In the current Australian market, waiting for traditional bank approval is often the quickest way to lose a competitive edge. Most business owners understand the frustration of watching a prime acquisition or a vital equipment upgrade slip away because capital was locked behind a rigid repayment schedule. A flexible line of credit is no longer just a debt facility; it’s a strategic asset for “opportunity readiness” that ensures you’re never caught off guard by cash flow gaps or sudden emergencies.

We recognise that the pressure of managing working capital while avoiding high interest rates can feel like a constant balancing act. This guide is designed to help you master the mechanics of revolving credit to boost your business agility and secure your financial future. You’ll discover how to build a robust financial safety net and access the capital needed for quick growth, all while maintaining the streamlined confidence that comes from expert financial positioning. We’ll explore the latest 2026 lending trends to ensure your business remains resilient in an evolving economy.

Key Takeaways

- Understand how a revolving line of credit provides a flexible safety net where you only pay interest on the funds you actually use.

- Learn to balance lower interest rates against asset security when deciding between secured and unsecured funding structures.

- Discover why a strategic line of credit often outperforms a standard business overdraft for long-term growth and acquisition plans.

- Identify the specific metrics, such as your Debt-to-Income ratio, that Australian lenders prioritise in the 2026 credit landscape.

- Gain inside access to how AI-driven insights can streamline your application and connect you with tailored finance solutions.

Table of Contents

- What is a Line of Credit? The “Swiss Army Knife” of Australian Finance

- Secured vs. Unsecured: Choosing the Right Structure for Your Business

- Line of Credit vs. Business Overdraft: Which Tool Should You Reach For?

- Qualifying for a Line of Credit: What Lenders Look for in 2026

- Optimising Your Cash Flow with Broker.com.au’s Expert Guidance

What is a Line of Credit? The “Swiss Army Knife” of Australian Finance

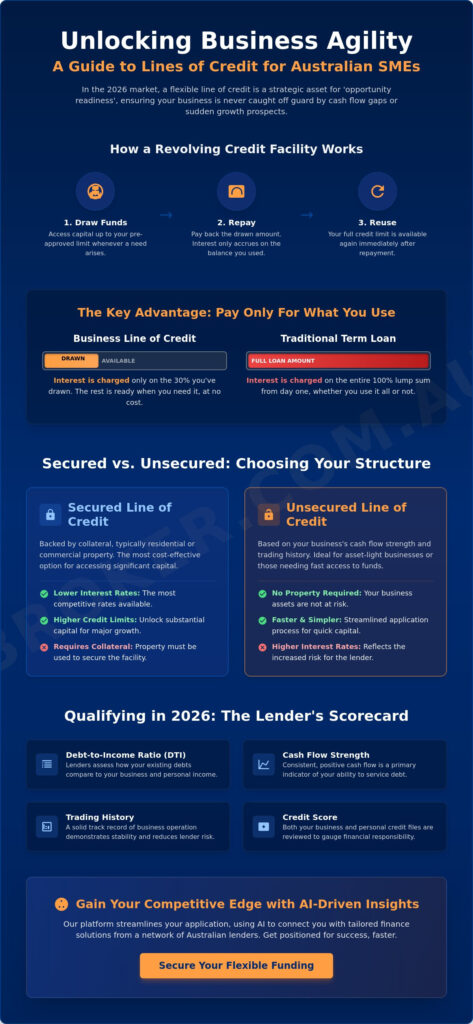

A business line of credit is a flexible, revolving credit facility that provides a pre-approved limit of capital which can be drawn, repaid, and reused as needed, with interest only accruing on the balance actually utilised. This tool acts as the ultimate financial safety net for Australian SMEs. Unlike a fixed-term loan, where you receive a lump sum and begin paying interest on the total immediately, this facility offers a “pay only for what you use” model. It remains available in the background, ready to be deployed the moment a project requires a boost or an unexpected invoice arrives.

Understanding What is a Line of Credit? requires looking beyond simple debt. It’s a strategic resource for the 2.72 million actively trading businesses across Australia. While a term loan is often rigid and requires a new application for every capital injection, a revolving facility scales with your needs. It provides a buffer against the cash flow gaps that often occur between project milestones or during long payment cycles.

How a revolving credit facility actually works

The mechanics of this facility are straightforward yet powerful. Once a lender approves your limit, you gain access to a pool of funds. You can draw down A$10,000 to cover a supplier deposit, pay it back three weeks later, and then immediately have that full limit available again. This cycle of drawing, repaying, and redrawing is what makes it “revolving.”

