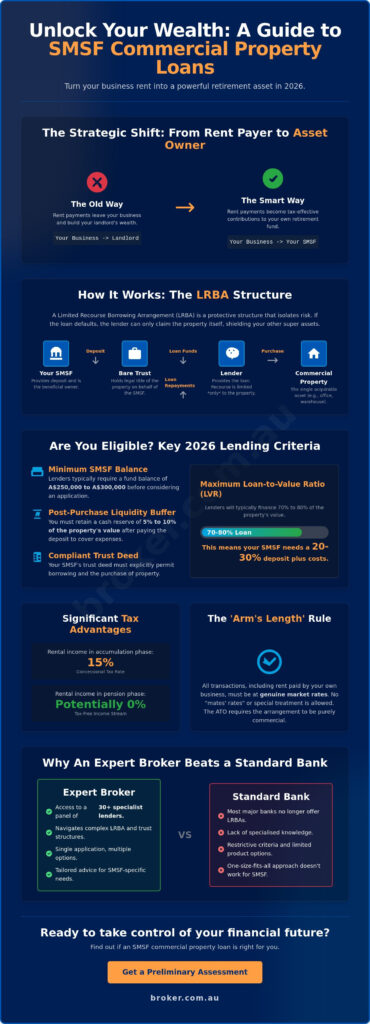

An smsf commercial property loan serves as a sophisticated financial instrument for trustees looking to diversify beyond traditional shares or residential units. Unlike a standard mortgage, this is a specialised facility designed to help your fund acquire high-value assets through a Limited Recourse Borrowing Arrangement (LRBA). The 2026 market has seen a marked preference for commercial assets over residential property. This shift is driven by tighter residential yields and the stability offered by long-term commercial leases, which provide the consistent cash flow required to meet fund objectives. This strategy is underpinned by the complex framework of Superannuation in Australia, ensuring all investments are made for the sole purpose of providing retirement benefits.

The “Arm’s Length” rule remains the cornerstone of compliance. While you can use your fund to purchase a warehouse or office for your own business to occupy, every transaction must reflect genuine market conditions. You can’t offer yourself a “mates’ rates” discount on rent or skip a payment during a slow month. The ATO requires that the fund operates as a professional landlord, ensuring the arrangement is purely commercial and doesn’t provide an improper present-day benefit to members.

The Strategic Shift: From Tenant to Landlord

Stop paying for your landlord’s retirement and start funding your own. By purchasing your business premises through your super, your company’s rent payments become an investment in your future. This approach offers significant tax advantages; rental income within the fund is generally taxed at a concessional rate of 15% during the accumulation phase. If the property is held until you enter the pension phase, that income can potentially become tax-free. Additionally, holding the asset within the superannuation structure provides a layer of asset protection, as the property is legally separate from your personal or business creditors.

Key Eligibility Criteria for 2026

Securing approval requires more than just a good idea. Lenders in 2026 have maintained strict benchmarks for SMSF borrowing. You’ll typically need to demonstrate:

- Fund Liquidity: Most lenders require a minimum SMSF balance of A$250,000 to A$300,000 before they’ll consider an application.

- Liquidity Buffers: You must retain a cash reserve (often 5% to 10% of the property value) after the deposit is paid to cover unforeseen expenses.

- Compliant Trust Deed: Your fund’s trust deed must explicitly allow for borrowing and the purchase of commercial real estate.

- Property Suitability: The asset must be a “single acquirable asset” such as a warehouse, retail suite, or medical consulting room.

The maximum Loan-to-Value Ratio (LVR) generally sits between 70% and 80%, meaning your fund needs a substantial deposit. It’s about showing the lender that the fund is resilient and the investment is sustainable for the long haul.

The Mechanics: How Limited Recourse Borrowing Arrangements (LRBA) Work

The security of an smsf commercial property loan relies entirely on the structure of a Limited Recourse Borrowing Arrangement, commonly known as an LRBA. This legal framework ensures that if the fund defaults on the loan, the lender’s right of recovery is limited to the specific property purchased. Your fund’s other assets, such as cash reserves, shares, or other property holdings, remain protected and out of reach. It’s a vital safeguard that prevents a single investment failure from wiping out your entire retirement nest egg.

To facilitate this, a Bare Trust (also known as a Property Trust) must be established to hold the legal title of the asset on behalf of the SMSF. While the SMSF is the beneficial owner and receives all rental income, the Bare Trust acts as the legal owner until the debt is fully extinguished. If you’re unsure how your current fund balance fits these complex requirements, you can get started with a preliminary assessment to see where you stand. Understanding this separation is crucial because many traditional banks have exited the LRBA space due to these administrative hurdles, leaving specialised non-bank lenders to provide the necessary flexibility for commercial acquisitions.

Compliance hinges on the “Single Acquirable Asset” rule. An LRBA can only be used to purchase one distinct asset. For example, you cannot use a single loan to buy two separate office suites on different titles, even if they are next door to each other. Failing to get this right can lead to severe ATO penalties and may force a premature sale of the asset.

The Structure of a Compliant Loan

A robust structure typically involves a Corporate Trustee rather than individual trustees. This provides long-term stability and simplifies the process when fund members change. One common trap involves property “improvements.” While your fund can use borrowed money for repairs and maintenance to keep the property in its original condition, you cannot use an LRBA to fund significant upgrades or developments that change the nature of the asset. If you want to add an extra floor to a warehouse, you’ll need to fund that through the SMSF’s existing cash reserves rather than the loan.

Managing Interest Rates and LVRs

In the June 2026 lending climate, Loan-to-Value Ratios (LVR) for commercial assets typically range from 65% to 80%. This means your fund needs a substantial deposit of at least 20% to 35%, plus enough liquidity to cover stamp duty and legal fees. Interest rates for an smsf commercial property loan generally sit higher than standard residential mortgages, reflecting the increased regulatory oversight and risk. Currently, advertised rates start from approximately 6.94% p.a. and can reach upwards of 7.69% p.a. depending on the lender’s appetite and the property’s location. Choosing between a fixed or variable rate requires a careful look at your fund’s long-term cash flow and the current 8.95% Safe Harbour benchmark for related-party loans.

How to Secure an SMSF Commercial Property Loan: A Step-by-Step Guide

Moving from the conceptual stage to a successful settlement requires a disciplined, methodical approach. Securing an smsf commercial property loan is significantly more involved than a standard mortgage application. It requires the seamless coordination of your accountant, solicitor, and a specialist broker to ensure every legal requirement is met before you sign a contract. Following this structured path helps mitigate the risk of non-compliance and ensures your fund’s capital is deployed effectively.

Step 1 & 2: The Foundation

The process begins with a rigorous review of your current position. Your accountant must confirm that your investment strategy explicitly permits property borrowing and that your fund has the liquidity to handle both the deposit and ongoing costs. If your trust deed is outdated, it must be amended to meet 2026 lending standards. Engaging specialists from the outset ensures a stress-free setup, providing the peace of mind that your fund remains compliant with the latest ATO regulations while you focus on your business operations.

Once the strategy is clear, you must establish the Bare Trust and Corporate Trustee structures. Lenders require these entities to be correctly sequenced to ensure the Limited Recourse Borrowing Arrangement is valid. Getting this foundation right is non-negotiable; errors in the setup phase can lead to double stamp duty or the rejection of your loan application entirely.

Step 3 & 4: The Hunt and Approval

Before inspecting properties, obtain a formal pre-approval. While a single bank in Australia might offer a limited range of products, using AI-driven brokerage tools allows you to scan the entire 2026 lending market. This technology identifies which lenders have the strongest appetite for your specific industry or property type, whether it’s a specialised medical suite or a standard industrial warehouse.

When you source a compliant asset, your due diligence must be exhaustive. Commercial valuations differ significantly from residential appraisals; they focus heavily on rental yield, tenant quality, and lease terms rather than just comparable sales. You must also conduct specific checks that residential buyers often overlook:

- Zoning Compliance: Ensure the property’s designated use aligns with your business or investment plans.

- Environmental Audits: Check for soil contamination or hazardous materials, which are common hurdles in industrial acquisitions.

- Lease Strength: For investment assets, the remaining lease term is a primary driver of your borrowing power.