It’s vital to distinguish between your total credit limit and your available balance. You only incur costs on the portion you’ve actually withdrawn. Lenders typically calculate interest on a daily basis, ensuring maximum transparency. This means if you only use the funds for five days to bridge a gap, you’re only charged for those five days. It’s an efficient way to manage working capital without the burden of long-term interest commitments on idle cash.

Why flexibility is essential for 2026 market conditions

In the 2026 economic environment, agility is your greatest asset. Global uncertainty continues to disrupt supply chains, often requiring businesses to secure inventory quickly when it becomes available. Having instant capital access allows you to bypass the lengthy approval processes of traditional banks. You can act while your competitors are still filling out paperwork.

This flexibility also supports proactive growth. If a business acquisition opportunity arises, or if you need to capitalise on a seasonal revenue surge, the funds are already there. Australian businesses often face seasonal fluctuations, whether in tourism, agriculture, or retail. A line of credit smooths these peaks and troughs, providing a reliable buffer that protects your personal peace of mind and keeps your operations running seamlessly.

Secured vs. Unsecured: Choosing the Right Structure for Your Business

Choosing the right structure for your line of credit is a foundational decision that impacts your interest costs and your personal risk profile. In the Australian commercial lending landscape, this choice usually boils down to the trade-off between lower interest rates and asset security. A secured facility requires collateral, typically in the form of residential or commercial property, while an unsecured facility relies on the strength of your business’s cash flow and trading history.

When exploring various Types of business finance, you’ll find that secured options often provide the most competitive pricing. However, they frequently involve a General Security Agreement (GSA). This legal document gives the lender a claim over all your company’s assets. While this structure is standard, it requires careful consideration to ensure you aren’t over-leveraging your business’s future. Best-in-class brokers look beyond the headline rate to analyse your total debt structure, ensuring your security arrangements don’t stifle your ability to borrow from other sources later.

Equity-linked lines of credit and the family home

For many Australian directors, the family home is the most powerful tool for unlocking “dead equity” to fuel business growth. By linking a line of credit to property, you can access significantly lower rates compared to unsecured products. It’s a highly efficient way to fund a business acquisition or a major fit-out. However, you must be wary of cross-collateralisation. This occurs when a bank uses your home to secure multiple loans, potentially giving them control over your private residence if the business hits a rough patch. Professional guidance is essential to ring-fence your personal assets while still capitalising on your equity.

Unsecured business lines of credit for rapid scaling

If you prefer to keep your personal property separate from your business ventures, an unsecured line of credit offers ultimate peace of mind. These facilities are assessed based on your monthly turnover and GST registration rather than physical assets. The primary advantage here is speed. Using advanced AI-driven credit assessment, many non-bank lenders can approve limits in days rather than months. This is particularly useful for managing supply chain disruptions or capitalising on sudden market opportunities. While the interest rates are higher, the lack of a GSA or property charge provides a level of flexibility that many modern entrepreneurs prioritise. If you’re unsure which path fits your current growth stage, it’s often helpful to start a low-pressure conversation with an expert who understands the nuances of the 2026 lending market.

Line of Credit vs. Business Overdraft: Which Tool Should You Reach For?

Many directors view an overdraft and a line of credit as interchangeable. While both offer revolving access to capital, their roles within a sophisticated financial model are distinct. An overdraft is typically an “on-demand” extension of your transaction account, designed to catch minor errors or brief timing gaps in payments. In contrast, a line of credit is a “strategic” facility. It often exists as a separate account with much higher limits, specifically tailored for growth initiatives rather than just covering day-to-day bills.

Fee structures also vary significantly between these two options. Overdrafts usually carry higher interest rates, often ranging from 14.55% to 25.00% p.a. as of May 2026, but they may have lower ongoing maintenance costs. A line of credit typically offers lower interest rates but includes a “line fee” or facility fee. This is a percentage charged on the total limit, regardless of whether you use the funds. For industries like construction, where project costs are massive and lumpy, the lower interest rate on a line of credit usually outweighs the facility fee. Retailers, however, might prefer an overdraft to manage small, frequent transaction account dips. To understand how these fit into your broader strategy, consult the Australian Government guide to business finance for foundational management tips.

When a business overdraft makes more sense

An overdraft is the ultimate tool for seamlessness. Because it’s linked directly to your trading account, it prevents “honour fees” or bounced payments if a client’s remittance is delayed by a day. It’s perfect for handling minor fluctuations without manual transfers. However, be aware of “clearing” requirements. Some lenders expect the account to return to a credit balance at least once every 30 days. This makes it unsuitable for long-term funding or significant project work.