Step 5: Finalise the Mortgage and Lease Agreement

The final stage involves executing the loan documents and, for owner-occupiers, formalising the lease between your business and your SMSF. This lease must be at market rates to satisfy the “Arm’s Length” rule. Once the mortgage is settled, the Bare Trust holds the title, and your business begins paying rent directly into your super fund, effectively building your retirement equity with every monthly payment.

Commercial vs Residential: Why Business Owners Favour Commercial Assets

Choosing between a residential house and a commercial warehouse for your super fund isn’t just a matter of preference. It’s a strategic decision that impacts your fund’s liquidity and long-term stability. While residential property is easy to understand, an smsf commercial property loan allows you to tap into an asset class that is purpose-built for wealth creation. The 2026 market shows that commercial yields continue to outperform residential averages, providing the cash flow needed to manage loan repayments without draining the fund’s liquid reserves.

The Business Real Property Advantage

The “Business Real Property” (BRP) rule is often described as the “holy grail” for small business owners. Usually, super funds are strictly prohibited from dealing with related parties. BRP changes the game by allowing your SMSF to purchase the very office or workshop you operate from. This means your business pays rent directly to your fund, effectively moving capital from your company’s balance sheet into your tax-sheltered retirement environment.

Compliance is straightforward but strict. The lease must be a formal document, and the rent must be verified by a valuer to ensure it matches current market rates. This arrangement provides your business with long-term tenure and your super fund with a reliable, high-quality tenant. If you’re ready to stop paying a third-party landlord and start investing in your own future, enquire about our tailored commercial solutions to get a clear picture of your borrowing capacity.

Yield and Growth Comparison

Commercial assets in 2026 typically offer net yields of 5% to 8%, significantly higher than the 2% to 4% often seen in residential markets. This performance is enhanced by “Net Lease” structures. In these arrangements, the tenant covers most outgoings including council rates, water, and insurance. For an SMSF trustee, this means more of the rental income stays in the fund rather than being eaten away by maintenance costs.

While commercial property carries a higher risk of extended vacancy, the lease terms offer much better protection. You aren’t looking for a new tenant every year; instead, you’re securing three, five, or even ten-year commitments. This long-term security makes it easier to project your fund’s performance over a decade or more. When you combine this with the potential for zero capital gains tax in the pension phase, the argument for commercial assets becomes hard to ignore. It’s about building a sophisticated portfolio that works as hard as you do.

Navigating the Complexity: Why an Expert Broker Beats a Standard Bank

Standard banks often lack the agility and technical depth required to manage an smsf commercial property loan effectively. While a local branch manager might understand a basic home loan, the intricate layering of Bare Trusts, Corporate Trustees, and ATO compliance often exceeds their standard credit policy. This narrow focus frequently leads to unnecessary rejections for perfectly viable funds. Broker.com.au offers a different path. Instead of being restricted to one bank’s rigid criteria, you gain access to a panel of over 30 specialist lenders through a single, professionally managed application.

Our proprietary AI technology takes the guesswork out of the process by matching your fund’s unique profile with the lender most likely to offer an approval. We don’t just find a loan; we integrate corporate advisory insights to ensure your total debt is structured for maximum capital efficiency. This holistic approach ensures that your property acquisition doesn’t just meet a requirement but actively strengthens your fund’s overall performance. It’s about looking at the big picture of your wealth, not just a single transaction.

Inside Access to Specialist Rates

The most competitive opportunities in 2026 often lie with non-bank and private lenders that don’t deal directly with the public. We provide inside access to these specialist rates, many of which offer more flexible LVRs or more favourable terms for niche industries like medical consulting or specialised industrial warehousing. Our team acts as a “High-Level Fixer” for complex fund structures, navigating the “outside of the norm” scenarios that traditional lenders often find too difficult to process.

We take over the heavy lifting of document preparation and compliance checks, providing a “stress-free” experience that keeps your application moving forward. By acting as the professional bridge between your fund and the lender, we ensure that every technicality is addressed before it can cause a delay. This level of personal attention ensures your fund remains in good hands from the initial enquiry through to final settlement.