The long-term benefits of a stand-alone line of credit

A stand-alone facility allows you to separate your growth capital from your operational cash. This separation provides much better visibility for financial modelling and tax reporting. Because these facilities aren’t tied to your daily spending, lenders are often more comfortable providing higher borrowing power. This is essential for business acquisition funding or major equipment upgrades. You also gain greater control over repayment schedules. Many providers offer interest-only periods, allowing you to reinvest profits back into the business during a scaling phase rather than being forced into immediate principal repayments. This flexibility is what transforms a simple credit limit into a genuine engine for business agility.

Qualifying for a Line of Credit: What Lenders Look for in 2026

The criteria for securing a line of credit have shifted significantly in recent years. In 2026, the assessment process has moved away from slow, manual reviews toward sophisticated AI-driven insights. Lenders now use real-time data feeds to evaluate your business’s health, focusing heavily on your Debt-to-Income (DTI) ratio. This metric is currently the most critical factor for Australian lenders, as it provides a clear picture of your ability to service new debt alongside existing obligations. If your DTI ratio is too high, even a strong turnover might not be enough to secure the limit you’re after.

Maintaining clean bank statements and up-to-date Business Activity Statement (BAS) filings is non-negotiable. Lenders scrutinise these documents for any signs of financial stress, such as late tax payments or frequent account dishonours. A professional broker plays a vital role here, helping you “present the case” by highlighting your strengths and explaining any temporary fluctuations. This proactive approach ensures a much more streamlined, stress-free approval process. If you want to see where your business stands, you can get started with a tailored assessment today.

Credit scores, ABN length, and financial modelling

While the focus is on the business, your personal credit history still carries weight. A strong personal score acts as a secondary layer of security for the lender. Most “best in class” interest rates are reserved for businesses that have held an active ABN for at least two years. If your business is younger, you may still qualify, but you’ll likely need robust financial modelling to prove your projected cash flow. This modelling demonstrates to the lender that you’ve planned for various market scenarios and can comfortably manage the revolving facility.

Documentation: Low-doc vs. Full-doc options

The choice between low-doc and full-doc applications usually depends on your need for speed versus your desire for the lowest possible rate.

- Low-doc: These facilities are ideal for rapid scaling. They require less paperwork, often relying on just a few months of bank statements and an ABN check. This path offers speed and privacy but typically comes with slightly higher interest rates.

- Full-doc: For businesses looking to lock in the most competitive pricing, a full-doc application is superior. You’ll need to provide complete financial statements, tax returns, and details of your company structures or trust deeds.

Organising your trust deeds and company structures early is essential. Lenders in 2026 are increasingly selective, and having these documents ready for scrutiny shows a level of professional maturity that can help tip the scales in your favour.

Optimising Your Cash Flow with Broker.com.au’s Expert Guidance

The Australian lending market has undergone a significant transformation recently. While several traditional institutions have restricted access to flexible revolving facilities for new clients, the demand for capital agility has never been higher. This shift has created a complex landscape for business owners to navigate alone. At Broker.com.au, we act as your expert guide, providing a whole-of-market perspective that far exceeds the limited options of a single lender. We don’t just offer products; we provide a sophisticated corporate advisory service designed to protect your cash flow and fuel your long-term dream.

Our proprietary AI technology is at the heart of our award-winning approach. It allows us to scan the Australian market in real-time, identifying the perfect lender for your specific niche, whether you’re in construction, retail, or professional services. This technology, combined with our “inside access” to the best rates, ensures you receive tailored solutions that aren’t advertised to the general public. We believe in a low-pressure conversation, which is why we use the “I’m interested” approach. It’s the start of a stress-reduction promise that moves you from uncertainty toward streamlined confidence.

Leveraging technology for a seamless application

We’ve eliminated the traditional paperwork burden through deep digital data integration. By connecting directly with your accounting software, our systems provide lenders with the real-time insights they need to say “yes” faster. This efficiency means you can focus on running your business while we handle the heavy lifting. Our team, including specialists like Matt and Kylie, monitors rate changes across the entire Australian market constantly. This proactive stance ensures that your line of credit remains competitive long after the initial settlement. Getting a fast approval isn’t just about speed; it’s about providing the agility you need to capitalise on sudden market opportunities.

Personalised advisory for complex business structures

Navigating borrowing within complex structures like trusts or SMSF loans requires a high-level fixer. Our advisors are deeply knowledgeable about the nuances of the Australian regulatory environment, including the current exemptions for small business lending. We often work with clients to restructure existing debt, freeing up essential cash flow for new acquisitions or equipment upgrades. Being “in good hands” means having a partner who goes above and beyond the norm to find a path to resolution. Whether you’re looking for a secured line of credit to unlock property equity or an unsecured option for rapid scaling, we ensure the process is professional, efficient, and entirely seamless. Your business deserves a finance partner that prioritises results over mere process.

Unlock Your Business Potential with Strategic Finance

Mastering a line of credit is about more than just managing debt; it’s about building a foundation of operational agility. We’ve explored how revolving facilities provide a vital safety net for cash flow gaps and how choosing between secured and unsecured structures can protect your personal assets while reducing interest costs. In the 2026 lending environment, being “opportunity ready” means having capital at your fingertips before the next big acquisition or project arises.

At Broker.com.au, we provide award-winning finance solutions designed to move you from uncertainty to streamlined confidence. Our team offers inside access to over 50 Australian lenders and utilises an AI-powered application process to deliver stress-free results. We’re here to help you navigate complex structures and find the perfect fit for your specific business goals. If you’re ready to take the next step, I’m interested in a tailored line of credit for my business. Let’s work together to turn your professional dreams into a resilient financial reality.

Frequently Asked Questions

Is a line of credit better than a credit card for my business?

Yes, a line of credit is typically superior for managing significant operational costs or growth initiatives. While credit cards are convenient for minor daily expenses, they often carry interest rates exceeding 20% p.a. A business facility offers much higher limits and significantly lower rates, making it a more professional tool for strategic funding. It provides the flexibility of a card but with the financial modelling benefits of a corporate loan.

Can I use a line of credit to purchase a new business or franchise?

Absolutely. Using a line of credit for business acquisition funding is a common strategy for scaling. It allows you to act decisively when a franchise or competitor becomes available for purchase. Because the funds are pre-approved, you can settle the deal without the delays of a new application. This “opportunity readiness” is a key advantage for directors looking to expand their portfolio quickly in the Australian market.

How much can I borrow with an unsecured business line of credit?

Borrowing limits for unsecured facilities are primarily determined by your business’s monthly turnover and trading history. Generally, Australian lenders offer unsecured limits ranging from A$5,000 up to A$500,000. Because no physical asset is required as collateral, the lender focuses on your cash flow health. If your business has a consistent revenue stream and an active ABN for over two years, you can often access these higher limits within days.

What happens if I don’t use the funds in my line of credit?

If you don’t draw down any funds, you won’t pay any interest. This makes the facility an excellent emergency buffer. However, most lenders charge an ongoing facility or “line fee” to keep the credit available. These fees are usually charged monthly or quarterly. It’s a small price to pay for the peace of mind that comes from having immediate access to capital whenever your business requires a boost.

Are line of credit interest rates fixed or variable in Australia?

In the Australian market, interest rates for these facilities are almost exclusively variable. This means your rate will fluctuate in line with changes to the lender’s benchmark or the Reserve Bank of Australia’s cash rate. While variable rates introduce some uncertainty, they also offer the flexibility to make unlimited repayments without the “break costs” associated with fixed-term loans. This aligns perfectly with the revolving, on-demand nature of the product.

How do I convert a line of credit into a term loan later on?

Converting your balance into a term loan is usually achieved through a refinancing process. If you’ve used your line of credit to fund a long-term asset and prefer a structured repayment schedule, a term loan can provide the certainty of fixed monthly payments. Our team can help you navigate this transition, ensuring your debt structure remains efficient. It’s a common move once an acquisition has stabilised and requires a predictable principal-and-interest plan.

What are the typical fees associated with a revolving credit facility?

You’ll typically encounter an establishment fee, which ranges from 0.50% to 2% of the total credit limit. Ongoing facility fees are also standard, often charged per quarter depending on the size of your limit. Some lenders may also apply drawdown fees each time you transfer funds to your trading account. We provide inside access to fee-transparent lenders, ensuring you understand the total cost of your facility before signing any contracts.

Can I link my line of credit to my offset account?

While offset accounts are a staple of residential home loans, they are rarely available for commercial lines of credit. Instead, these business facilities function like a giant transaction account where the balance is the “debt.” Any funds you deposit into the facility immediately reduce the balance, which in turn reduces the interest you’re charged. This “all-in-one” structure provides a similar benefit to an offset account by keeping your interest costs as low as possible.