Starting Your SMSF Journey

The path to property ownership doesn’t have to be a source of anxiety or confusion. An initial conversation with our experts allows you to gauge your fund’s actual borrowing capacity and identify any potential roadblocks before they become expensive problems. We help you move from a state of uncertainty toward a streamlined, confident investment strategy that secures your business’s future. If you’re ready to take the next step and gain full control over your superannuation, I’m interested in an SMSF commercial loan.

Take the Next Step Toward Property Ownership

Securing an smsf commercial property loan is a transformative move for any Australian business owner. It allows you to move beyond the limitations of traditional superannuation and start building tangible equity in the very premises that drive your success. By mastering the mechanics of Limited Recourse Borrowing Arrangements and ensuring your Bare Trust is correctly structured, you protect your fund’s existing assets while capturing the high yields and long-term security that commercial property offers in 2026.

As an award-winning Australian brokerage, we provide you with inside access to a vast panel of specialist lenders that operate far beyond the reach of major banks. Our proprietary AI-powered loan matching technology ensures your application is directed toward the lender with the highest probability of approval, making the entire journey seamless and efficient. You don’t have to navigate these technicalities alone; our team is here to act as your expert guide through every compliance hurdle.

I’m interested in exploring SMSF loan options

You’re in good hands with our specialists. We’re ready to help you turn your retirement goals into a concrete reality and secure your operational base for years to come.

Frequently Asked Questions

Can I use my SMSF to buy a commercial property for my own business?

Yes, you can purchase a warehouse, office, or retail space through your fund and lease it back to your own business. This is possible under the “Business Real Property” exception, provided the lease is conducted at a market-rate rent. You must have a formal lease agreement in place to ensure the arrangement remains at “arm’s length” and stays compliant with ATO regulations.

What is the minimum deposit required for an SMSF commercial property loan?

You will generally need a deposit of at least 20% to 30% of the property’s purchase price. In the 2026 lending environment, most Loan-to-Value Ratios (LVR) are capped at 70% to 80%. It’s also essential to have extra capital within the fund to cover stamp duty, legal costs, and the mandatory liquidity buffers required by most lenders.

Can I renovate a commercial property owned by my SMSF?

You can renovate the property, but you cannot use borrowed money for “significant improvements” that change the asset’s essential character. Any major upgrades or extensions must be funded entirely from the fund’s existing cash reserves. Standard repairs and maintenance intended to keep the property in its original condition are permitted and can be managed through the smsf commercial property loan or fund cash.

How much can my SMSF borrow to buy a warehouse or office?

While borrowing capacities vary, many specialised lenders provide funding for amounts up to A$5,000,000. Your specific limit depends on the property’s valuation and your fund’s ability to meet repayments through rental income and concessional contributions. Lenders also typically look for a minimum fund balance of A$250,000 to A$300,000 before approving an application.

Are the interest rates for SMSF commercial loans higher than standard loans?

Yes, interest rates for these specialised products are typically higher than standard commercial mortgages. This reflects the increased regulatory complexity and the limited recourse nature of the arrangement. As of June 2026, advertised rates generally start from 6.94% p.a., while the ATO Safe Harbour benchmark for related-party loans is set at 8.95%.

What happens if my SMSF cannot make the loan repayments?

If your fund defaults, the lender’s right of recovery is restricted solely to the property held as security. Because of the Limited Recourse Borrowing Arrangement (LRBA) structure, the lender cannot claim any other assets within your super fund, such as your shares or cash balances. This keeps the rest of your retirement nest egg safe even if the property investment fails.

Do I need a separate trust for an SMSF property loan?

Yes, you must establish a Bare Trust, also known as a Property Trust, to hold the legal title of the asset. This trust is a legal requirement that keeps the property separate from the rest of the fund’s assets while the debt is outstanding. Once the smsf commercial property loan is fully repaid, the legal title can be transferred directly to the SMSF.

Can I transfer a property I already own into my SMSF?

You can transfer commercial property you already own into your fund, which is a significant advantage not available for residential assets. This can be achieved through a market-value purchase or as an “in-specie” contribution. It’s a popular strategy for business owners looking to move their operational premises into a more tax-effective environment while staying within contribution limits.